Price growth edges lower despite reasonable economy

Insight

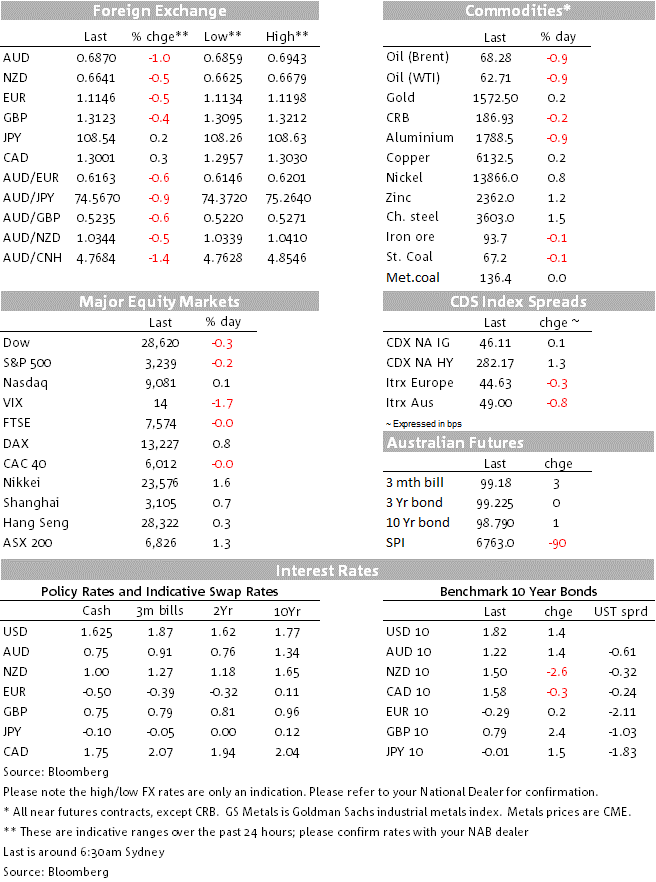

It’s been a particularly bad 24 hours for the AUD (if you aren’t an Australian exporter, that is).

AUD/USD is down by a little over 1% on Monday’s New York closing level to a low of 0.6859 and which has taken it back below its 200-day moving average. The AUD/JPY cross has not fared much better, off 0.9% to a low of 74.57, in doing so breaking below significant upward trendline support. And the low on the AUD/NZD cross of 1.0340 is its lowest since since early August 2018. If it closes in New York near here, it will be its lowest daily close since late March 2019.

Underlying causes of the AUD’s weakness look to be more idiosyncratic than global, even though the USD had drawn support from good non-manufacturing ISM data (more below). Certainly the latest losses can’t be blamed on risk sentiment, which remains improved on the levels seen either side of the weekend, albeit US stocks are coming into the last hour of trading showing small-scale losses for the S&P and the Dow, if not the NASDAQ which is about flat. Also to note is that AUD weakness has flown in the face of a stronger CNY, which yesterday rose by over 0.4% to its strongest levels against the USD since the start of August 2019 (which, recall, was just in front of the US announcing 10% tariffs on all remaining China imports not at the time subject to tariffs).

Yesterday’s domestic economic data, albeit second tier, clearly had a hand in AUD weakness. ANZ’s Job Ads series for December was the second largest monthly fall since 2009 (-6.7% m/m), attributed to spill-overs from the bushfires as has happened at times of previous natural disasters (to then bounce back). Weekly consumer sentiment was on the soft side too, -1.7% to 106.2 in the week to Jan 5, from its most recent previous reading before Christmas in mid-December. Consumers are more worried about the economy despite more favourable perceptions about personal finances. This is a sentiment indicator of course, not spending, but important to watch nevertheless. So concerns about economic slowing, inevitably compounded by the bushfires and in turn seeing expectations rise for a resumption of RBA easing when it returns on February 4, are doing damage alongside the aforementioned breach of important technical levels. And while the latest CFTC/IMM data published on Monday night shows a still-large speculative short position in AUD, we’ve also judge that, flow-wise, part of the sell-off in all things AUD so far this week reflects selling by traders who got long during December (a month, remember, when AUD/USD rose by more than 4%). Market implied odds for a 25bp RBA cut on Feb 4 are now close to 60%, up from around 38% on Christmas eve.

The key overnight development has been economic not geopolitical, namely the US non-manufacturing ISM report. The 55.0 headline was up on 53.9 in November and just above the 54.5 consensus, driven primarily by a surge in the business activity sub-series, to 57.2 from 51.6 and suggesting that the news of a Phase 1 US-China trade deal, however minimal in substance, has gone somehow toward restoring sentiment and activity in the sector that represents some 88% of the US economy. Moreover, the 55.2 Employment sub-series, albeit down on 55.5 in November, is on some estimates consistent with non-farm payrolls growth in the order of 180,000 (ADP employment due tonight ahead of payrolls on Friday).

Also to note on the US data front was a significant shrinkage in the US trade deficit in November, to $43.1bn. versus $46.9bn, largely reflecting 1% fall in imports (-1.3% in real terms, and which is supportive of Q4 GDP). This was to a large expect expected after US firms had earlier rushed to import in front of the imposition of either new or additional tariffs on Chinese imports. The net result of this week’s US data flow has been to see the Atlanta Fed keeping its Q4 ‘GDPNow’ estimate unrevised at 2.3% (the first official estimate of which is due on January 31).

We have US treasury bond yields up 1.6bps for 10-year treasuries but unchanged at the shorter end; US equities currently -0.3% for the Dow, -0.2% for the S&P and +0.1% for the NASDAQ and hour before the close, and the DXY USD index up a third of a percent to just back above 97.0. In commodities, oil has extended the modest loss seen during our time zone, to be down just under 1% (Brent to $68.28). Gold is making further progress towards the $1,600 level in many pundits sights, currently +$5 to $1,571. Base metals are mixed, aluminium -0.9% but most others up (LMEX index is little changed) while iron ore is down 0.1%.

Australia Building Approvals due at 11:30 ET are likely to have fallen further. Residential approvals are forecast to fall 2% in November (consensus +2% but with a very wide dispersion of market estimates, from -5% to +5%). Apartment approvals don’t appear to have stabilised and NAB expects a further fall in unit approvals to offset a moderate bounce in house approvals. We also get official November job vacancies (which were -1.8% in October).

Offshore this evening, German November factory goods orders are of interest for any evidence of stabilising in manufacturing conditions, that certainly are not in evidence judging from recent months’ PMI numbers – including for December – mired dep in sub-50 contractionary territory. The various Euro area confidence readings, for December, will also be worth a look

In the US, the ADP employment report is the highlight and may have some bearing on estimates for Friday’s non-farm payrolls

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.