Total spending grew 0.9% in June.

US equities bounced higher overnight, helped by Facebook’s earnings report.

https://soundcloud.com/user-291029717/bouncing-into-the-month-as-shares-turn-about-face

On the last day of what’s been a very ordinary month for equity investors, the market has rallied in size, kicked off in Asia yesterday on hopes of a Trump-Xi trade “great deal”, and given a further push from a market looking for good news from Facebook that released after the US markets closed yesterday. Remember too that with the capitulation in stocks this month, funds likely had to rebalance their portfolios at the end of the month to lift their exposure to equities, that exposure restrained by lower prices.

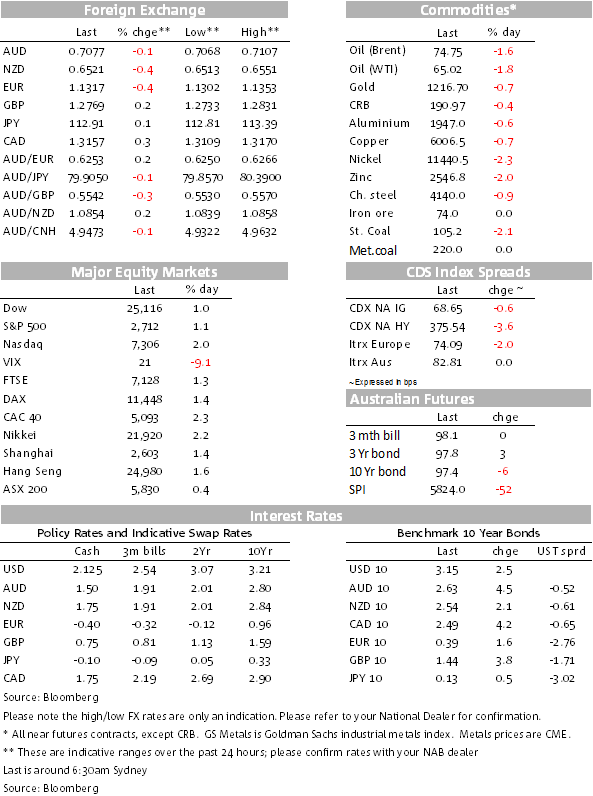

The FAANG stocks are up in size this morning, the FAANG index by 3.59%, limiting the loss for October to 7.21% and for the Nasdaq to a decline of 9.20%, up 2.01% by the close. The S&P 500 is up 1.09% and down 6.94% for the month. European equities had an equally positive finish to the month.

The USD has only made small incremental net gains on a DXY/BBDXY basis. Notwithstanding the risk-on rally in size, the AUD remains below 0.71, trading at 0.7077 this morning and not able to recapture 0.71 again, though it did briefly spike to 0.71, only to relent. Yesterday’s headline CPI had a soft edge to it, headline CPI missing by a tenth, and annual underlying CPI still at 1.8%, June quarter annual growth also revised down by a tenth. That was immediately followed by softer than expected China PMIs, the AUD pulling back as a result from earlier near-0.71 levels.

Despite the de facto risk on mood of markets, the AUD has failed to regain a 71 handle, likely held back by some continued volatility in the USD/CNY(CNH) testing higher, the market testing the nerves of the Chinese monetary authorities that have drawn a line in the sand at 7. USD/CNH is trading at just below 6.98 this morning. There are signs the Chinese authorities are taking steps to tighten liquidity in the offshore CNH market (making it more expensive to short the CNH) by increasing bill sales.

The big currency mover overnight has been Sterling, Cable up 0.51% on a short-covering rally from hopes of a Brexit deal as the 11th hour approaches. (Haven’t we heard that refrain before?) This time it was a letter from UK Brexit Secretary to the UK cross-bench Parliamentary Committee on exit from the EU that a deal will likely be done by November 21, Raab saying he’d be happy to then appear before the Committee. There was a departmental clarification that there is “no set date for negotiations to conclude”, but this news was enough to flush out some Sterling shorts. Whether a deal can be done – perhaps the backstop of a temporary customs union for the UK to essentially kick the can down the road further – thus avoiding a physical border in Ireland and satisfy all sides, only time will tell. If there is one done, then there could be quite some rally: my FX Strategy colleague Gavin Friend from London that Cable could rally by 10% in a relatively short time, also seeing a sizeable lift in EUR/GBP. “If”, that is, “if” a little word with a big meaning.

Data released overnight was largely taken in its stride and not having a large market impact. There was a reminder of potential investor wage inflation nerves being frayed ahead of Friday’s payrolls with a bounce-back in the US Employment Cost Index for Q3 that rose a stronger than expected 0.8%/2.8%, the market expecting 0.6%. The upside surprise came from wages and salaries that rose 0.9% after 0.5%, reversing what was an unexpectedly low print in Q2. Nothing too much to alarm investors that wage inflation is racing away, but this measure is increasing toward 3%, the ECI at 2.8% in Q3 in annual terms, wages and salaries up 2.9%. It’s onward now to average hourly earnings tomorrow night.

The EC CPI release for Oct was in line with expectations, headline CPI at 2.2% and the core CPI back up to 1.1% from 0.9%. The EUR was largely unmoved overall, drifting off somewhat this morning, after initially lifting somewhat.

With equities back in the ascendancy, for the day anyway, it’s not surprising that bond yields have pushed back up, but to a rather modest extent, and also not frightened by another increase in the US Treasury’s quarterly refunding announcement, the largest since 2009!, nor to the extent of end-month rebalancing selling of bonds back into equities. The 10 year US Treasury is up 2.65bps to 3.1492%, Aussie 10 year bond futures little changed.

The story for the hard commodities in Asia yesterday and overnight has been mixed to softer. LME base metals lost some ground, copper down 0.66%, oil is softer, as is gold. The bulks were mixed yesterday, Dalian iron ore little changed as was steel rebar futures.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.