Online retail sales growth slowed in May following a fairly strong April

Insight

The rising US dollar is playing havoc on emerging market currencies and the Aussie has got tied up in the bad news.

https://soundcloud.com/user-291029717/aussie-down-and-staying-there

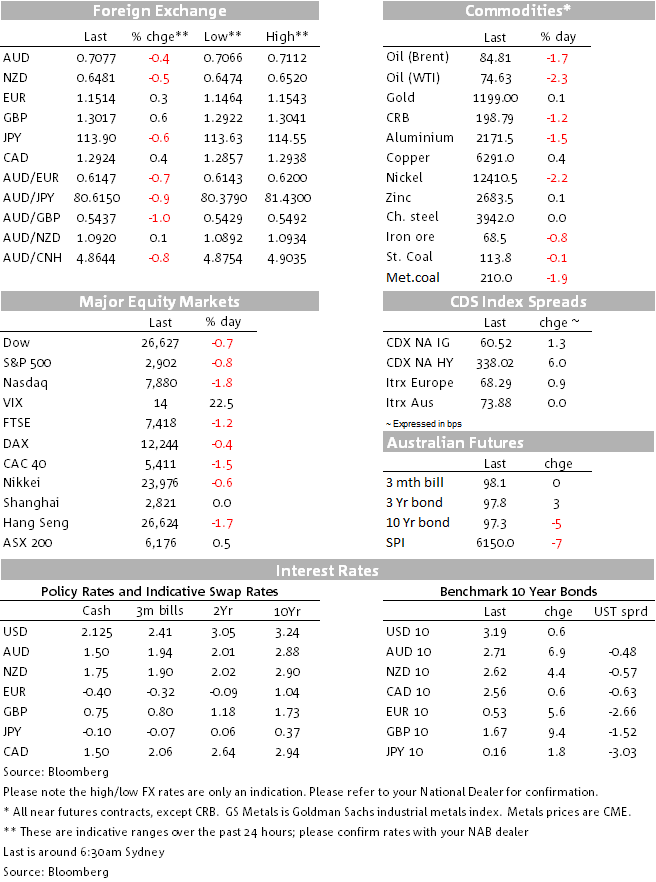

Jay Powell’s remarks late in the New York day on Wednesday suggesting that the Fed is still a long way from neutral, have continued to reverberate around global markets in the last 24 hours, compounding the earlier US data-inspired rise in bond yields. The latter are now hurting rather than helping US equities or so it seems, while the contagion effects into Emerging Markets from the rising US yields/rising USD backdrop – in Asia especially yesterday – have meant that AUD/USD has made a new post-March 2016 low, of 0.7066.

On Wednesday night, or at least right up until the last hour or so of New York trading, rising US bond yields and rising US equities were happy bedfellows, justified on the basis that the undeniable strength of the US economy evident in incoming data means that US corporate earnings should continue to rise at a sufficient rate to more than offset the negative impact on valuations associated with a rising ‘risk free’ interest rate.

That may be so, but the rise on 10-year bonds yields from around 3.15% at Wednesday’s US equity close to a high of 3.23% in Thursday’s offshore trading, does look as though it has spooked equities somewhat. We might add into the mix the Bloomberg story published yesterday titled “The Big Hack: How China Used a Tiny Chip To Infiltrate US Companies”, which you can read here.

This plays heavily into the view that the Sino-US trade stoush is not just about Trump’s infatuation with the size of the US-China bilateral trade balance, but is a much more geopolitical affair (some call it the new Cold War) as well as being related to China’s desire to dominate the technology sphere in years to come (epitomised via its Made In China 2025 strategy). It means that an early resolution of Sino-US trade issued is not a realistic prospect. Anyway, suffice to say the IT sector was the biggest driver of overnight US equity weakness, down 1.8% relative to the overall 0.8% drop in the S&P500 (and bigger 1.8% fall for the NASDAQ).

From the aforementioned 3.23% cycle high seen late in our day yesterday, 10 year Treasuries have edged back down, now at 3.185% (so up less than 0.5bp on Wednesday’s NY close) while the 2-year note yield is actually 0.4bp down – so the steeper curve themes from mid-week remains in place. European bonds followed the lead from US treasuries on Thursday with Bunds ending the day 1.5bps higher, helped too by the absence of fresh upward pressure on Italian yields amid more signs of the government backtracking on earlier fiscal deficit proposals (or at least rising market confidence that they ultimately will, in order to stave off the risk of a ratings downgrade to ‘junk’):

As for Powell’s comments from late Wednesday that “we may go past neutral, but we’re a long way from neutral at this point, probably“, we don’t regard this as a change of thinking by either him or the wider FOMC relative to the just-gone FOMC meeting (last week). There, recall, the median member view of the neutral rate sat at 3% versus the current 2.0-2.25% Fed Funds target range, so effectively three rate rises away. That doesn’t seem a lot does it, though you could argue that it means the Fed is only about 70% of the way to neutral relative to zero. Semantics really, but what Powell’s remarks have done is to shift the market further toward pricing in what the Fed’s median dot profile suggest the Fed themselves think they’ll need to do in 2019 and 2020, with now about 2.2 rate hikes priced for 2019 (against the Fed’s median dot suggesting three).

Reflective of the more risk adverse market tone, now in developed as well as Emerging Markets, the Japanese yen is the second strongest G10 currency of the past 24 hours, USD/JPY down over 0.5% to just back below ¥114. Sterling has just pipped the yen to top spot, with reports that both EU officials and the (Northern Irish) DUP party that props up the Tory government, aren’t dismissing out of hand the latest suggestion for a ‘backstop’ on the thorny Irish border question that needs resolution in order to secure a Brexit Withdrawal (transition) Agreement. This in effect means at least a temporary border down the Irish Sea.

The three bottom slots on the G10 scoreboard are occupied by the NZD, CAD and AUD, all 0.4-0.5% lower with NZD just faring worse. Oil has flipped from tailwind to headwind with WTI crude off almost $2 and Brent almost $1.50 , some of the speculative froth of late seemingly being blown off. But it’s the combination of USD strength and weaker EM currencies that goes most of the way to explaining the weakness here (most of the fall in AUD to below 0.71 and in NZD to below 0.65 yesterday occurred before oil started falling. Higher/lower oil is a negative/positive for the Kiwi via the impact on its terms of trade, the opposite for the Aussie given the link to LNG prices. Other commodity prices are mixed, though base metals are mostly lower, including iron ore, as is metallurgical coal (-1.9%).

Yesterday’s NAB and BNZ lowered their forecasts for both AUD and NZD over the next there quarters, seeing limited prospect of a recovery in either currency over this period, in particular with Sino-US trade tensions liable to get a fair bit worse before they get better and, we think, a strong likelihood China will orchestrate a further, if modest, CNY depreciation next year. In the meantime, the rate gap between the US over Australia and New Zealand is set to widen further. We now characterise the likely NZD/USD range s 0.633-0.67, and while we are calling AUD a ’70-75 cents’ currency, we will not be at all surprised to see the 2016 lows near 0.68 tests in coming weeks or months.

In our time zone, the RBA’s Alex Heath is speaking in Canberra at 11:35 AEST

Offshore tonight, Germany factory orders will we worth watching after recent soft manufacturing data, while tonight it’s US (and Canada) payrolls.

US non-farm payrolls are expected to rise by 185k, also NAB’s forecast (with upside risk). As much or more attention will likely be paid to earnings after last month’s jump to 2.9% y/y. 0.3% is the NAB forecast and consensus, implying 2.8% yr/yr. The unemployment rate is seen falling to 3.8% from 3.9%, matching its post 1969 low.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.