We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

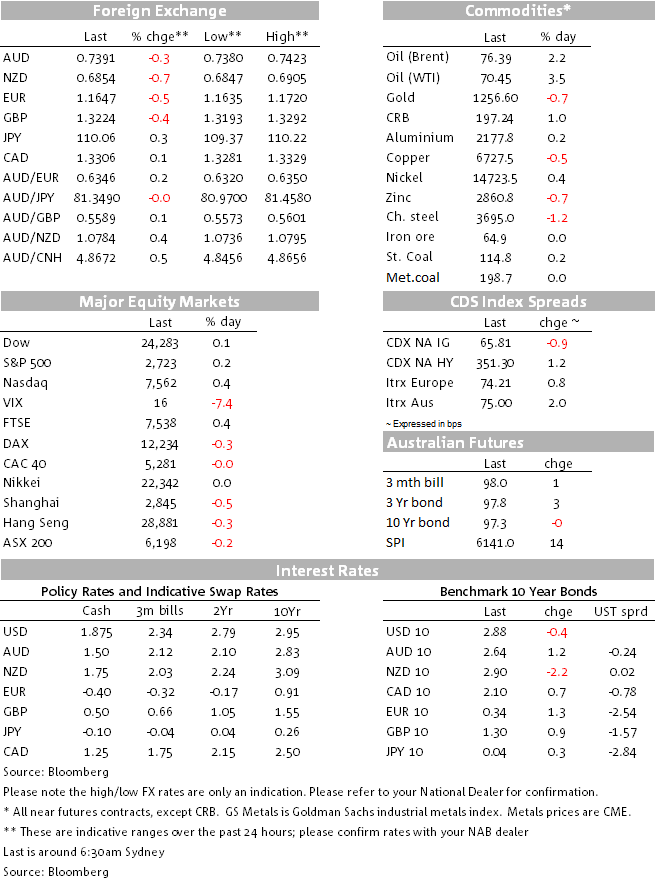

Oil prices pushed higher.

https://soundcloud.com/user-291029717/oil-up-as-us-threatens-allies-over-buying-from-iran

Tuesday’s offshore markets have witnessed a partial reversal of some of Monday’s key market movement, with the US dollar firmer and US stock showing modest gains, albeit pared into the close (S&P finishing +0.2% higher having been more like +0.5% an hour beforehand). The VIX is back below 16 having had a look up at the 20 level at its highest on Monday.

The energy sector has led the US stock market higher thanks to a decent move up in oil prices (Brent +$1.68 and WTI crude +$2.47). This is on intensifying supply concerns amid still robust global demand, the proximate cause of the latest run up being demand made by the U.S. that Japan stop importing oil from Iran and a related US threat to apply ‘zero tolerance’ to those who flout US demands. The deadline for the re-imposition of sanctions on Iran by the U.S. is not until November but is seems some countries who currently rely on Iranian imports and who are fearful of retaliatory actions from the U.S. should they continue to do so, are acting pre-emptively. Indeed, according to one oil industry report I’ve seen this morning, Iranian production in June has fallen to around 2.2 million barrels per day from 2.7 million barrels in May.

Alongside reduced Iranian output and hence exports, supply problems in Nigeria and Libya continue to be noted, alongside which a power failure is reportedly impacting on the export of Alberta oil sands in Canada. And as for last weekend’s OPEC/Russia agreement to increase supply by a notional one million barrels a day, this could in practise be as little as 270,000 barrels a day according to a report from the respected Bank Credit Analyst issued last night.

A slump in global trade would doubtless take care of any excess demand in global oil market, but here the overnight news is slightly positive. After Monday’s mini-market meltdown was seen to result from the various source reports that President Trump was going to imminently announce restrictions on Chinese investment in US technology related entities, the latest reports are that Trump is siding with his Treasury Secretary Steve Mnuchin over trade adviser and resident China hawk Pete Navarro, in wanting to use the Committee on Foreign Investment in the United States (CFIUS) to determine whether any (not just Chinese) investments in US firms should be allowed to proceed.

Also on the positive side of the trade tensions ledger has been an invitation extended by Trump for European Commissioner Jean Claude Juncker to visit the White House. This is as Trump insists he’s close to a being able to pronounce on a request made to the Commerce Department to determine whether car imports have the potential to threaten national security (and therefore provide the pretext for 20% tariffs – albeit down from 25% mentioned earlier). Let’s see if the US can be persuaded to pull back from the brink here, since we shouldn’t underestimate the impact bringing the brewing trade tariff war to the auto sector would have on a large sector of the industrial economy, such is the labyrinthine nature of global auto supply chains.

One other thing to note on trade tariffs is that Canada is reportedly preparing steel quotas and tariffs on China and other countries, designed to prevent a potential flood of steel imports from global producers looking to avoid US tariffs.

The across the board US dollar strength overnight (DXY +0.4%) is a reminder that when trade tension rise, USD tends to suffer alongside the AUD. The Aussie has though failed to hold above 0.7400 overnight, partly because the USD is up, but also because of the concerns raised this week that China is now allowing its currency to weaken beyond levels consistent with volatility in the USD. Daily USD/CNY fixings have now taken on added significance.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.