Online retail sales growth slowed in May following a fairly strong April

Insight

A risk-off mood saw moves to US Treasuries with big falls in yields and shares.

https://soundcloud.com/user-291029717/bonds-run-hot-sacrificial-may

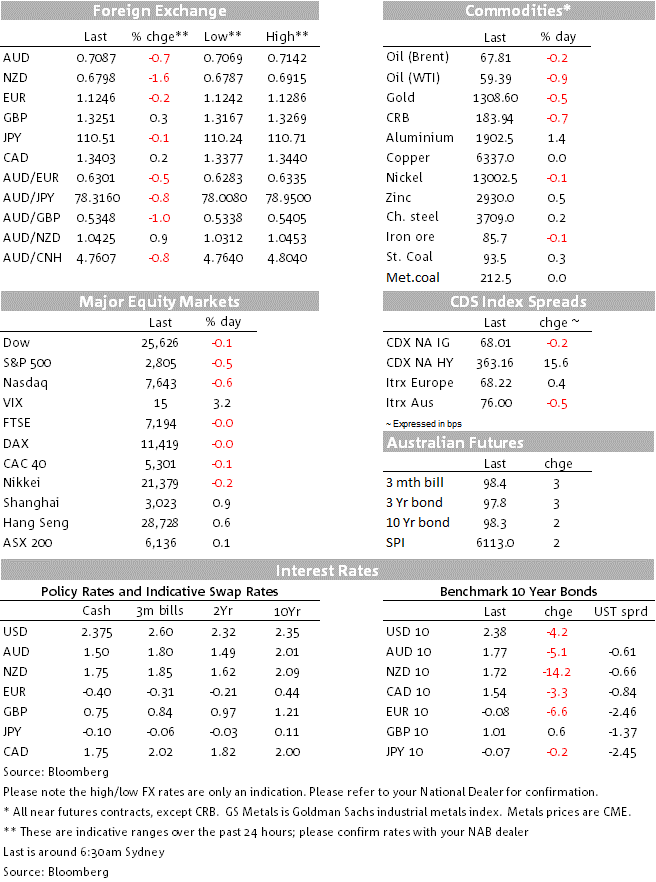

It has been a cagey night for markets with declines in core global bond yields heightening concerns over a more protracted global growth slowdown. European equities closed mixed and main US equity indices ended the day in negative territory . Speaking early in the session, ECB Draghi depicted a glass half full picture noting that “a soft patch does not necessarily foreshadow a serious slump”. Markets were not convinced with 10y Bunds leading the decline within core bond yields. Meanwhile the FX market has been a bystander – the NZD has retained it post RBNZ losses and the AUD underperformed reflecting the market’s wary mood. The UK Parliament indicative voting has begun and PM May has promised to resigned if her WA is approved by Parliament. GBP is a tad stronger, but the final outcome from the voting process is not expected until early next week

In a night devoid of any significant economic data releases, market attention has been centred on Central Bank speakers with the ECB and Its Watchers conference taking centre stage. President Draghi delivered a glass half full assessment of the EU economic outlook stressing that “a ‘soft patch’ does not necessarily foreshadow a serious slump” adding that the ECB’s inflation goal has been “delayed rather than derailed,”. The President then went on to stress that accommodative policy is still needed (implying a further delay on the prospects of lifting policy rates) while at the same time he also conveyed confidence that growth in the economic bloc will eventually regain speed. Notably as well the President acknowledge the Bank was ready to soften the adverse effect from negative rates if they are found to harm the transmission of its monetary policy. The “if “ in the last statement is an important caveat, reflecting the ECB’s uncertainty on whether there are significant adverse effects from its negative rate policy, in a similar vein Vice President Guidos noted that while compressed interest margins pose a challenge to banks, the gains “have so far greatly offset the losses.”. So similar to the BoJ, it remains to be seen if the ECB will make any changes to its negative rate policy and none of the ECB speakers overnight offer any suggestions on what measures could be introduced to offset the adverse effects from the current negative interest rates policy setting.

