Online retail sales growth slowed in May following a fairly strong April

Insight

Another bond rally, this time in the UK with inflation coming in softer than expected.

Coming up: AU Jobs, CH Loan Prime Rate, JN Trade, US Jobless Claims/Philly Fed

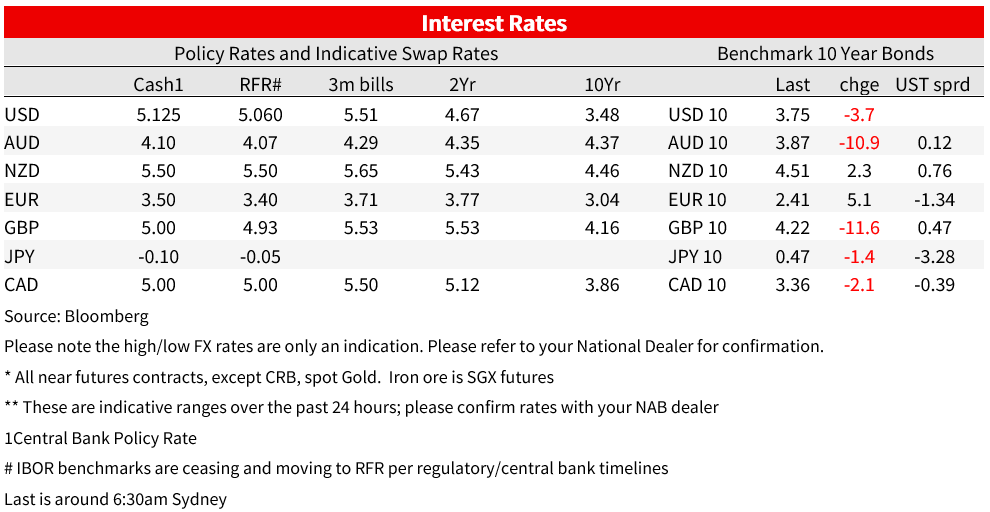

Another bond rally, this time in the UK with inflation coming in softer than expected. Headline CPI was 7.9% y/y vs 8.2% expected, and Core was 6.9% y/y vs. 7.1% expected. UK Gilt yields tumbled with 2yr -18.4bps to 4.91% (low 4.86%) and 10yr -11.7bps to 4.21% (low 4.14%). BoE Bank Rate pricing also fell sharply, with terminal pricing falling by around 20bps to 5.80% by February from 6.0% yesterday. As for the August BoE meeting, markets now price a 44% chance of a 50bp rise in August, down from 70% previously. The moves in Gilts initially dragged yields lower elsewhere in what was a quiet night for data. US 10yr yields are -4.3bps to 3.74%, though 2yr yields are little changed on net at 4.76% (low 4.69%) with the 2/10s curve -4.5bps to 102.4bps. The moves were almost entirely reflected in real yields with the 10yr TIP yield -4.0bps to 1.52%. One piece of news worth watching for food inflation is the price of wheat which rose 9% after Russia warned it would treat ships travelling to Ukraine as potentially carrying arms.

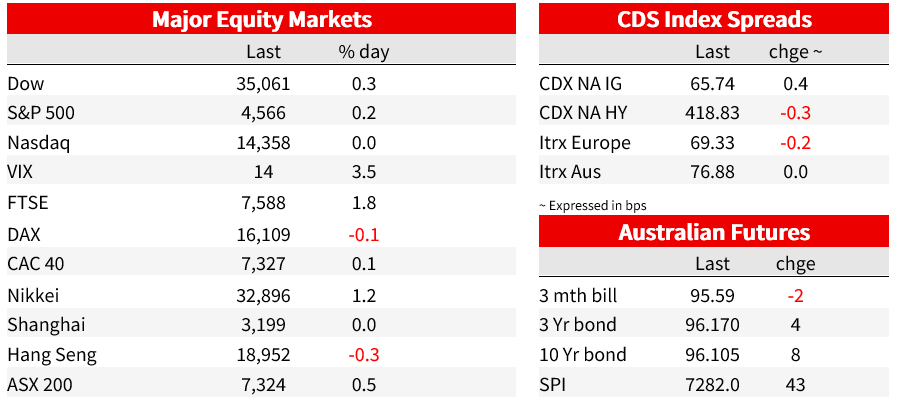

Equities meanwhile rose with the S&P500 +0.2%, and it is worth noting the index is now only 4.8% away from its all time high, having rallied 27.6% from its low of 2022. A larger equity rally was seen in the FTSE of 1.8% following the softer than expected CPI figures. US earnings season continues to surprise to the positive with 78% so far beating expectations, bolstering views of a soft landing. Reporting after the close yesterday was JB Hunt, a large US transport firm, which said it “saw evidence from customers in June that the destocking has moderated ”, with its shares up some 3.8% today. Goldmans meanwhile was the last mega bank to report with its shares up 1.0% even though it missed second quarter earnings (3.08 a share vs. 3.18 expected); revenue did beat though at $10.9bn vs. $10.84 expected. Reporting post-close were Netflix (-5.6% post-market) and Tesla (+0.2% post market).

