Online retail sales growth slowed in May following a fairly strong April

Insight

The markets were buoyed at the end of last week by hopes that some sort of trade deal with China was closer.

https://soundcloud.com/user-291029717/average-inflation-deal-hopes-and-a-really-big-can-kick-for-brexit

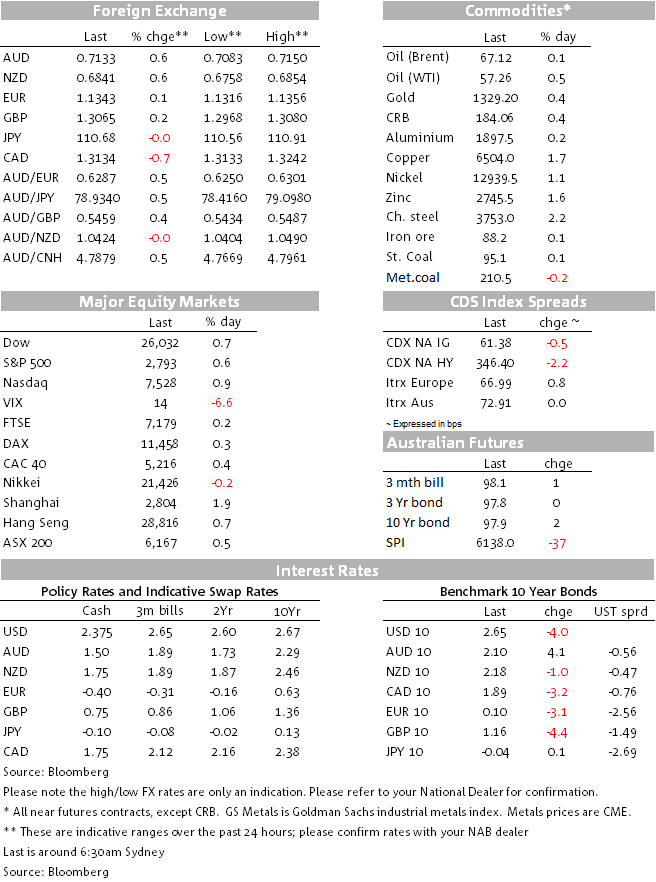

US stock market indices went out of a strong footing Friday, recovering from intra-day weakness in the last ‘hour of power’ to close near the highs, despite a 20%+ drop in the shares of Kraft-Heinz, the latter after announcing downgraded earnings estimates, write-downs and an SEC accounting investigation. The S&P 500 ended 0.66% higher at its best level since mid-November, 11.4% up YTD and now 19% back from its December 24th lows.

Rising Sino-US trade optimism was one of the factors driving positive risk sentiment Friday and sees the VIX back down onto a 13 handle and to its lowest level since October 5th (i.e. very close to the start of the Q4 equity mark rout). This, incidentally, has had the effect of pushing up our short term fair value estimate of AUD/USD by almost half a cent, currently at 0.7250.

US President Trump said Friday there was ”a very good chance” the US would strike a deal with China to end their trade dispute and that he was inclined to extend his March 1 tariff deadline and meet soon with Chinese president Xi Jinping. Chinese Vice premier Lui He in Washington for the talks and attending Trump’s press conference, agree there has been “great progress” and that “from China, we believe that (it) is very likely that it will happen and we hope that ultimately we’ll have a deal. And the Chinese side is ready to make our utmost effort”. Trump indicated he probably would meet with Xi in March in Florida to decide on the most important terms of a trade deal.

US Treasury Secretary Steve Mnuchin had earlier said the two sides had reached an agreement on currency, though reports Saturday night were that the US and China hadn’t yet agreed on the critical issue of enforcement in a proposed currency deal that would ensure Beijing lives up to its promise to not depreciate the yuan, Bloomberg said citing ‘four people familiar with the matter’.

Strength in US stocks markets on Friday was associated with lower not higher US bond yields, 10-year Treasuries lower by 4bps and 2s by 3.5bps. Relevant here is the developing Fed-speak, initiated a while back by NY Fed president John Williams, that too-low inflation risks being the Fed (and other central banks’) bug-bear in coming years.

Fed Vice Chairman Richard Clarida, on Friday in Chicago said that facing a long term environment of low interest rates and low inflation, it’s a good time for the Fed to undertake a review of how it goes about pursuing its twin goals of maximum employment and price stability. The Fed’s framework review begins with an event in Dallas on Monday and will include a research conference in Chicago in June, the conclusions of which will be published in the first half of 2020, Clarida said.

