Online retail sales growth slowed in May following a fairly strong April

Insight

The new approach to China isn’t any softer.

https://soundcloud.com/user-291029717/a-new-approach-to-china-but-not-a-softer-one

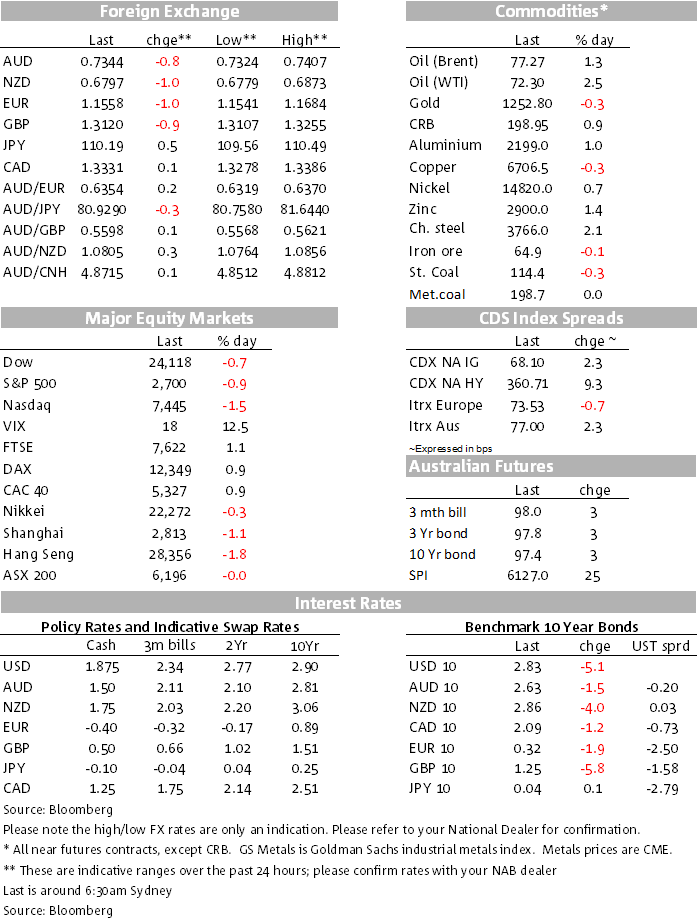

What started in the European session as a risk-positive mood with the Dax up 0.9% and the FTSE +1.1% reversed course in the US session with the Dow closing down 166 points, -0.68%, the S&P down 0.86%, and the Nasdaq off 1.54%. Flowing notably against the tide of selling were energy stocks that rose 1.34% on the back of another step up in oil prices, WTI jumping $1.85 to $72.39 (+2.62%) and Brent up $1.10 to $77.40 (+1.44%) on the back of a four times larger weekly drawdown in crude inventories in the week of 22 June, -9.891mb against the 2.572b expected decline, taking WTI to its highest level since 2014.

Reported and refocused on again overnight, President Trump confirmed yesterday’s news reports that he would use the existing committee that scrutinises foreign acquisitions of US companies to limit Chinese investments in sensitive American technologies rather than use a more confrontational approach of executive orders. As my BNZ colleague has reported this morning, that was of some comfort, but US equities reversed course after Trump’s economic advisor Larry Kudlow said that China’s reply to US trade demands has so far not been satisfactory, that Trump was not retreating on China and that the committee’s powers would be beefed up.

Adding to the further outbreak of a risk off mood was some coverage of what looked to be a worrying internal Chinese think tank report on deleveraging and liquidity that had appeared briefly on the Internet on Monday, before being removed. The National Institution for Finance & Development warned “we think China is currently very likely to see a financial panic. “Preventing its occurrence and spread should be the top priority for our financial and macroeconomic regulators over the next few years.” How much credence to give the report is not known, but it did add to negative investor sentiment.

This all comes after the Chinese monetary authorities cut the RRR over the weekend and have continued to set a higher fix for the USD/CNY above what might have been expected from day-to-day movements in the USD resulting in some net depreciation of the Chinese currency against the backdrop of trade tensions. While the AUD/USD is lower again this morning, so are other major crosses that have lost ground to a resurgent USD, the DXY index up 0.67% to 95.316 in what has turned out to be a night for a stronger dollar/ weaker China risk.

The AUD/USD is back to the lowest for the year, trading only marginally higher at 0.7340 with EM currencies down, the BRL for example off 1.75% (sugar was down 3.21% overnight) and the ZAR off 1.68%. The he NZD has had a very ordinary 24 hours, back below 0.68 (and AUD/NZD back above 1.08, though that cross has given up some gains as the NY session unfolded) thanks to a negative NZ Business Survey yesterday, the backdrop of China, and the market’s risk-off mood. Technically, on the downside, 72¼ looks to be the next level of major support for the AUD should this risk off mood persist. Note also that we are coming up to the July 6 deadline when the $34bn of US-China tariffs are due to kick in with threats of another $200bn. There’s been a small measure of NZD interest after this morning’s RBNZ on hold decision and guidance.

US durables goods orders for May were softer than expected in May, offsetting other more positive trade and inventories data also for May. The smaller than expected trade deficit for May was a nine month low and was, adding to the case for a bounce-back in net exports in Q2 GDP. As a result of this data, the latest Atlanta GDPNow estimate for Q2 GDP was pared back ever so slightly to 4½% from 4.7%. Fed hawk Rosengren (non-voter this year but is next year) said in a speech overnight that “we do need to think about is inflation picking up faster than we think” but at “if you really think expectations are really well-anchored, maybe we can take a little more risk”.

Ahead of the BoC July 12 meeting, Governor Stephen Poloz was speaking overnight running through the various positives and negatives facing the Canadian economy, trade tensions, potential growth and inflation impacts, robust business investment, still some uncertainty on housing, and so on. The market has priced in an equal risk of either a hike or leaving rates unchanged. The CAD was bid higher on net after the speech (it jagged even higher initially), having also garnered relative support overnight among the commodity currency pairs on the boost in oil prices.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.