NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

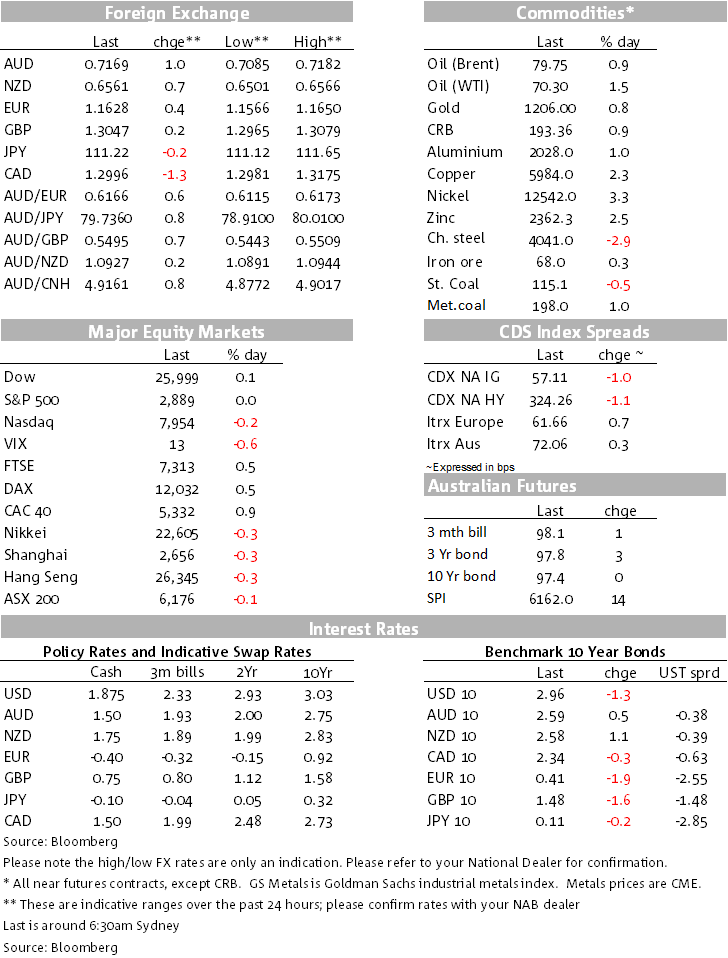

The Aussie and Kiwi dollars gained some ground helped by hopes of renewed trade talks between China and the US.

https://soundcloud.com/user-291029717/aussie-up-on-trade-hopes-oil-rallies-on-florence-approach

After teetering on the brink of 0.71 in recent days and looking to test lower levels, the market has been caught short with a sequence of more encouraging news on the trade front over the past 24 hours. The Brexit mood music has also continued to improve, adding momentum and no doubt lifting PM May’s stocks and a warm tailwind for the Pound.

The AUD sits at the top of the FX leader board, up 1.1% from yesterday’s local close, matched by a 1.1% rise in the NOK from the oil price lift, while the NZD is also up 0.9%. European equities rallied, but US equities have been choppy. An already flat US Treasury curve has flattened, 2y yields up 0.4bps but 10s down 1.29bps, capped by a miss on the August US PPI ahead of the CPI tonight and a solid Treasury auction, and notwithstanding oil’s overnight gains.

It’s been a sequence of better trade reports over the past 24 hours – we know that 24 hours can be a lifetime in this market – that’s for now flushed out some AUD shorts and USD longs. Setting the scene yesterday were words from Trump that the US-Canada trade talks are “coming along very well” and that the Canadians are willing to include dairy in the trade negotiations. Dairy is a politically sensitive issue for Trudeau and also for Trump who is looking for mid-West support from the likes of Wisconsin dairy farmers.

Mexican Economy Minister Guajardo was also on the wires saying that a US-Canada trade deal was a high chance. Then it was news that the UK and the EU were preparing for a special summit to sign a Brexit deal in November, timing expected to be announced “within days”. There were reports overnight that the EU is redrafting a new Irish border proposal, one that is more digestible to the UK.

Overnight, delivering more trade optimism momentum were reports that US Treasury Secretary Mnuchin was to lead trade talks with his Chinese counterpart Le Hui, supposedly an outreach to Beijing to get talks back on track “in coming weeks”. Whether this has the support of the man at the top is not known and we remember that the last such Mnuchin talks produced little. It’s lifted prospects that the $200b tariff rise is being put off.

In the last hour, NZ dairy gain Fonterra has announced its annual results and finalised its 2017/18 milk price at $6.69, down 1c on previous guidance, also confirming its $6.75 guidance for the current 2018/19 season. The NZD is unmoved.

Oil prices surged again as Florence approaches. WTI lifted 1.5% to $70.30 (up over $1), while Brent was also higher, by 0.83%, testing $80 and sitting just below that level this morning. While the pull back in the USD would explain some, the weekly US DoE oil report confirmed not just another draw down in crude inventories, but one that was three times market expectations, down 5.3mb after a 4.3mb draw the previous week, the market expecting a 1.58mb draw. Near term and longer dated futures contracts rose.

Gold rose 0.8%, while the LME had a better day too, the LMEX composite index up 1.99%, copper up 2.36% and nickel up 3.19%. Bulk prices were also mostly higher.

The US August headline and core PPI fell 0.1%, missing market expectations of a 0.2% increase, the miss from lower trade services prices from lower wholesaler and retailer margins, those margins accounting for nearly a quarter of the core. Whether this is transient or not, it will have made analysts wonder about tonight’s CPI and plays to the still non-threatening threads in the Fed’s Beige Book released overnight.

It reported a somewhat mixed growth report across the 12 Fed districts, that labour shortages were widely reported, but that “wage growth was mostly characterised as modest or moderate, though a number of Districts cited steep wage hikes for construction workers. Some Districts indicated that businesses were increasingly using benefits—such as vacation time, flexible schedules, and bonuses—to attract and retain workers, as well as putting more resources into training”.

Fed President Bullard and Governor Brainard were both speaking, Bullard again urging caution on further raising rates, but Brainard saying the Fed may have to raise rates to above 3% , seemingly on growth optimism. It was a hawkish comment from her. She did note that leverage lending was rising but that there was little sign of an inflation breakout.

In the end, the US Treasury curve flattened, the front end yields supported by Brainard’s comments but the PPI proving some support to the longer end on the day as did the solid Treasury auction, and despite the kick up in oil.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.