Economic and financial market update

Insight

There’s caution in the air, but could it just be for a day?

https://soundcloud.com/user-291029717/a-risk-off-mood-just-for-today

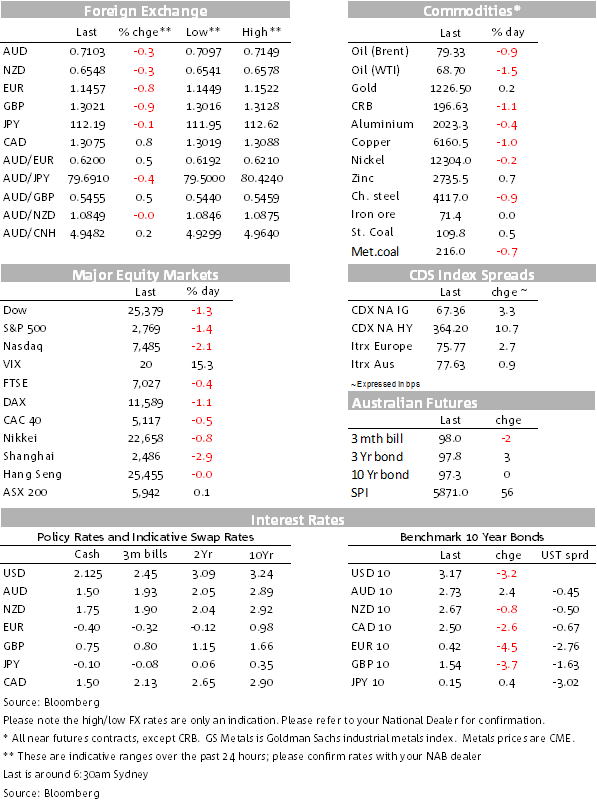

Equity market sentiment has turned sour again in the past 24 hours. The Shanghai stock market fell 2.94% yesterday (it’s down a cool 11.9% so far this month and 24.8% ytd), spilling over into softer European markets. The Eurostoxx index was down 0.51%, the E600 Banks index down 1.69% and Milan’s market off 1.89%. Not surprising then that bonds rallied, with the exception of Italy and its Southern European markets on EC officially-telegraphed concerns over Italy’s Budget plans. US main board stocks have closed softer again, the Nasdaq again leading, down 2.06% and the FAANG stocks by 2.96%.

The USD has found some more support again, though it’s been as much from softness in counterparts rather than renewed appetite for the big dollar, it seems. The Euro is looking a little brittle over Italy woes, while Sterling still has Brexit to deal with along with this week’s softer CPI and, overnight, a slight miss on Retail Sales. (Retail Sales ex fuel declined 0.8% somewhat weaker than the -0.4% consensus.) The CAD is being held back by further softness in oil prices (as is NOK the more so), while the souring of risk sentiment has weighed on the AUD and to a lesser extent, the NZD.

Despite a 3 point rise in the VIX overnight to 20.55 and for a time some softness in the RMB, the AUD edging lower but toward 0.71, testing lower in sympathy with equity market volatility. The Yen has out-performed overnight, while the Swiss Franc has been steady. Chinese growth numbers loom today for the AUD.

EU Commissioners Dombrovskis and Moscovici sent a “please explain” letter to Italian Finance Minister Tria noting that Italy’s fiscal plans for 2019 constitute “an obvious significant deviation” from EU rules. The size of the deviation from the structural improvement of 0.6% of GDP recommended by the EU Council is “unprecedented in the history” of the Stability and Growth Pact (big words!), the EU Commission warning of “particularly serious non-compliance” with EU fiscal rules. The EC is seeking a response by noon (European time), Monday Oct. 22

This has seen pressure on Italian short end and term bond markets, the Italian 2y yield jumping 17.5bps to 1.523% (Germany’s is -0.616%) and 10s up 13.8bps to 3.686. BTP 10s are back to their highs. Spanish, Portuguese, and Greek bond yields also rose in high grade market where there was some switch from equities to bonds.

The economic news out of the US continued to reflect growth momentum. The Philly Fed index for October printed at a still strong 22.2, almost unchanged from 22.9 and slightly above consensus, while weekly jobless claims were a still very low 210K (in line with consensus) and still pointing to a job market that’s as tight as it’s been since Neil Armstrong walked on the moon for those of us old enough recalling that grainy black and white TV vision. The Conference Board’s Leading Index rose 0.5% in September, up at a 6m annualised pace of 5.6% still pointing to a solid growth outlook. Next month, stocks will be something of a headwind, one of the ten components along with the yield curve.

Uber-monetary policy dove St Louis Fed President Bullard was speaking overnight and again he was extolling the virtues of leaving rates on hold in his usual methodological manner. To support his view, he presented a paper on a re-stylised R-star, the neutral real Fed funds rate. (You can see his paper here.) His thesis is that the economy’s growth spillover to inflation has been severely attenuated (a flatter Phillips curve) by a factor of 10. He also suggests using real-time inflationary expectations to calibrate inflation. Time will tell who is right. Bullard is not a voter this year but will be next and no doubt will be one of the “couple” of FOMC members cited in the Minutes who don’t favour rates moving into restrictive territory.

Fed Governor Quarles was also speaking and among other comments noted the significant doubt around the level of the NAIRU and that the Fed can gradually raise rates without becoming restrictive. As we noted yesterday, the median FOMC estimate of the accommodative/restrictive rates border is 2¾-3%.

Commodities were generally softer overnight, again led by WTI off 1.45% to $68.74 and Brent down 0.89% to $79.34. Base metals were lower, gold marginally so, while the bulks were mixed, iron ore pulling back after a recent rally.

Also:

Tonight:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.