Online retail sales growth slowed in May following a fairly strong April

Insight

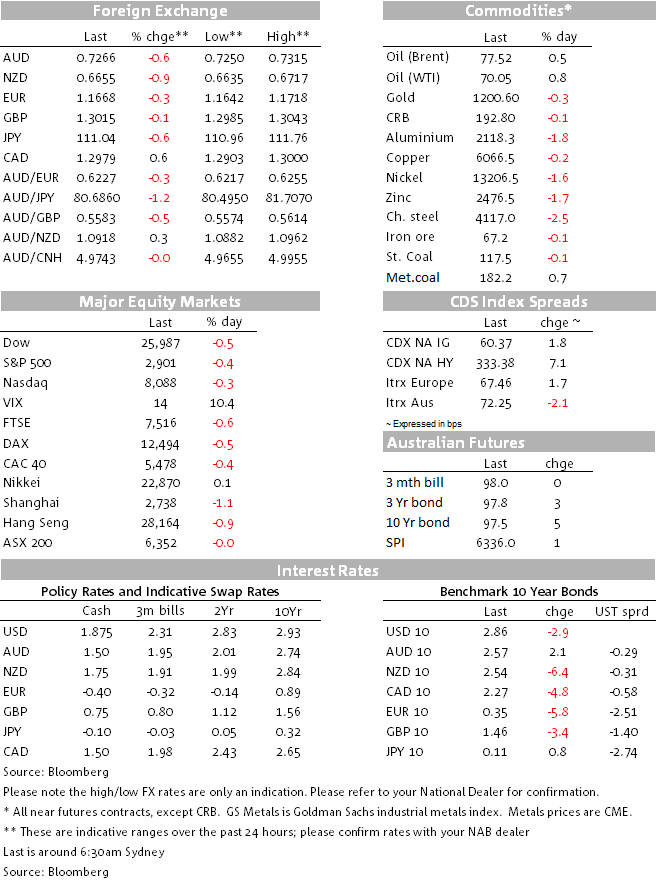

Equities and currencies in emerging markets took a tumble overnight, hurting the Aussie and Kiwi dollars in the process.

https://soundcloud.com/user-291029717/argentina-turkey-and-trade-uncertainty-hits-emerging-markets

News in the last couple of hours courtesy of Bloomberg that President Trump wants to move ahead with a plan to impose tariffs on $200 billion of Chinese imports as soon as the public comment period concludes next week, has pulled the rug from an earlier recovery in US stocks that in turn had been driven by a recovery in European bourses on news that the EU was (again) offering to cut tariffs on auto imports to zero if the US would do the same. Recall the EU currently imposes 10% tariffs on all cars coming into the EU from outside while the US imposes 2.5% tariffs on car imports and 25% tariffs on light trucks. Trump has just said that Europe’s offer for no auto tariffs is ‘not good enough’. Also helping US (technology) stocks was the news that Warren Buffet was lifting his stake in Apple, describing the iPhone as ‘enormously under-priced’.

Reading the full Bloomberg story on Trump’s China tariff intentions isn’t quite so alarmist, suggesting no decision has yet been made, that it could be implemented in stages, would not start immediately, etc. etc.. Trump has also tweeted that he expected to sort out trade differences by the time he meets with China’s President Xie in November. One thing’s for sure – Sino-US trade developments are destined to be the defining feature of September’s markets. We are inclined to take the headlines that Trump is minded to announce his intentions to ratchet up tariffs on China as early as next week at face value (the consultation period ends next Thursday).

The China tariffs headlines knocked more than 0.5% off the S&P 500 and another 20 pips off the AUD, that earlier wasn’t showing any sign of recovery from Wednesday and Thursday’s double hit from first the news Westpac was lifting its standard mortgage rate by 14bp – the market presumption being this would mean RBA policy ‘lower for longer’ – and then yesterday’s weak Q2 Capex (-2.5%) and Building Approvals data (-5.2%).

The AUD currently sits at 0.7266 and 2.1% down on the month heading into month-end, losses which have just been out-done by the NZD (-2.5%) which took another sizeable hit from yesterday’s ugly ANZ business survey. As a result of the latter, the NZ rates market now ascribes about a 50% probability to a 25-point cut to the OCR in the coming year. The Aussie rates market doesn’t have a 25-point rate hike priced before 2020, but is still not flirting with the idea of a rate cut before then.

Also not helping AUD has been renewed pressure on Emerging Market currencies outside Asia, with the Argentine Peso off another 12% overnight, this after the country had earlier asked for speeded-up disbursements of its $50bn IMF aid package and a failed attempt to shore up the currency with a15% jump in interest rates, to now 60%. Renewal of pressure on the Turkish Lire is also evident, off almost 3% overnight on rumours of the central bank deputy governor resigning and now back much close to 7 than 6 against the USD having been briefly sub-6.00 on Monday (so now 12% down on the week).

ZAR, CLP and MXN and BRL are also all lower by between 0.9% and 2.4%. This puts the JPM Emerging Market Currency index off another 1% (having been 1.5% lower immediately after the China tariff headlines). We will likely see some follow-through losses in Asia impacting on the ADXY to which the AUD remains highly correlated.

Slippage in both MXN and CAD has come despite continued optimistic soundings from the ‘new-NAFTA’ negotiations currently in place and where Trump has just said that a trade deal with Canada may come by Friday or ‘within a period of time’.

Elsewhere amongst the majors, the JPY has caught a fresh safe-haven bid to be 0.6% higher on the day, while the GBP is little changed, so still holding all of Wednesday’s gains on the comments from the ERU’s Barnier about a special Brexit deal for Britain. GBP has also been helped by a UK Times report indicating that French President Macron is urging EU leaders to make a deal with Britain as part of his vision for a united Europe – both inside and outside the EU. The Euro is lower against the USD (by 0.3%) but is continuing to out-perform commodity-backed currencies whenever trade tensions escalate.

US equities have closed with the S&P off 0.4%, the Dow -0.5% and NASDAQ -0.3%.

The China tariffs story has turned an earlier 0.5bp fall in 10-year Treasury yields into a 2.5bp drop, and a 1bp decline in the 2-year yield into one of also 2.5bps.

Oil is higher despite signs Europe is working hard to preserve an Iran nuclear deal that would allow it to by-pass US sanctions, but hard commodifies are all lower led by aluminium and nickel while Chinese steel futures are 2.5% lower.

US data had no real market impact, with the important core PCE deflator data for July coming in at 0.2% as expected, pushing the year on year rate up to 2% (i.e. bang on the Fed’s target) from 1.9% in July. Personal income was up 0.3% and spending 0.4%, close enough to expectations not to matter for markets while weekly US jobless claims remains very low at 213k (212k expected).

China official PMI numbers are out at 11:00 AEST and where both manufacturing and services readings are both expected to fall slightly, to 51.0 from 51.2 for manufacturing and from 54.0 to 53.7 for services.

Following yesterday’s ugly ANZ business survey, consumer confidence readings are due at 08:00 AEST. Australian July RBA credit numbers are at 11:30.

Also in our time zone Japan published unemployment, industrial production and most importantly, Tokyo August CPI data.

Tonight, EZ CPI is the European highlight and in the US, the Chicago PMI and final Michigan consumer sentiment.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.