Coming in for landing in a heavy cross wind

Insight

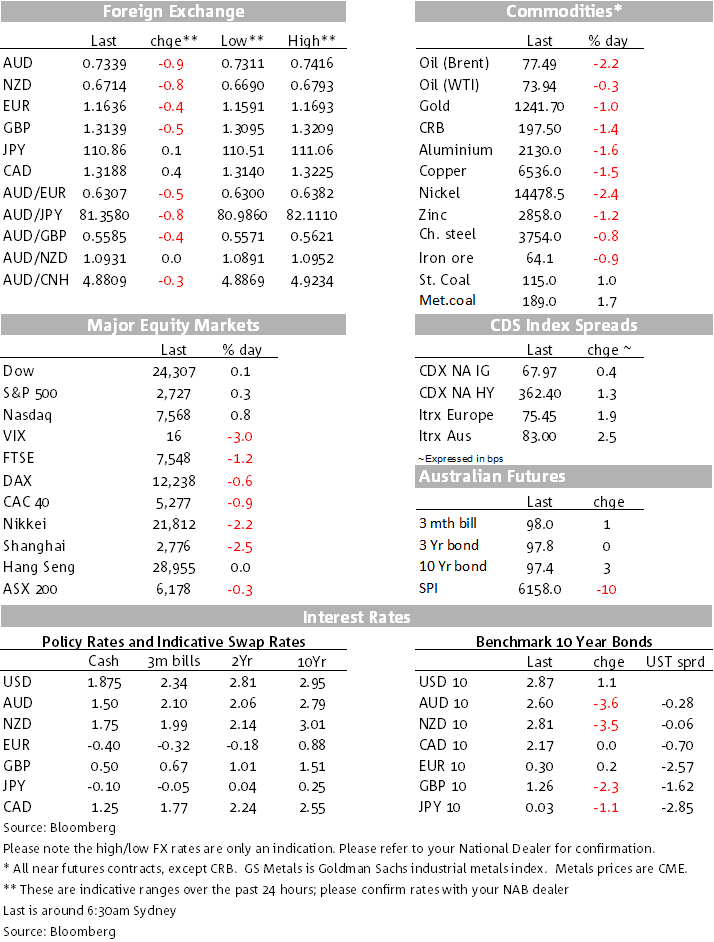

The Aussie and Kiwi dollar were two of the worst performing currencies overnight.

https://soundcloud.com/user-291029717/aussie-and-kiwi-dollar-hit-by-a-hat-trick-of-uncertainty

Political uncertainty in Germany and escalating tensions on global trade, centred around President Trump’s policies and possible retaliatory action appear to have been sufficient to hog the headlines and dog sentiment for a good part of the overnight session, coming with no horrors at all from the data. The scene was set in part from the local trading session yesterday, Asian equity markets fell and futures for European and US markets declined. Overnight, the euro-area’s EuroStoxx 600 declined by 0.8%. The S&P 500 was down 0.6% earlier this morning but by the end of the session had scrambled back to positive territory. The LMEX index was down 1.51%, the AUD was testing toward 0.73, but has since “recovered” to 0.7338. The AUD and the NZD are both lower by the best part of one percent.

On German politics, Merkel has been meeting the Bavarian coalition leader of the CSU party Seehofer, a result being either no change to the status quo, allowing Merkel to govern, or a break-up that could see Merkel run a minority government or call fresh elections. In news earlier this morning, Herr Seehofer says that the coalition CDU/CSU has reached agreement over migration, EUR positive, also providing some support to the Aussie.

There have been no major developments on the global trade front. It still all looks very uncertain, with President Trump expected to impose the promised extra tariffs on the specified $34b of China imports at the end of the week and China set to match that with retaliatory action, followed by another $200bn from the US side more than half promised. Meanwhile, the EU is preparing its moves against Trump’s threats to put tariffs on the auto sector.

A late turnaround in the S&P500 might reflect some more positive comments by Trump to reporters this morning, saying he’s close to making a “fair” trade deal with the EU. He also said that he isn’t planning anything on WTO membership for now but may do if the organisation isn’t fair to the US – a response to a weekend report that the US was looking to ignore WTO trade rules, effectively withdrawing.

The economic news from yesterday and overnight has done nothing materially to frighten the horses. China’s Caixin manufacturing data was only marginally softer than expected, final manufacturing PMI data for the euro area was revised down trivially (from 55.0 from 54.9), Japan’s Tankan large manufacturer’s index was only marginally weaker than expected (21 cf 22 expected), all very small misses.

By contrast the US manufacturing PMI was much stronger than expected, but largely driven by one component, slower supplier deliveries, a sign of further capacity constraints and therefore inflationary pressure in the economy. In any case, it’s still a strong figure; the new orders index was a very handy 63.5, so business is hardly slowing. This news might be behind US Treasury yields not falling in an environment that had tinges of risk-off. The 2-year rate is up 2bps to 2.55% while the 10-year rate is up one basis point to 2.87% after being as low as 2.82% last night. Comments in the survey showed that respondents are “overwhelmingly concerned about how tariff related activity is and will continue to affect their business”. The Atlanta Fed upped its estimate of GDPNow for Q2 to 4.1% from 3.8% after last night’s data.

All eyes now on the RBA for what they say on the state of the core economy but particular attention to potential swing factors, notably funding costs (one to watch in the days and weeks ahead now that the end of the financial year has passed), trade tensions (more looming), and the domestic housing market that appears to be still cooling and market speculation of out of cycle rate rises. The RBA would certainly be content that the AUD is doing some heavy lifting in terms of supporting Australian export sectors.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.