Speaking at the same event, NY Fed President John Williams said that persistently soft inflation readings could damage the Fed’s ability to convince the general public it will hit its 2% goal and keep the economy on a solid path. Central banks in other major economies are likely to face similar problems, Williams warned. “Indeed, we have seen some worrying signs of a deterioration of measures of longer-run inflation expectations in recent years”, he said. Also weighing in, SF Fed President Mary Daly agreed it was equally important to be aware of the risks of lower inflation, alongside the central bank’s more traditional task of fighting fast-rising prices.

Latest Fed speak can only serve to re-enforce the sense that the bar to the Fed resuming rate hike(s) later this year or next is quite high, notwithstanding the implicit tightening bias that showed through in last week’s Minutes of the January FOMC meeting.

In FX, it was the CAD, NZD and AUD that were the best three performing G10 currencies, amid a slightly softer USD backdrop (DXY-0.1%), the latter engendered by positive risk sentiment.

NZD fully recouped Friday’s APAC day losses – and then some – that came on the headline that “RBNZ says bank capital increase could lead to eventual rate cut”. Taken in context, the rate cut comments were quite conditional on many other factors, Deputy Governor Geoff Bascand telling reporters that “The Reserve Bank expects lenders could respond to higher capital by increasing the margins between their lending and deposit rates. If it went in the way we see it, and nothing else changed, it’s a marginal tightening in monetary conditions. If we were worried about that and thinking we have an economy that’s undershooting inflation or undershooting maximum sustainable employment, we’d offset it with an OCR cut”.

We said at the time Friday we view the 0.5% dump in the NZD as a gross overreaction (but such is the power of the abbreviated ‘red headline) and indeed NZD ended Friday night as the best performing G10 currency

Seemingly helping AUD alongside positive risk sentiment and the aforementioned drop in the VIX, China foreign ministry spokesman Geng Shuang said in a news conference Friday that ‘I would like to clarify here that these reports (that China had banned Australian coal imports) are false” . He added that “Based on my information the ports in China are all receiving declarations for imported coal, including that from Australia”. Geng did though admit that China customs were “stepping up efforts to analyse and monitor the quality and safety of imported coal”. (Bloomberg reporting).

AUD and the Australian rates market were virtually unmoved throughout Friday’s parliamentary testimony by RBA Governor Lowe, which re-iterated the ‘evenly balanced’ view of the downside and upside risk to interest rates, albeit Lowe said that it was unlikely rates would be raised this year (so implicitly admitting any move this year would only be to cut). AUD ended just over 0.5% up on Friday at 0.7128 versus a 0.6% gain for NZD and 0.7% for CAD (the latter despite some underwhelming retail sales numbers). Complementing these moves, commodity prices were almost universally higher Friday.

On Brexit, plenty of weekend developments and which see GBP starting the week about 0.1% up on where it went out of Friday. UK PM May has said she won’t now bring a vote on the ‘meaningful say’ on her Withdrawal Agreement to parliament before May 12th; but this doesn’t look like preventing the ‘Cooper Mark 2’ Amendment that would provide for an extension of Article 50, being voted on this week. There is also the suggestion of another Labour Amendment that if passed would force a 2nd Referendum. Meanwhile EU officials are suggestion that some governments want a 21-month extension of Article 50 (so into 2021) if there is no Brexit Agreement by March 29th. Everything still points to no hard Brexit on March 29th.

Japan CPI ex-fresh food 0.8% y/y (0.8%E, 0.7%P)

Germany Q4 GDP 0.0% q/q (0.0%E); y/y 0.9% (0.9%E)

Germany IFO Business climate 98.5 (98.9E, 99.3P)

EZ final Jan CPI 1.4% (1,4%E, 1.4% preliminary); core 1.1% (1.1%E, 1.1% preliminary)

UK CBI Feb retail sales 0 (5E, 0P); total distributive trades sales 14 from 13

Canada Dec retail sales -0.1% (-0.3%E, -0.9%P)

Canada retail sales ex-autos -0.5% (-0.3%E, -0.7%P)

NZ Q4 retail trade, where BNZ look for a 0.7% gain (consensus 0.5%) in volume

Northing in Australia, where Q4 Capex (Thursday), Construction work done (Wednesday) and January RBA Credit (Thursday) are the known highlights.

Offshore tonight, it’s just the Chicago Fed National Activity Index, US Wholesale Inventories and the Dallas Fed Manufacturing Survey. BoE’s Carney and Fed Vice-Chair Clarida are due to speak.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.