NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Why are the Aussie and New Zealand dollars amongst the worst performers overnight?

https://soundcloud.com/user-291029717/mayhem-as-may-manoeuvres-for-her-deal

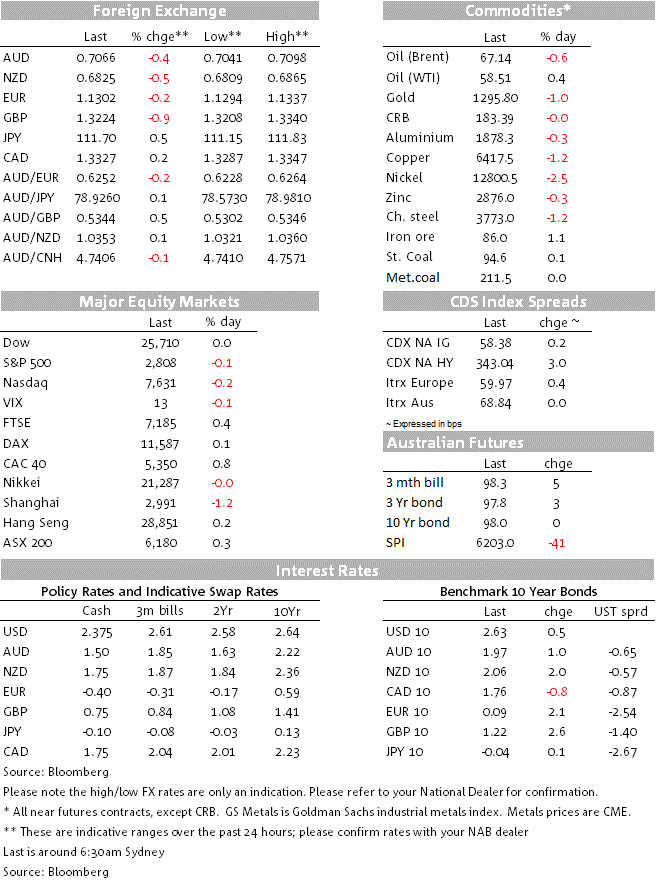

A quiet night, all things GBP included even though we now have at least some idea of ‘what happens next’ on Brexit. Risk sentiment has been (very marginally) impaired from reports that a Trump-Xi meeting is looking unlikely before late April at the earliest. The USD is weaker in DXY terms but this is largely on the back of the peeling back of the big New York afternoon Sterling gains on Wednesday, most of which occurred during our morning yesterday. AUD/USD is about 5 pips up on where Sydney left it last night at 0.7065 and NZD/USD about 10 pips lower at 0.6823.

On Brexit, the motion that has won approvals in the House of Commons 90 minutes or so ago is the one proposed by the government itself and which now gives it the authority to request two things of the EU. One is a short extension of Article 50 (through no later than June) in the event that at the third time of asking (next week) PM May manages to secure parliamentary support for her Withdrawal Agreement. The second, if this fails, is that the government would seek a lengthier extension – to allow for the formulation of a new Brexit strategy – with an understanding this would likely mean the UK having to participate in EU elections scheduled for late May.

GBP received a minor fillip on news of approval of the government’s motion, but ‘cable’ was up by no more than 20 pips and has now given back those gains and then some, hinting at a speculative market already long GBP and failing to find follow-through on the news.

Our view is that there is still plenty of upside potential for GBP from here, but still just enough uncertainty around for there to be no rush to fully price in either a soft Brexit (and quite conceivably softer than implied by May’s own withdrawal agreement) or indeed no Brexit. This is in part since the tail risks of an eventual no-deal Brexit and/or a snap General Election, still cannot be completely eliminated.

On US-China trade talks, reports earlier in the day that a Trump-Xi meeting might not take place at least until late April, but which could be expanded to a full state visit rather than just a photo-op to sign a trade deal, were greeted with some disappointment. Since then, US Treasury Secretary Steve Mnuchin has been out on CNBC confirming that there will be no Trump-Xi meeting this month at least but that he is pleased with progress on trade talks.

More telling perhaps, have been reported comments from Trump’s former chief economic adviser Gary Cohn in a Freakonomics podcast, that the U.S. is “desperate right now” for a trade pact with China as negotiators from both countries seek to reach a deal. “The president needs a win,” Cohn said and that, “The only big open issue right now that he could claim as a big win that he’d hope would have a big impact on the stock market would be a Chinese resolution,” Cohn said of a trade agreement. “Getting the trade deficit down I will never say is easy, but of the issues on the table, that’s relatively easier.”

There were no top-tier data releases overnight. US home sales for January were weaker than expected although the previous month was revised higher and there does look to be some underlying improvement here consistent with the recent fall in mortgage rates and a related pick-up in mortgage applications. Jobless claims rose slightly more than expected to a 4-week week high, with the trend in the series suggesting a modestly weaker labour market over recent months.

The data, and indeed what other news there has been as per above, has had scant impact on either US equities or bonds, US indices closing little changed on the day while Treasury yields between 2 and 10 years are within half a basis point of where they were 24 hours ago. We are though seeing a little more steepening in the 10s/30s curve, with the long bond 3bps higher at 3.045% (and following what was a fairly poor 30-year auction on Wednesday).

CH: Retail sales (y/y%), Feb: 8.2 vs. 8.2 exp.

CH: Industrial production (y/y%), Feb: 5.3 vs. 5.6 exp.

CH: Fixed assets investment (y/y%), Feb: 6.1 vs. 6.1 exp.

US: New home sales, Jan: 607 vs. 622 exp. (Jan revised to 652k from 621k).

US: Weekly jobless claims 229k (225k exp. 223k prev.)

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.