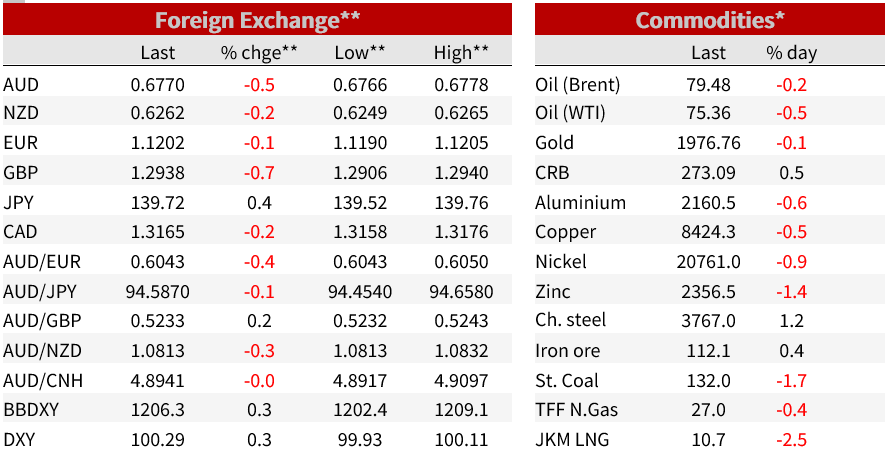

In FX, GBP fell -0.8% in reaction to the softer than expected inflation figures alongside the fall in Gilt yields. The US Dollar made broad-based gains with the DXY +0.3%, consolidating after the large fall last week. The DXY will encounter resistance at 100.85 which formed the previous 2023 range base. Major pairs are broadly in line with the USD strength seen overnight with EUR -0.1%, AUD -0.4%, NZD -0.3% and USD/JPY +0.4%.

As for the data in detail, UK CPI was softer than expected on both the Headline (7.9% y/y vs, 8.2% expected and 8.7% previously) and Core (6.9% y/y vs. 7.1% consensus and 7.1% previously). This represented the first downside surprise in five months and is the largest deviation from consensus in two years. Whether that suggests the BoE may be finally gaining traction with rate rises is unclear, though markets have certainly taken it as a sign of a broad-based downturn in inflation, reassessing how high the BoE may need to take the Bank Rate. Terminal Bank Rate pricing has fallen by around 20bps to 5.80% by February from 6.0% yesterday. As for the August BoE meeting, markets now price a 44% chance of a 50bp rise in August, down from 70% previously. Elevated wage growth will remain a concern for policy makers, which could keep underlying inflation pressures high, and recall wages excluding bonuses rose 7.3% y/y in May.

BoE Deputy Governor Ramsden declined to add any interpretation to the CPI numbers, instead repeating that inflation remains “much too high”. Ramsden spoke on QT and said he saw scope for a step up in the pace of shrinking the balance sheet. He said officials are “quite keen to create headroom where I can, so that you don’t just get this kind of ratcheting up of the bank’s balance sheet.” He’s also wary of the BOE’s purchases “creating distortions in that market .” As for the impact of QT so far, he estimates the around £80 billion in sales this year translates into 10 basis points on yields. The BoE is set to make a decision on QT at the start of October, with the bias seemingly to a larger envelope (see BoE: Quantitative tightening: the story so far − speech by Dave Ramsden).

There was also some second-tier US housing data that came in softer than expected. Housing Starts were 1,434k vs. 1480 expected, and Permits were 1,440k vs. 1,500 expected. The data is incredibly volatile month to month and comes after very strong figures last month which were revised down a little (prior month Housing Starts revised down to 1,559k from an initially reported 1,631k).

Lastly, across the Ditch, New Zealand Q2 slowed to 6.0% y/y from 6.7% in Q1 which was marginally higher than the consensus estimate of 5.9%. The RBNZ had forecast an annual increase of 6.1% at the May Monetary Policy Statement (MPS). However non-tradables inflation, capturing domestic price pressures, was higher than median forecasts and the RBNZ’s projections from the MPS. A range of other core inflation estimates, including the RBNZ’s sectoral factor model, also pointed to stubborn underlying inflationary pressures. However, we don’t think that the CPI release is sufficient to alter the RBNZ’s projection from May that the OCR has reached a peak for the cycle.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.