SME conditions stable but still below average

Insight

Phil Dobbie talks to NAB’s Tapas Strickland about the market reaction to this, and to Theresa May’s announcement that 23 Russian diplomats will be sent packing in response to the Salisbury nerve agent attack.

President Trump is expected to launch new tariffs on China next week. Phil Dobbie talks to @NAB’s Tapas Strickland about the market reaction on today’s #MorningCall. Little reaction to UK’s expulsion of Russian diplomats. Plus retail sales in China and the US and GDP in New Zealand.

https://soundcloud.com/user-291029717/us-targets-china-uk-targets-russia

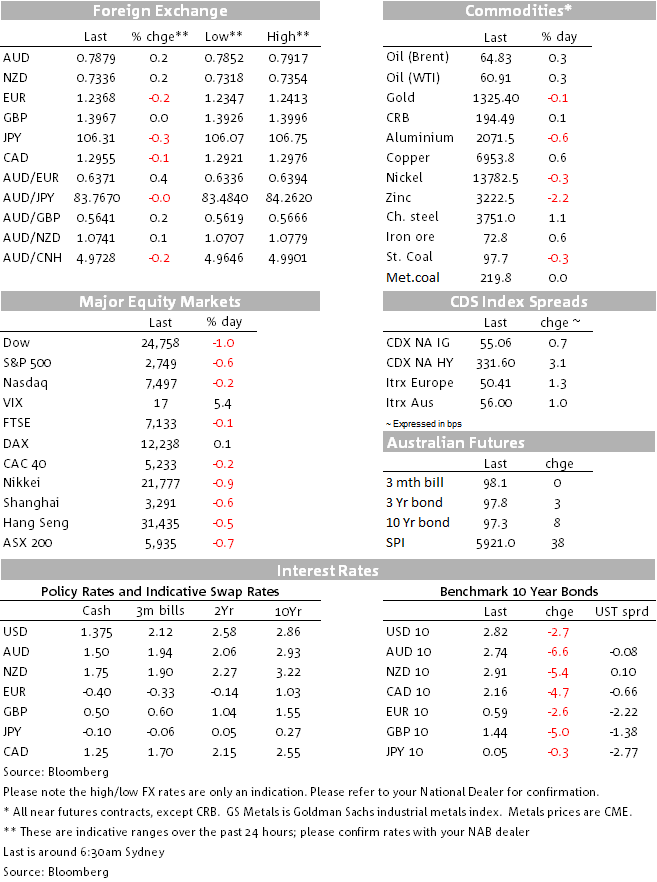

Market optimism has been dented over night following a string of news that provided cause for pause on the consensus view over the upbeat global growth outlook. US data disappointed, Draghi sounded dovish, the White House confirmed its intentions for more China sanctions, the UK spells Russian diplomats and the Libor/OIS spread widened again, further tightening offshore USD short term funding.

February US retail sales underwhelmed against expectations of a tax cut induced rebound. The headline reading printed a third consecutive reading of -0.1%mom against expectations of an uptick to 0.3%. The retail sales ‘control group’, which feeds directly into GDP, rose only 0.1% in February, despite near-record levels of consumer confidence.

US equities opened higher, but then immediately headed south factoring the softer US data that had been released an hour earlier. Later in the overnight session the White House confirmed it wants to reduce the US Trade deficit with China by $100bn, following yesterday’s reports on the administration’s plans to impose trade tariffs on $60bn of imports from China. The news dented to risk sentiment again, dragging US equities and UST yields lower. Then the move was further compounded by the release of the Atlanta Fed GDPNow index showing a trim to US GDP growth for Q1-18 to 1.85% from 2.48%. Meanwhile, A Chinese foreign ministry spokesman said “if the United States takes actions that harm China’s interests, China will have to take measures to firmly protect our legitimate rights.”. All major US equity indices are trading in negative territory with the S&P500, currently down 0.57%.

The move lower in UST yields has been led by the back end of the curve with the 10y and 30y yields down 3.4bps and 4.6bps respectively. 10y UST yields traded to an overnight low of 2.7988%, coming close to the lower end of the 2.78%-2.95% range that has been in place over the past 5 weeks. The 10y rate now trades at 2.813% while the 30y rate is at 3.053%. The 2y10y curve flattened for a 3rd consecutive day with the spread currently at 55.5bps, its lowest level since January 26th. 10y UK gilts (-5bps) and Bunds (-2.6bps) also closed lower, at 1.4337% and 0.593% respectively. News that the UK had decided to spell 23 Russian diplomats and Draghi’s dovish remarks (see more below) were additional factors helping the move lower in European yields.

Meanwhile currency moves have been relatively contained with the USD little changed in index terms. SEK is the top G10 performer, up 0.48% with pair currently trading at 8.18. Overnight Sweden CPI data for February printed in line with expectations at 0.7%mom. The mild risk aversion tone to the overnight session plus ongoing political concerns surrounding the Abe government has seen USD/JPY drift lower over the past 24hrs with the pair currently trading at ¥106.31, after trading to an intraday high of ¥106.75 during our APAC session yesterday.

AUD rose steadily in the early part of the overnight session, seemingly still basking in the glory from yesterday’s better than expected China activity data, a factor that also boosted most commodities. Iron ore leading the way, up 0.59%, Copper 0.50% and oil prices up around 0.35% ( after some volatility on the back of news that OPEC raised its expectation for supply growth from the US and other producers for a fourth consecutive month). Steam coal, on the other hand, has remained under pressure down 1.02% on the day. AUD reached an overnight high of 0.7917, but the turn in risk appetite that began around midnight weighed on the aussie, dragging the pair down to 0.7871, 10pips below where it currently trades. Taking a step back, the AUD continues to find the air quite thin around the 0.7920/30 area, but at the same time the pair remains in a mild upward trend that began on the first day of the month which saw the currency trade down to a low of 0.7713.

The Euro currently trades at 1.2368, after trading to a low of 1.2347 overnight following comments from ECB President Draghi noting that recent EUR gains “weren’t all warranted by economic fundamentals.”. The President also noted that the ECB is more confident on “inflation converging towards our aim over the medium term”, but that further evidence is needed. Accordingly, monetary policy “will remain patient, persistent and prudent”.

Ahead of the NZ GDP release this morning (see more below), The NZD traded in very narrow range overnight, between 0.7318 and 0.7349, and currently sits at 0.7335.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

SME conditions stable but still below average

Insight

NAB executives give their view on the critical role brokers play, and the opportunities ahead. Originally published on Australian Broker on 24/06/24

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.