Online retail sales growth slowed in May following a fairly strong April

Insight

US retail sales soared in January jumping 3% well above the consensus, 2.0% and Sales ex-autos jumped by 2.3%, more than double the consensus, 0.9%.

CH: 1-Yr MT lending facility rate, Feb: 2.75 vs 2.75 exp.

UK: CPI (y/y%), Jan: 10.1 vs 10.3 exp.

UK: CPI core (y/y%), Jan: 5.8 vs 6.2 exp.

EC: Industrial production (m/m%), Dec: -1.1 vs -0.8 exp.

US: Empire manufacturing, Feb: -5.8 vs -18 exp.

US: Retail sales (m/m%), Jan: 3.0 vs 2.0 exp.

US: Retail sales ex auto, gas (m/m%), Jan: 2.6 vs 0.9 exp.

US: Industrial production (m/m%), Jan: 0.0 vs 0.5 exp.

US: NAHB housing market index, Feb: 42 vs 37 exp.

Cause I am a champion, and you’re gonna hear me roar – Katy Perry

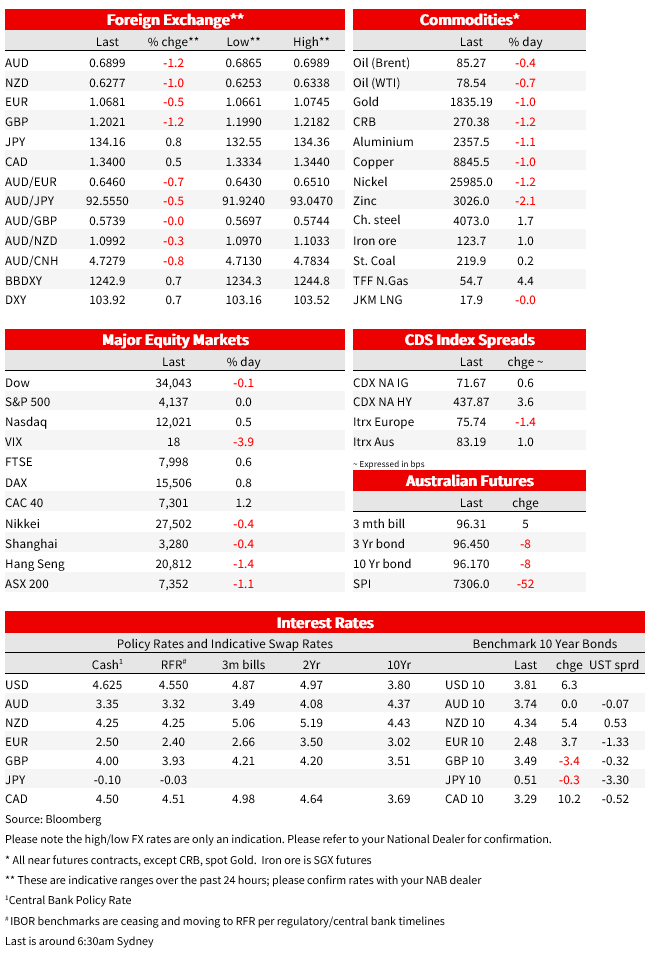

US retail sales were the data release to watch overnight, and the outcome was bombastic. After a negative print in December, the US consumer started the new year with a ravaging appetite to consume. Other US data releases also beat expectation, reinforcing the notion that the Fed has more work to do to tame inflation. US equities gapped lower at the start the session but have managed to crawl their way back into positive territory, longer dated UST yields have led a steepening of the curve with the 10y Note now above 3.80%. The USD is stronger across the board with GBP and AUD the underperformers over the past 24 hours.

US retail sales soared in January jumping 3% well above the consensus, 2.0% and Sales ex-autos jumped by 2.3%, more than double the consensus, 0.9%. There was strength across the board, with all of the retail categories within the report experiencing gains.

The headline sales were boosted by a surge in vehicle sales, up 6.4%, boosted by catch-up demand and warmer weather. Strength in retail sales figures have been supported by a strong labour market that saw a net increase of 517k new jobs in January and as noted by the NY Consumer survey earlier in the week, the US consumer is not worried about losing their job. Also supporting retail consumption, the WSJ notes the increase in social security checks which jumped 8.7% in January, following the Social Security Administration decision to increase the benefit due to inflation in 2022 and its impact on the cost-of-living, this was the biggest adjustment in four decades. That means that roughly 70 million people suddenly had more money at the start of the year. The fading of the pandemic as covid cases continue to decline and more people going and enjoy themselves (food services and drinking places recorded the biggest rise in sales during the month 7.2%) played their part too.