In the end, Draghi and other ECB commentators overnight did little to change the sombre market mood. Core bond yields were already declining ahead the ECB speeches and if anything the downtrend accelerated once the speeches had ended. 10y Bunds led the decline, trading down to an overnight low of 0.093% before closing the day at -0.081%, 6.5bps lower on the day. The move lower in UST yields were again been led by the front end of the curve with the 2y tenor down 6.2bps to 2.20% while the 10y rate declined by 5bps and now trades at 2.377%.

European financial shares were boosted by Draghi’s negative rate comments helping the Stoxx 600 index close just above positive territory while healthcare and IT sectors recorded declines over 1%. Meanwhile, the losses in US share have been more uniform with all 3 major indices ending the day down between -0.2% and -0.65%.

Moves in currency markets have been more subdued. The USD has remained in its upward trend established after the dovish FOMC meeting on March 21, despite a broad decline in global yields, in a world concern over the prospect for the global growth outlook 10y UST yields at 2.37% look a lot more attractive than 10y Bunds and or 10y JGBs at -0.08%. The EUR now trades at 1.1247 and USD/JPY is at ¥110.51, both are little changed over the past 24 hours.

NZD has retained its post RBNZ losses and now trades at 0.6798, 1.50% lower relative to levels seen this time yesterday. Yesterday’s OCR review from the RBNZ was widely anticipated to pass with little fanfare with an unchanged policy outlook, but the Bank shocked the market by explicitly introducing a bias to ease policy, commenting “given the weaker global economic outlook and reduced momentum in domestic spending, the more likely direction of our next OCR move is down”. Our BNZ colleagues note that the RBNZ also surprised the market at its August (to the dovish side) and February (to the hawkish side) Monetary Policy Statements. In both cases there was an additional ½ cent follow-through in the following days, before the market reaction was reversed by subsequent factors. If the same pattern follows, then the NZD might well be supported around 0.6750 before global trends take over. This afternoon ANZ’s business outlook survey takes on increasing importance, in light of the RBNZ’s fresh policy bias, with a weak result fuelling rate cut expectations and only a strong rebound likely to have any opposing market impact.

Yesterday the AUD gapped a little bit lower in sympathy with the NZD move, but unlikely the kiwi that traded sideways during the overnight session, the aussie continued to drift lower overnight not helped by the souring in sentiment evident in bonds and equity markets. The pair now trades at 0.7086, after trading down to an overnight low of 0.7066. Today we get the ABS measure of job vacancies and although it is not usually a market moving data release, our economists note that the RBA has noted the strength in Job vacancies at the end of last year, while job ads, the NAB survey measure of employment conditions and unemployment expectations have weakened. Faced with this divergence, the RBA has placed greater faith in the ABS’s broader measure of labour demand, which, in theory, captures all available job openings, not just those advertised externally. Our view is that this divergence will be resolved by vacancies falling sharply in Q1 given the monthly indicators provide a more timely read on the labour market. If we are right, this should concern the RBA as it would point to slower growth in employment.

The UK Parliament has begun the indicative voting process eight Brexit options, the results of which are non-binding.The eight options are no-deal, Norway Plus, Norway, Customs Union, no-deal emergency brake, second referendum, and Malthouse Plan B which is like a managed no-deal Brexit. PM May hopes to have a third vote on her plan at the end of the week, but there still remains an element of doubt whether the speaker will allow it. PM May told her party this morning that she will stand down once she has ratified a deal and Britain has left the EU, which might help trigger more support for her deal, although crucial support from coalition partner DUP remains in doubt. GBP has been well supported overnight and currently trades at 1.3251

Finally in other news, speaking to the WSJ Fed’s Kaplan noted that before considering whether to lower rates, “I’d need to see an inversion of some magnitude and/or some duration…If you see an inversion that goes on for several months…that’s a different kettle of fish,” he said. “We’re not there yet.” Importantly he states: “I’m being very careful not to speculate on what we do next,” he said. “I don’t think we’re going to have a good fix on that until we get a better grip on the second quarter, because the first quarter is very noisy.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.