Total spending grew 0.9% in June.

Mario Draghi is preparing to chair his last ECB meeting, with no expectation he will move rates.

https://soundcloud.com/user-291029717/au-revoir-draghi-bonjour-uk-election?in=user-291029717/sets/the-morning-call

The Radiohead song from the ‘Kid A’ album was originally titled Lost at Sea, containing references to the UK shipping forecast, including for the Irish Sea, where the UK government proposes to position a new border between Britain and the EU and so dividing the British mainland form Northern Ireland. In Limbo just about sums up where are we are with Brexit this morning and the best I can do by way of musical analogy following what has been a soporific offshore session for global markets.

Media sources are reporting that EU ambassadors to all 27 member states are supportive of another Article 50 extension, which is to be formally discuss on Friday. This is likely to be for three months – against the wishes of Boris Johnson – unless an agreement is reached facilitating an earlier Brexit. In the meantime, the UK PM is no doubt weighing up next steps, his chances of getting an election, etc.. A meeting between him and Labour opposition leader Jeremy Corbyn on Wednesday came to nothing, according to the BBC.

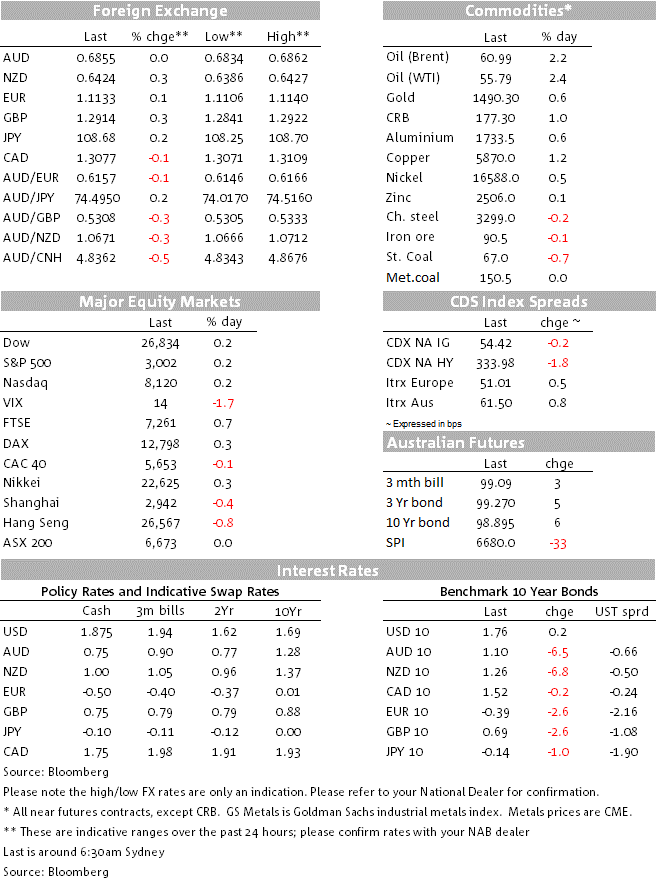

Sterling is actually the best performing G10 currency in the last 24 hours, so fully recovering about half of the one and a half cent drop against the US dollar in Tuesday’s late New York day trade, following the parliamentary defeat of the government motion to limit debate on the Withdrawal Agreement Bill to just three days. Elsewhere in FX, NOK is the next best performing of the majors, +0.3%, and CAD is also a touch firmer (+0.2%) in the wake of Monday’s better than expected showing by Justin Trudeau’s Liberal party, seen to leave it a bit less beholden to the left-leaning minority opposition party. Common to gains for both currencies is smartly higher oil prices (+$1.33-1.36) after the EIA reported an unexpected 1.7mn barrels draw on crude inventory stocks last week.

0.3% vs. no change for AUD in the last 24 hours so meaning the AUD/NZD cross is now some 1.25% lower since the middle of last week to sit below 1.07. It does though remain comfortably inside our estimated fair value range. MNI yesterday reported an interview with RBNZ Assistant Governor Hawkesby who was said to be “very happy” with the way in which interest rate cuts are feeding through into the economy, lowering borrowing rates and keeping the NZD low. And the way the article was written, Hawkesby seemed quite joyous about the evident rise in house prices. The same might be said here for the RBA, where higher asset prices are seen to be one of the primary transmission mechanisms from easier monetary policy through to the real economy. There’s another Terry McCrann article out apparently (I haven’t read it) making the case for the RBA keeping rates steady rather than cutting them further.

The mainboard indices all just closing with gains of between 0.2% and 0.3%. In a classic example of taking a glass half full approach to incoming corporate earnings, Caterpillar’s stock is up 1% after missing both its Q3 EPS and revenue estimate and lowering its full year guidance. But the stock rose reportedly on announced plans to cut back in production in response to weaker demand. That’s alright then.

Bond markets are barely showing a pulse following decent rise in yields earlier in the week, US 10-year Treasuries up 0.5bps to 1.766% and 2s +1bp to 1.586%. Earlier European bond yields closed very narrowly mixed.

Eurozone ‘flash’ October PMI releases dominate the economic agenda today. Small improvements across France, Germany and pan-Eurozone and for both manufacturing, services and composite readings are the consensus expectation and the EUR will be sensitive to deviations one side or the other of this.

The ECB meets for what is Mario Draghi’s swansong meeting and post-meeting press conference. The meeting itself is an ‘interim’ one at which changes in monetary policy settings are not typically discussed or at least agreed. Draghi will no doubt underline for the need for the recent policy shift, especially as the macroeconomic situation continues to deteriorate and EU government’s continue to display reluctance to share the easing burden. He will doubtless be quizzed on the reported internal policy differences that emerged after this month’s decision to restart QE.

US durable goods orders (expected -0.7% in headline terms) and weekly jobless claims feature in the US. Amazon reports its earnings after the close, so 6:00 AEDT on Friday

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.