A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

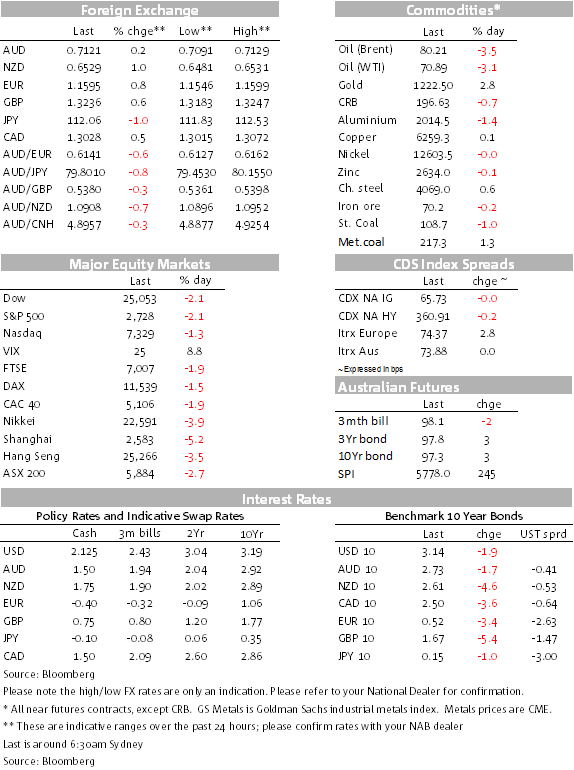

Equity markets took another hammering overnight.

https://soundcloud.com/user-291029717/another-night-of-the-long-knives

It’s been another volatile overnight session, European stocks taking over where Asia left off yesterday, the Eurostoxx 600 down 1.98% with the FTSE, DAX, and CAC-40 all down by between 1½-2%. The US market has been in the red for most of the session, the market making it back to square mid-session before more selling re-emerged in the last two hours of trade. At its intraday low, the Dow was down close to 700 points, and has closed down 546 points, down 2.13%. The market is still struggling with lofty valuations and all the other factors such as US-China trade and political tensions, elevated oil prices and the restraining effect of higher US rates and yields.

There has not been a full-blown risk off event across asset classes – that while equities have been under pressure again, currencies, bond market, and credit indices have seen contained moves and in some cases with tinges of “risk-on”. For FX, there has not been a further increase in the USD. It’s been the opposite, the DXY off a net 0.20% since last APAC time yesterday and the spot Bloomberg DXY index down 0.31%. The AUD/USD made its way back above 0.71, trading at 0.7120/25 as this note goes to press, having tested 0.7105 in the past two hours, and despite a very choppy last hour or two for US stocks.

Most major currencies have made some net gains against the USD, the exceptions being the Swiss Franc and the Japanese Yen, though to be technically fair, the yen is up marginally since late yesterday, up 0.05%, but the CHF is off 0.28%. The best performers have been Kiwi (+0.75%) and Aussie (+0.60%) more symptomatic of risk-on rather than risk-off and perhaps reflecting an already short market and long USD.

It’s been a similar story for bond yields with yields not gapping 10-15bps lower in yield that a risk-off sizeable rally might fuel, but more measured, incremental moves. German 10y bund yields closed down 3.4bps to 0.518, while US 10s have declined a marginal 2 bps to 3.1423% and despite a still choppy end to the session for US equities.

US 2y yields have actually risen slightly, up 0.4bps. January 19 Fed funds futures have eased by 1 bps, the market continuing to price in an over 80% likelihood that the Fed will again hike in at its December 19 meeting (when there’ll be a full dot points/forecasts refresh) after taking a break at its forthcoming 8 November meeting.

President Trump has been railing further against the Fed, saying that the market plunge is a correction that he thinks is caused by the Federal Reserve. He said that the Fed was “going loco”, but that he wasn’t going to fire Jay Powell, just expressing disappointment. “I think it’s far too fast, far too rigid”, that the rate rises are “not necessary in my opinion and I think I think I know about it better than they do. “The Fed is out of control,” “I think what they’re doing is wrong.” While being especially open and free with his comments, he’s not the first President to be disappointed with Fed actions and no doubt won’t be the last.

There was certainly no US September CPI-inspired sell off. The headline and core CPI both missed consensus by one tenth, the miss in the core CPI attributed to an out-sized decline in used car prices, the largest such decline in 15 years after the large unexpected decline in apparel prices last month. Yes, a one-off, and will only add to the Fed continuing on with its path of gradual rate rises up to around its neutral rate.

Esther George, Kansas City Fed President has been on the wires (she’s doesn’t get a vote this year, but will next year, as will James Bullard at the other end of the policy spectrum) noting trade uncertainties but also speaking of inflation risks from fiscal policy and accommodative monetary policy settings.

Again, the biggest move was in oil, to the downside again, the US EIA revealing a larger than expected weekly jump in crude inventories, up 5.987mb, above the 2.173mb expected and following a 7.975mb rise the previous week. WTI and Brent were both down by over 3%, WTI and Brent both now closer to $70/$80 respectively. Again bucking equities, copper rose marginally, but other base metals dipped. Bulk commodities were mixed, iron ore and steel prices higher. For once, gold had a big move, this one to the top side, up $34/oz, +2.87%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.