NAB pushes out first rate cuts to May 2025 as “lower for longer” strategy plays out

Insight

It was mostly quiet on Friday and on the weekend, with an initial push higher in yields and sell-off in equities largely reversing later in the session.

“Take the pressure down; Cause I can feel it, it’s rising like a storm; Take hold of the wheels and turn them around; Take the pressure down”, Pressure Down, John Farnham, 1986

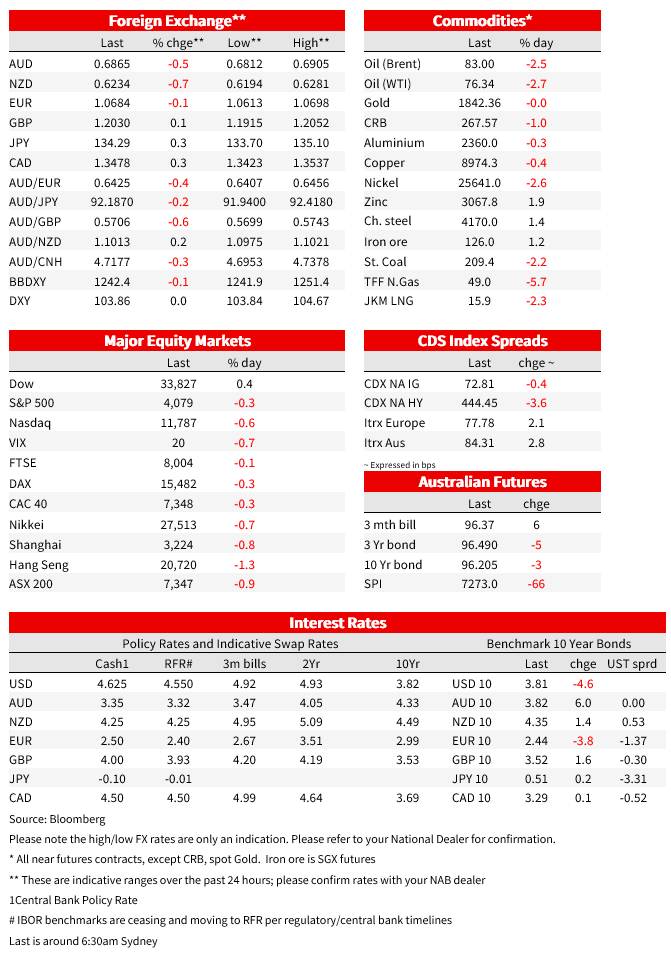

It was mostly quiet on Friday and on the weekend, with an initial push higher in yields and sell-off in equities largely reversing later in the session. Squaring and covering shorts ahead of today’s US President’s Day Holiday was cited for the reversal, as was some less hawkish messaging from the Fed’s Barkin, which talked up the merits of moving by 25bp increments, running counter to Mester and Bullard’s discussion of wanting a 50bp hike in February. The US 10yr yield at one point hit 3.93%, before more than retracing to close at 3.81%. Over the week though the 10yr yield is up 8bps. A similar story was seen in shorter-end yields with the 2yr at one point hitting 4.71%, before reversing to close at 4.62%, still up some 9.8bps on the week. Equities told a similar story with the S&P500 at one point down -1%, before paring losses to end the session -0.3%, and is also down -0.3% on the week. The USD (DXY) broadly followed the moves in yields, ending -0.1% after having been up 0.6% at one point, and is up 0.2% on the week. A similar story was seen across most pairs: GBP +0.1%; USD/JPY +0.3%; EUR -0.1%. The AUD (-0.5%) and NZD (-0.7%) underperformed with the AUD currently trading at 0.6866.

