Total spending grew 0.9% in June.

It’s a sea of red for shares this morning. How much of this is down to Larry Kudlow’s comment that there’s a “pretty sizeable distance to go” before trade issues are resolved with China?

https://soundcloud.com/user-291029717/a-way-to-go-for-growth-and-that-trade-deal

It’s a sea of red in risk markets overnight, equities down in Europe and the US, the Eurostoxx 600 index down 1.49% and as we write the US main boards are all down by more than 1%, the mood damped by a combination of no near term resolution to the trade wars and economy growth forecast downgrades coming out of the EC and the Bank of England. That all came with comments from White House economic adviser Kudlow that there is a “sizeable distance” between the US and China over trade.

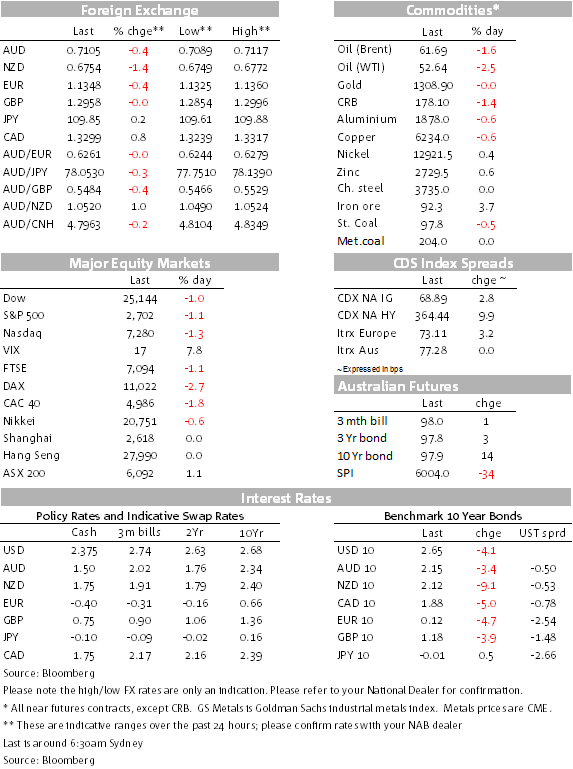

Against some further incremental support for the big dollar, the AUD has continued to drift lower. The softer than expected labour market report out of NZ yesterday added a little more weight into the antipodean currencies’ saddlebags. The NZD took the brunt of that news (supporting AUD/NZD), but it also weighed on AUD sentiment, the AUD/USD trading sub 0.71 yesterday afternoon APAC time. This sell side weight came in the wake of the RBA’s growth downgrade on Tuesday and Governor Lowe making clear in his speech Wednesday that the RBA’s latent monetary policy bias has now become balanced, the RBA considering upside and downside scenarios for growth.

The Euro and Sterling have had whippy nights, but if we’d come in this morning knowing for sure what we do about the official growth forecast downgrades, associated EUR and GBP currency weakness would not have surprised. Both the European Commission and the Bank of England took the knife to their outlooks, both revising down their growth outlook for this year by around ½%. The EC cut its German, France, and Italian forecasts, the latter by 1% to a barely visible 0.2%, a repeat of last year’s 0.1% performance after their fiscal woes. Lower Italian growth will only hamper their chances of getting to their budget target; getting there would require tighter policy. Growth for the EC was cut by 0.6% points from 1.9% to 1.3%.

Adding some real-time force to how this slower economy is playing out, German industrial production in December disappointed expectations at -0.4%/-3.9% against the consensus forecast of 0.8%, though no one can have been too surprised given the previous day’s slide in factory orders. The decline in production was broad-based, so cannot be attributed to the softer tone in the auto industry alone. Trade is no doubt a big factor.

Joining the downgrade club, the BoE also took the scalpel to its growth outlook, not surprising given the wide array of Brexit uncertainty, catering to plan for the worst perhaps and hope for the best. The UK economy is now forecast by the BoE to grow by 1.2% this year, down from the 1.7% the Bank expected last November. At his press conference, Governor Carney spoke of how Brexit was cascading through the UK economy, rattling companies and consumers. He also spoke of how after the “fog of Brexit” has cleared, the BoE would be looking at a rate rise in the next couple of years, though even that was scaled back from more that were expected last year. This seemed to do the trick in producing some whippy price action in Sterling, reversing some earlier sell off.

With the market beset by a risk off tone, bonds were in demand, the German 10y down 4.7bps to 0.115% and as we go to press, the US 10y also by 4.46bps to 2.65%. The short end also joined the bond party, 2s down a somewhat larger 4.69bps on the day. This comes after comments yesterday in APAC time from Fed Chair Powell at a town hall meeting that the US was in a “good place” with low unemployment and inflation near target, a tone also repeated by Quarles. Fed President Kaplan spoke overnight about time needed the clarify the outlook, speaking of one or two quarters needed.

Oil and iron ore were the big movers overnight, in opposite directions, oil down in size, WTI by 2.48% to $52.68 and Brent by 1.61% to $61.68. Kudlow’s comments seemingly threw enough cold water on the demand outlook, adding a degree of selling force to what was an already evident drift lower in the session. Copper prices in New York have not likewise plunged, currently off 0.3% a similar move to the LME session. Gold was little changed and the softs were mostly weaker.

At the other end of the scale, after Vale’s production and licensing woes, iron ore prices in Asia yesterday moved higher again on their march toward $100/t, prices now north of $90/t. The Chinese trading market returns next week, so it will be interesting to see how that market reacts.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.