We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Geopolitical tensions remain centre stage with markets clearly in wait-and-see mode.

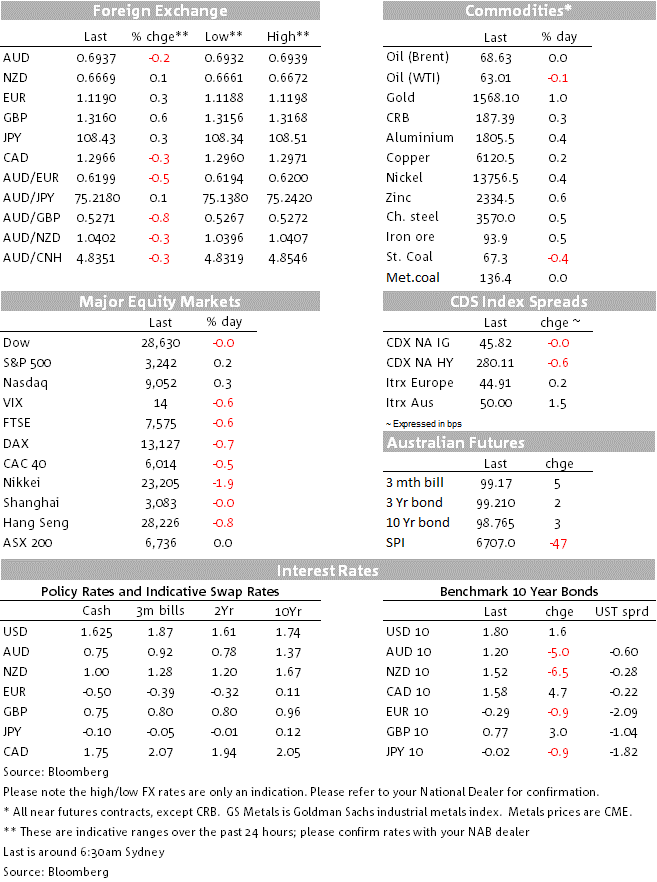

The risk-off mood though did ebb slightly overnight with no new developments, while strong Services PMIs from the UK, EZ and the US serve as a reminder that the global economy appears to be stabilising as we start 2020. Reflecting some ebbing of the risk-off mood, USD/Yen rose (+0.3% to 108.44), while gold pared some of its gains to end +1.0% to 1,568.70. Equities are broadly steady with the S&P500 +0.2%, while yields are slightly higher with US 10yr +1.6bps to 1.80%. In FX, GBP lead gains (+0.6% to 1.3157) after a stronger than expected final-Services PMI. The USD fell with the DXY -0.3% to 96.69. The AUD underperformed, down 0.2% even with USD weakness.

Rhetoric unsurprisingly remains on the strong side, though with no new developments overnight. The latest threats include President Trump’s warning that he could target Iranian cultural sites, while Iranian leaders continue to threaten retaliation for Friday’s assassination of General Soleimani. One Iranian general noted “the minimum retribution for us is to remove America from the region”. We may not get further development on this until after today with mourning ceremonies only set to conclude with the burial of Soleimani’s remains on Tuesday. The potential for this to spiral into a cycle of retaliation remains and markets will likely remain cautious. In related news, AFP is reporting that the US army is preparing to “move out” of Iraq.

Services PMIs were revised higher on the final read for December in the UK, EZ and the US. The UK Services PMI was revised to 50.0 from 49.1, EZ to 52.8 from 52.4 (with Germany importantly 52.9 from 52.0). The stronger than expected reads saw gains in both EUR and GBP, with GBP leading G10 FX gains to be up 0.6% to 1.3157. Anecdotes from the report emphasised stabilisation in the services sector for Europe, helped along by an increase in new business. Separately, Retail Sales for Germany were very strong in November, up 2.8% y/y against 1.0% expected.

The US Services PMI was also revised higher to 52.8 from 52.2, though was not as market moving and all eyes will be on the Non-manufacturing ISM later tonight. Aggregating the individual country PMIs, the JPMorgan Global Services PMI rose to 52.1 from 51.6 in November, with output, new orders and employment at five-month highs (see link for details).

All talk is on the bushfire crisis. Yesterday PM Morrison committed an initial $2bn over 2 years to rebuild communities via a newly established National Bushfire Recovery Agency. Importantly, the government appears to be more willing to open the fiscal taps with PM Morrison stating “the surplus is of no focus to me. What matters to me is the human cost and meeting whatever cost we need to meet”.

The AUD underperformed, down 0.2% to 0.6937 with no single catalyst. Market pricing for a February rate cut has been creeping up, partly driven by geopolitical tensions as well as the potential for the bushfire crisis to have affected activity and is now around 55% priced by the market.

Domestic focus will be on the normally second-tier ANZ/RoyMorgan Weekly Consumer Confidence Index to glean the extent to which the bushfire crisis may be weighing on consumers. Also out is ANZ Job Ads for December. Internationally, the focus will be on the EZ CPI and then to the US Non-manufacturing ISM.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.