Long-term signal vs. Short-term noise

Insight

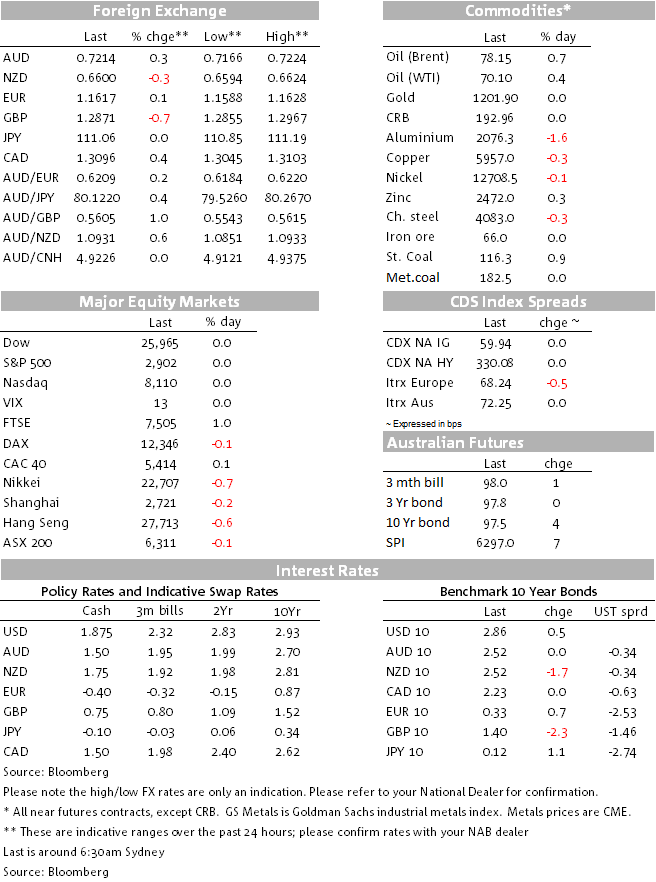

Quieter markets didn’t help the pound which fell on further UK-EU disagreement on Brexit and more speculation on a leadership challenge.

https://soundcloud.com/user-291029717/brexit-bluster-aussie-data-and-nz-rate-cuts-possible

“Find the torch, burn the plans, State your case in the land” – Paul Weller

It has been a quiet start to September partly due to the US being on holiday celebrating Labor Day. European equity indices ended the day little changed with the UK FTSE 100 the stand out, up almost 1% and buoyed by a 0.7% decline in the pound. Criticism of PM May Brexit plan, rumours of leadership spill and soft manufacturing data all conspired against GBP. AUD climbs above 72 cents, but with EM usual suspects under pressure it is hard to get too excited on the mini AUD rebound. Meanwhile in bond land, softer Italian budget rhetoric has helped Italian sovereign bonds outperform overnight.

Last week GBP climbed above 1.30 on the back of seemingly positive Brexit sound bites with the move boosted by a short squeeze as the currency pair climbed above its then August month to date high of 1.2936. Over the weekend PM May said she would not compromise on the UK government’s Chequers plan and also ruled out a second Brexit referendum. In response EU’s chief Brexit negotiator Michel Barnier said that he “strongly opposed” the “illegal” Chequers plan, because it sought to unpick the single market. PM May’s obdurate position appears to have back fired amid strong criticism within her party and rumours of a leadership challenge. Former UK Brexit negotiator Davis said that he will vote against May’s plan and others suggested that she obviously didn’t have any Parliamentary backing for the plan. Former foreign secretary Johnson claimed May’s plan would be a “disaster” for Britain and this has restarted speculation of a possible leadership challenge to May as Parliament opens for business after the summer break. Also not helping GBP, on the economic front, the UK manufacturing PMI came in softer than expected, slowing to its weakest level in two years. GBP is down 0.7% to 1.2873 and in the process the move has helped the AUDGBP cross climb back up to 0.56 mark.

On the other side of the ledger, the Swedish krona is the top G10 performer, up 0.8%, with traders putting it down to a short squeeze ahead of a Riksbank meeting this week and a general election, where focus has turned to the rise in support for an anti-immigration nationalist party that could form part of the next government.

After a soft end to the month of August, AUD has started the month of September in a slightly positive mood (+0.35%), climbing back above the 72c mark with GDP partials yesterday supporting our view for a reasonable Q2 GDP print on Wednesday. That said, it is hard to get too excited on the AUD near term fortunes given the imminent risk that President Trump may impose another round of tariffs on Chinese imports. In the domestic front more out-of-cycle mortgage rate rises adds a domestic element to downside AUD risk via further pushing out expectations for the start of an RBA tightening cycle and although it has been a relative quiet night for markets, EM FX usual suspects have remained under pressure.

The Argentine peso fell another 4.2% in spite of a new round of austerity measures announced by President Macri. BRL is down 2.27% with news that a Brazilian electoral court has banned former President Lula from competing in next month’s elections doing little to arrest the political uncertainty in Brazil. Yesterday’s Turkey’s August inflation printed at 17.6% and while the country’s central bank has promised to make the necessary policy adjustment next week, the market remains sceptical given President’s Erdogan wishes for lower rates. Meanwhile ZAR was also down more than 1% on no new news.

So for now most of EM woes can be attributed to country specific issues, but with USD liquidity shrinking as the Fed is expected to continue with it gradual tightening strategy and with President Trump seemingly keen on pursuing its hard line on trade policy, EM contagion risk is still alive and kicking. Thus with AUD being the G10 risk barometer, we still think the currency’s balance of risks are tilted to the downside.

Quiet start to September with the US celebrating Columbus day. US equity futures edge up a few points on Monday and European equities were little changed, barring the UK FTSE which was up 0.97%.

European bonds closed little changed with UK Gilts a couple of bps lower amid rising domestic political uncertainty ( 10y Gilts -2.3bps to 1.402%). Italian BTPs were the stand out performers lifted by softer rhetoric on the Italian budget by Deputy PM Salvini. Deputy PM Salvini said Italy’s budget will lower taxes and respect rules.

It has been another mixed night for commodities with LMEX (-0.40%), copper (-0.60%) and aluminium (-1.32%) all having a negative start to the new month. Meanwhile oil prices ( Brent +0.94%, WTI +0.43%) and lead (2.02%) are the outperformers.

Assessment of Iranian sanctions and the prospect of tropical storm Gordon becoming a hurricane as it crosses the Gulf of Mexico have helped oil prices perform.

EZ: Manufacturing PMI unchanged from the flash at 54.6. Nothing much to read into here, trade uncertainty remains a headwind

UK Manufacturing PMI disappoints at 52.8 against expectations of 53.9. Details show New Export orders are slowing and have contracted for the first time since April 2016. That flowed to slower rates of production and employment – job creation at large enterprises was quoted as being “near-stagnation”. Brexit uncertainty remains a headwind.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.