Coming in for landing in a heavy cross wind

Insight

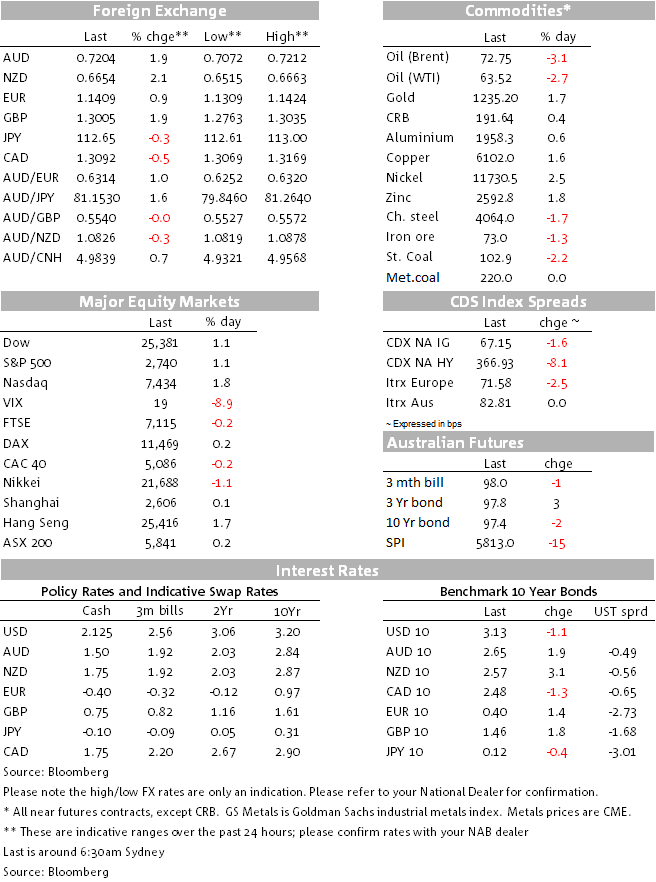

The US dollar staged a swift reversal overnight, with the spot index falling significantly. We’ve also seen US stocks on the rise, along with significant leaps forward for the Aussie dollar and the pound, whilst oil falls sharply.

https://soundcloud.com/user-291029717/big-moves-based-on-small-bits-of-hope

Sometimes is hard to come up with a song title, but on rare occasions we have to use two!

After making new highs early morning yesterday, the USD has been on a steady decline over the past 24 hours with a mix of factors at play. Brexit news have boosted the pound with a hawkish BoE also playing a supporting role and yesterday’s improvement in risk appetite was enhanced further overnight by a tweet from President Trump highlighting a “very good conversation with President Xi”. Moves in currencies have also been amplified by extreme positioning with gains in the NZD and AUD likely reflecting a squaring of short positions. Meanwhile on the data front a soft ISM didn’t help the USD with UST yields also nudging a bit lower, oil prices also had a rough night weighted down by new data showing OPEC increase in supply….and finally Apple’s disappointing results could set the tone for equities today

The steady rise in the USD over the past fortnight or so has come to an abrupt end over the past 24 hours. It all started yesterday with the improvement in risk appetite helping risk sensitive currencies regain some ground against the USD. Brexit news then hit the screen with The Times reporting the UK and EU had come to a preliminary agreement to allow UK banks and financial services firms to access the EU market after Brexit. The headlines triggered a jump in the pound from 1.2770 to 1.2850 with the euro also benefiting from the news (now @1.1410). The article noted that under the services deal the EU would guarantee UK companies access to European markets as long as British financial regulation remained broadly aligned with that of Europe. Subsequently, UK officials downplayed the report saying the claims were “unsubstantiated” and later on EU chief negotiator Michel Barnier described the report as “misleading”.

