NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US equities reversed their declines with a sharp rise overnight, ahead of today’s GDP numbers.

https://soundcloud.com/user-291029717/a-swift-reversal-in-choppy-waters

The long and winding road, that leads to your door – The Beatles

After yesterday’s big drop, European and US equities have rebounded overnight with tech shares leading the gains. As expected and in spite of recent softer activity readings, the ECB has retained it policy guidance and remains on the long and winding road that leads to the end QE by the end of this year. Draghi played down the risks to the economic outlook, but his Euro uplift proved to be short lived. USD indices have remained on the ascendency with GBP the big underperformer while AUD and NZD hold their ground. The improvement in risk sentiment lifted UST treasury yields with the belly of the curve leading the way.

Apart from watching the equity market, last night’s ECB meeting was the other focus for markets. As expected, the ECB left rates on hold and made no changes to its forward guidance, the Bank is still set to end its quantitative easing programme at the end of the year and rates are still expected to remain on hold “through the summer of 2019”. Draghi’s killer quotes is that he still sees risks as “broadly balanced” and sees “no sense that we should doubt our confidence that inflation is gradually converging to our aim” adding that “ The labour market is becoming tighter and recent wage increases are here to stay”.

Draghi attributed the most recent weakness to sector- and country-specific factors which are seen as temporary and highlighted the emission regulation on the car industry in Germany as one example. Interestingly, Draghi suggested that these factors may continue to weigh in the near future, so although temporary they are likely to last a bit longer than expected. Nevertheless, the ECB reiterated that, despite the recent moderation, consumption and business investment remain strong, supporting the expansion going forward.

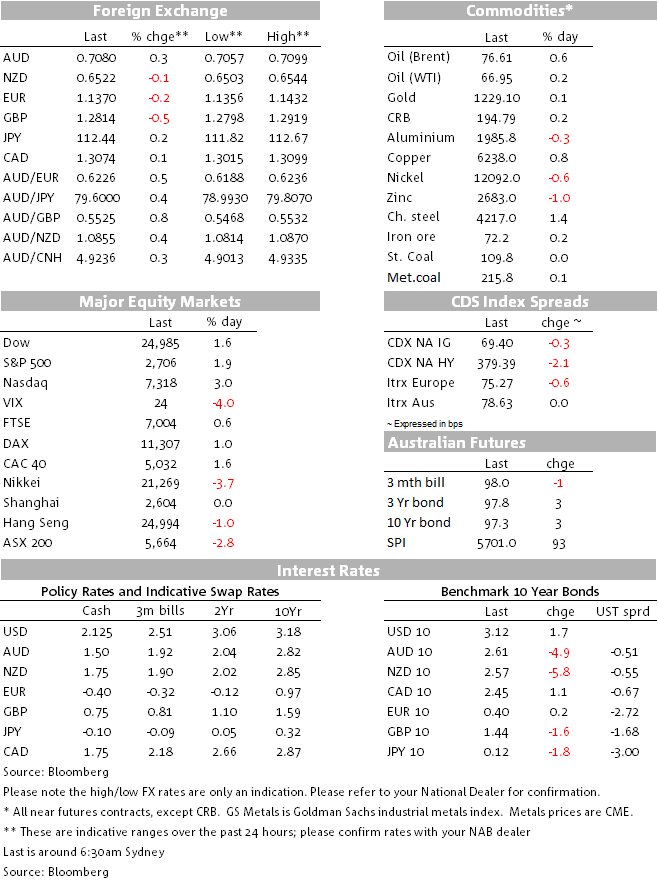

The Euro was briefly boosted by Draghi’s comments, reaching an overnight high of 1.1432, but it seems that the market remains unconvinced on Draghi’s views that the risk to the outlook remain “broadly balanced”. The pair now trade at 1.1370, 10 pips above the overnight lows. Technically the Euro is in no man’s land and it seems that the market wants to test the August low of 1.1301 before a material rebound can ensue.

Meanwhile and in part reflecting Euro weakness, the USD remains bid with the break of technical resistance in BBDXY at 1200 favouring an extension of the current move higher. DXY, the narrower USD index, currently trades at 96.625, 10pips below the YTD high. GBP is the big G10 loser with the pair now trading at 1.2817, after briefly trading below the figure overnight. It seems that at the moment no news are bad news for the pound, the clock keeps on ticking and politicians remain unable to find a solution to the Brexit deadlock(s).

AUD and NZD again remain comfortably trading within recent ranges. Relative to yesterday’s level’s the Kiwi is a tad lower (-0.17%) at 0.6522 and AUD is a tad stronger (+0.33%) at 0.7080. Both currencies are typically quite sensitive to risk aversion, but the recent spike in equity volatility has not translated into downward pressure for either of these currencies. That said history would suggest that if equity volatility remains elevated then it is still reasonable to expect both AUD and NZD to eventually succumb to this pressure.

After yesterday’s more than 3% fall, the S&P500 has today closed at 1.86%, with some attributing this to better earnings results from familiar names like Twitter, Microsoft and Tesla, but the reality is that we’re just in a more volatile trading environment, so more time is needed to say with some certainty that a recovery now looks to be in place. European bourses were also positive, with the Euro Stoxx 600 index up 0.5% and Germany’s DAX up 1.0%.

The US rates market has largely followed US equities, with the rebound in equities seeing the 10-year rate push up to 3.14%, up 4bps for the day and reversing some of yesterday’s decline. The move higher in yields has been led by the belly of the curve, overnight the 7y auction tailed slightly and featured the lowest direct bidding stats since 2011.

Commodities are mostly falt to a little bit stronger with oil prices at the top of the leader board, up just under 1%. Metal prices are little changed and Zinc is the big loser, down 0.98%.

New vice-chair of the Fed, Clarida, gave his first speech on monetary policy and he gave a fairly upbeat view on the US economic outlook, with a positive view on productivity, business investment and the labour market, seeing scope for stronger jobs without generating inflationary pressures. On rates he looked to stick to the line of the FOMC, in saying “I believe some further gradual adjustment in the policy rate range will likely be appropriate”.

WSJ reported that the US is refusing to resume trade negotiations with China until Beijing comes up with a concrete proposal to address Washington’s complaints about forced technology transfers and other economic issues, according to officials on both sides of the Pacific. One White House official said that if China wanted a meaningful meeting between Trump and Xi at the November G20 meeting, then there needs to be some groundwork and without that it’s hard to see the meeting being fruitful. China is reluctant to propose anything until further discussions have taken place, so there’s a bit of a stand-off there.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.