Online retail sales growth slowed in May following a fairly strong April

Insight

US non-farm payrolls data emed to indicate a Goldilocks economy – more jobs and with wages contained.

https://soundcloud.com/user-291029717/goldilocks-and-the-magic-money-tree

March US payrolls growth beat expectations, but market reaction was muted both for the USD and Treasuries. Payrolls rose 196k, above the formal 177k expectations (NAB +156k) and whispers that the extensive floods might have forestalled hiring. Despite the return of strong payrolls growth, wages were soft, lower than expected at 3.2% y/y against 3.4% expected (NAB 3.3%), amplifying the message of yet another Goldilocks report, great for growth markets without stoking inflation worries.

The unemployment rate was also unchanged at still low 3.8%, while the participation rate fell two-tenths to 63.0% from 63.2%. Payroll growth did not add any new fears about US growth, coming after last month’s low read that was playing to the lower growth paradigm. It was a report that keep the Fed alert to how the economy is transitioning beyond the early year weakness, an eye also on the evolving trade talks and what may come out of that.

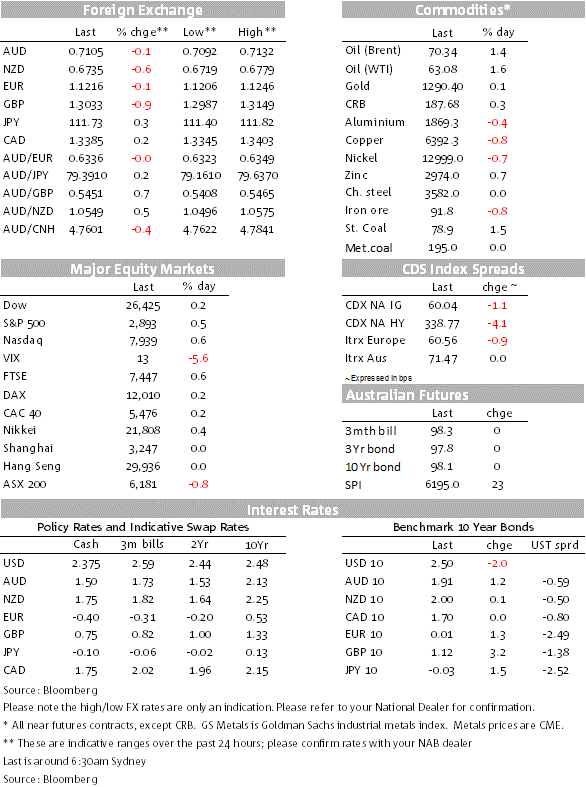

Yields gyrated initially, taking their cue from the lower wages print and then taking note of the headline payrolls beat. In the end yields settled lower, with 10yr yields -3.9bps to 2.4954% and 2yr yields -2.2bps to 2.3322%. FX was broadly unchanged with the USD (DXY) remaining around 97.30, the DXY making some further incremental gains over the course of the US session.

After the report, President Trump called for the Fed to reverse course and to undertake quantitative easing: “I personally think the Fed should drop rates” because they are slowing down the economy and instead of “quantitative tightening it should actually now be quantitative easing”. As for Fed Funds pricing, markets continue to price in a high chance of the Fed cutting rates with a 70% chance of a rate cut by December 2019.

The AUD opens the week at 0.7105, with little net change over the course of last week, initially a lower AUD after the change to the RBA’s forward guidance in their post-Board statement on Tuesday, followed by a rally after better than expected retail sales report for February. The AUD did drift lower on Friday after payrolls, the USD getting something of a bid tone, despite the further rally in equities, a lower VIX and of course non-threatening US average earnings growth.

This morning’s press sees a post-Budget Newspoll with the Coalition getting something of a post-Budget bounce. On a two party preferred basis, it’s back to a 48/52 split, the Coalition making up two points in the latest poll, the Oz today describing it as the post-Budget bounce.

The election date has still not been called by the PM, now making May 18 an almost certain date with the election now likely to be announced this coming weekend. If you follow the polls, Sportsbet has Labor still as short-priced favourite at 1.14 and the Coalition at 5.00, pretty much the same as before the Budget.

On the Brexit front, PM May is continuing to squeeze the Brexiteers in her party to accept a deal or risk a longer timeline risking no Brexit but with no clear success as yet and with more timelines approaching. There is now particular news on the negotiations with Corbyn, all this ahead of Wednesday’s EU Summit where she is expected to press the case for a further extension beyond Friday’s date that was the extension granted by the EU beyond 29 March.

Theresa May requested a short extension to Brexit from the EU, to June 30th, something the EU has previously turned down. Negotiations between Corbyn and May will continue, with the Sunday Times reporting that May is willing to make some concessions on joining a customs union and was willing to write this into law (thereby making it difficult for her successor to undo). If no solution in the negotiations can be found, May has promised that MPs will get to vote on a range of Brexit options, with the government apparently willing to abide by parliament’s decision, although time is short before the EU Summit on Wednesday.

Downing Street released a statement saying “on Brexit there are areas where the two main parties agree: we both want to end free movement, we both want to leave with a good deal, and we both want to protect jobs. That is the basis for a compromise that can win a majority in Parliament and winning that majority is the only way to deliver Brexit. The longer this takes, the greater the risk of the UK never leaving at all,” she said. Corbyn said over the weekend that he was waiting for her to move on her plan.

The Pound was softer at the end of this week, the worst performing currency on Friday, down a net 0.57% since we went home Friday.

Meanwhile, the Sino-US trade talks were reported to have made “new progress” according to the Chinese press over the weekend, including on the ever-thorny issues of IP, verification and more. There are more talks this week, apparently by video link. The mood music continues to be quite positive, though the market awaits a “deal”.

Rounding out the week on the data front, German Industrial Production for February was better than expected up 0.7% (expected 0.5%) also coming with a handy upward revision to January’s from -0.8% to flat. Supported by better construction activity, IP is on track to increase by a net 0.5% in Q1, adding in the order of 0.2% points to overall growth.

Canadian employment was a little lower than expected in March, down 7.2K, but that was after a very strong 55K February gain. The unemployment rate was steady at 5.8%. The CAD drifted lower over the NY session on Friday, but only in line with the soft bid for the USD, and despite oil having a good session, WTI up 1.4% on continuing supply news from OPEC caps and Venezuelan production woes.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.