Under the surface an interesting dynamic to note is the increase in implied inflation breakevens with the 2yr breakeven now back to 2.90%, after having dipped down close to 2.0% in January, and is now back to highest levels since November. That suggests markets are taking a real signal of inflation persistence from the macro data seen since the beginning of the year. If that plays out then the call will be higher for longer and a few US investment banks have recently raised their forecasts for the Fed up by 25bps to 5.25-5.50%. Markets are currently pricing a terminal rate of around 5.28%, with only 22bps worth of cut now priced in H2 2023. The equity market so far seems sanguine about the rates outlook, seemingly taking more signal from the better than expected macro data, then from what that then means for rates and getting inflation down.

Fed speak was slightly less hawkish on Friday with the Fed’s Barkin (non-voter) advocating for moving by 25bps following last week’s discussion on the merits of a 50bp hike by Mester and Bullard. Barkin said: “I like the 25-basis-point path because I believe it gives us the flexibility to respond to the economy” and “That means I’m comfortable raising rates potentially more often to a higher level if inflation were to come in hot, and I’m comfortable backing off if inflation were to not,” “I think it’s what best balances the inherent uncertainty (in the economy) and one’s desire to do a sufficient amount to control inflation, but not to needlessly overshoot. ” The Fed’s Bowman (voter) was also speaking, noting that “I think we’ll have to continue to raise the federal funds rate until we start to see a lot more progress on that [inflation].” Former Treasury Secretary Summers (who has called this cycle) also noted “the Fed’s been trying to put the brakes on and it doesn’t look like the brakes are getting much traction’.

Across the pond, ECB speak was mixed with hawkish comments from Schnabel initially supporting a move higher in European yields, then more measured comments by Villeroy. Schnabel said: “We are still far away from claiming victory” and that “Markets are priced for perfection…They assume inflation is going to come down very quickly toward 2% and it is going to stay there, while the economy will do just fine. That would be a very good outcome, but there is a risk that inflation proves to be more persistent than is currently priced by financial markets.” In Schnabel’s view “A broad disinflation process has not even started.” In contrast Villeroy was more measured, noting “ It is likely we will reach the terminal rate by the summer, which technically ends in September” and that “there will be no automatic moves at each meeting, nor the impossibility to act afterwards if needed.”

Data was very sparse. In the UK retail sales surprised in January, with core sales up 0.4% m/m vs. -0.2% expected. The prior month though was revised down to -1.4% from -1.1%, and illustrates the widespread seasonal adjustment issues seen globally over the November, December and January period. We will have to wait for another month to have a cleaner read of the macro data globally. Meanwhile across the pond, conflicting anecdotes on the health of the consumer continues. The WSJ noted on the weekend that some 9.3% of auto loans extended to people with low credit scores were 30 or more days behind on payments at the end of last year, the highest share since 2010. With used car prices having fallen, some borrowers now owe more than their vehicles are worth. (see WSJ: More Auto Payments Are Late, Exposing Cracks in Consumer Credit).

Finally in Australia, on Friday RBA Governor Lowe gave testimony to the House Economics Committee. At the margin, Dr Lowe’s emphasis on getting inflation down being “the priority right now”, and focus on the risks of “not doing enough” may have come across as marginally more hawkish. Guidance to their being at least two more hikes was repeated in the Governor’s opening Statement – “based on the currently available information, the Board expects that further increases will be needed over the months ahead to ensure that inflation returns to target and that this period of high inflation is only temporary ” (underline added). It was also pleasing to see the RBA also took our interpretation on last week’s labour market figures (see NAB note AUS: RBA Lowe remains hawkish, perhaps marginally more hawkish given inflation “…has to be the priority right now” and for those wanting more information the official Hansard Transcript).

In Australia Q4 WPI wages on Wednesday is the key event in a week that also includes the RBA Minutes of the February meeting on Tuesday, and pre-GDP investment partials:

Offshore there are five events to watch, while it is also the one-year anniversary of Russia’s invasion of Ukraine on Friday (expectations are that Russia may launch an offensive):

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB pushes out first rate cuts to May 2025 as “lower for longer” strategy plays out

Insight

NAB’s Chief Economist, Alan Oster provides his thoughts on the Australian and Global economy.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.