In other US economic news, US homebuilder sentiment rose in February by the most since mid-2020 (NAHB/Wells Fargo index gained 7 points to 42), as easing mortgage rates over the past several months have boosted the housing market. US industrial production was flat but was held down by an 8.9% plunge in utilities output on reduced demand for heating. Also beating expectations, the US Empire manufacturing index rebounded by 27 points to a still negative reading of -5.8 , well above the -18 expected by economists. The balance of US data has seen the Atlanta Fed increase its Q1 GDPNow estimate to 2.4% from 2.2%.

For now, the main take way is that the US consumer remains in rude health and with inflation still too high for comfort, the Fed has no alternative but to keep lifting the funds rate . The recent flow of strong US data releases has resulted in a reassessment of near-term Fed hiking expectations with the Funds rate now seen at 5.245% by the July 26th meeting (up ~40bps since the start of the month). Of note too, the market for now still retains the expectations the Fed will be easing policy before the end of 2023 with the funds rate seen at 5.072% in December this year.

Looking at US treasury yields, reaction to the data triggered a steepening of the curve with the move led by longer dated tenors. The 30y Bond gained 9bps to 3.862% while the 10y Note is up by 7bps to 3.81%. Of note the increase in near term Fed rate expectations did not result in a rise in the 2y Note, essentially unchanged at 4.622%, with near term rate expectations lifting followed by expectations of rates decline from late 2023 and 2024.

The good economic news initially triggered a selloff in equities with both the S&P 500 and the NASDAQ falling at the start of the overnight session, but the move proved short lived with both indices now back above positive territory . After falling close to 0.75% the S&P 500 now trades 0.12% on the day while the NASDAQ is 0.76%. Looking at S&P 500 main sector performance, Consumer Services and Discretionary stocks are up by 0.87% and 0.67% while Energy stocks are the underperformers down ~2%. Oil futures have struggled to perform (down and then up to be unchanged on the day) after EIA reported that crude inventories rose over 16m/b last week. Devon Energy Corp. fell as much as 12% after fourth-quarter earnings missed estimates.

Moving to currencies, the USD is stronger across the board with the DXY index up 0.71% and now toying with a move above 104, gains overnight are improving the technical picture for the index with little resistance seen before levels close to 105. Looking at G10 pairs, GBP (now @1.2023) and AUD (@ 0.6901) are the notable underperformers, down 1.29% and 1.27% respectively.

The move lower in GBP was triggered by a meaningful downward surprise to the UK inflation report for January. UK CPI fell by more than expected during the month, with annual inflation easing to 10.1% and under the 10.3% consensus. UK CPI inflation is now down a full percentage point from its 41-year high of 11.1% peak back in October last year. The inflation downside surprise was reinforced by the core measure falling to 5.8%, well under the 6.2% expected, and the first clear step lower from the 6.5% peak back in September. Still too high, but more definite signs of moving in the right direction helped by lower petrol prices.

Supporting GBP’s underperformance, UK Gilt yields buck the global trend higher, with the 10-year yield down 3bps and shorter-end yields down 6-8bps, unwinding some of the previous day’s large gains following the strong labour market data.

The AUD underperformance began yesterday as the market continued to digest the implications from the US CPI release while declines in APAC equity indices didn’t help the AUD either. AU swap rates and AUD pushed lower on the day but that was probably more on souring risk sentiment which extended through the overnight session. The AUD still has some support around the 0.6850/80 area, but with the USD in the ascendency, the AUD is certainly looking vulnerable.

The NZD drifted down toward 0.63 yesterday and has slipped below that mark overnight amid ebbing risk sentiment and USD strength. The NZD dipped to its lowest level since early in the New Year, looking down toward 0.6250, before steadying around 0.6279 currently, down ~1% on the day.

The euro has not escaped the USD ascendency, down 0.56% over the past 24 hours to 1.0682 while USD/JPY is now at ¥134.18, up another big figure over the past 24 hours. Speaking overnight, ECB President Lagarde reiterated that Bank intends to raise borrowing costs by another half-point next month given the current strength of underlying inflation.

In other news, the nonpartisan Congressional Budget Office (CBO) said the US could become unable to pay all of its bills on time sometime between July and September, so a bit sooner than many expect, the estimate still leaves lawmakers plenty of time to come to an agreement before the US contemplates the prospect of defaulting on its debt.

Finally, after news Fed Vice Chair Brainard will be taking on the government position of director of the National Economic Council as early as next week. The WSJ notes the White House is considering nominating Austan Goolsbee, who became president of the Chicago Fed last month, to serve as vice chair of the Federal Reserve’s board of governors. Goolsbee voted for a 25bps hike at the Fed’s Jan. 31-Feb. 1 meeting.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.