The pound ignored the politician rebuttal and later in the European session a more hawkish Bank of England (BoE) gave GBP another leg up. The new BoE forecast, which assume a “smooth Brexit”, show inflation above the 2% target for most of the forecast period, implying the Bank foresees a somewhat faster pace of rate rises than priced-in by the market. Governor Carney noted that the economy was at full capacity and wage growth had been higher than expected. Then early this morning the FT reports that EU officials have floated a compromise aimed at overcoming the dispute between London and Brussels over a “backstop” provisions to avoid a hard border between Ireland and Northern Ireland. So after starting the day at 1.2770, GBP now trades at 1.3014, up almost 2%. The news are obviously positive and although we have been down this road before, the sound-bites are encouraging. Worth noting here though that one thing is for the UK government to reach an agreement with the EU, then whatever is agreed still needs to be approved by both the UK parliament and also EU members. So there is still a long and likely volatile road ahead.

The NZD is the other top performer overnight, up +2.18% and now comfortably trading with a 66 handle. This time yesterday the kiwi was trading at 0.6516 and intraday chart shows the pair has been on a steady rise since then, the pair nowtrades at 0.6659, a level not seen since late September. The AUD which yesterday was supported by a much stronger than expected trade surplus, has also traded higher (+1.94%) and now trades at 0.7209, up 39 pips over the past 24hrs and is back above the figure for the first time since early October. Overnight the USD has been broadly under pressure, not helped by a softer ISM print (more below), but AUD and NZD outperformance has also been boosted by the break of key technical levels which have more than likely been accompanied by squaring of short positions by speculative investors. Both antipodean currencies have been stuck in a downtrend with short positions close to extreme levels, the overnight breaks above 0.6578 for the kiwi and 0.7168 ( 50DMA) for the aussie have essentially broken these downtrends and if sustained it will discourage speculators to continue to bet on lower levels. If risk sentiment remains buoyant, the clearing of short positions suggest both antipodean currencies have near term upside. Trump’s tweets and non-farm payrolls tonight are the ones to watch.

As noted above, USD softness has not just come about by gains in other currencies. The big dollar also came under pressure overnight by a softer then expected ISM manufacturing print. the ISM manufacturing survey fell by more than expected in October (57.7 vs. 59 exp.), led by declines in the new orders and production indices. The survey remains at very healthy levels overall, and consistent with still strong levels of US manufacturing activity, but there are signs that the pace of activity is slowing. BBDXY now trades 0.80% lower at 1200 and DXY is at 96.68, down 0.90 over the past 24hrs.

Equity markets have started November strongly (S&P500 +1.06%, NASDAQ +1.75%), continuing on from the large increases yesterday. Equities and broader risk sentiment were boosted by an encouraging tweet from President Trump on China trade negotiations. Trump tweeted “Just had a long and very good conversation with President Xi Jinping of China. We talked about many subjects, with a heavy emphasis on Trade. Those discussions are moving along nicely with meetings being scheduled at the G-20 in Argentina.” White House economic advisor Larry Kudlow later told CNBC that “nothing is set in stone right now”, on whether Trump would impose further tariffs on China. Despite the more positive comments overnight, expectations are low that China will make the concessions that Trump has been demanding, making it likely that the US ultimately imposes further tariffs on China. Equities were also supported by better than expected corporate earnings results (although these didn’t appear to provide much support to the equity market in October). Apple releases its results after the bell today.

All that said Apple has just released its results reporting lower than expected revenues. Apple Sees 1Q Rev. $89B to $93B, Est. $92.74B, shares are now down 4% afterhours.

UST yields have been relatively stable over the past 24hrs. The softer than expected PMI print weighted on yields with the move lower led by the front end of the curve. The 2y tenor is down 1.5bps to 2.85% and the 10y rate is 1bps lower at 3.13%.

Following the improvement ins risk sentiment copper is the outperformer overnight up 2.5%. Meanwhile oil prices are sharply lower (WTI -2.5 and Brent -3.45%). Oil prices fell following news that OPEC’s crude production climbed to the highest level since 2016 as increases by Saudi Arabia and Libya offset losses stemming from impending U.S. sanctions on Iran.

The ISM manufacturing index fell to 57.7 from 59.8 in September, below the consensus, 59.0. The 2.1 decline in the ISM was driven by New Orders (-4.4 to 57.4) and Production (-4.0 to 59.9)

US third quarter productivity rose at a 2.2% annualized rate, a tenth better than consensus. Unit labour costs rose 1.2%, marginally above consensus, 1.0%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.