NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

President Trump is threatening more tariffs – this time on car imports.

https://soundcloud.com/user-291029717/brexit-fears-more-trump-tariffs-and-powell-close-to-neutral

Just try to see in the dark, Just try to make it work – The Cure “Close to me”

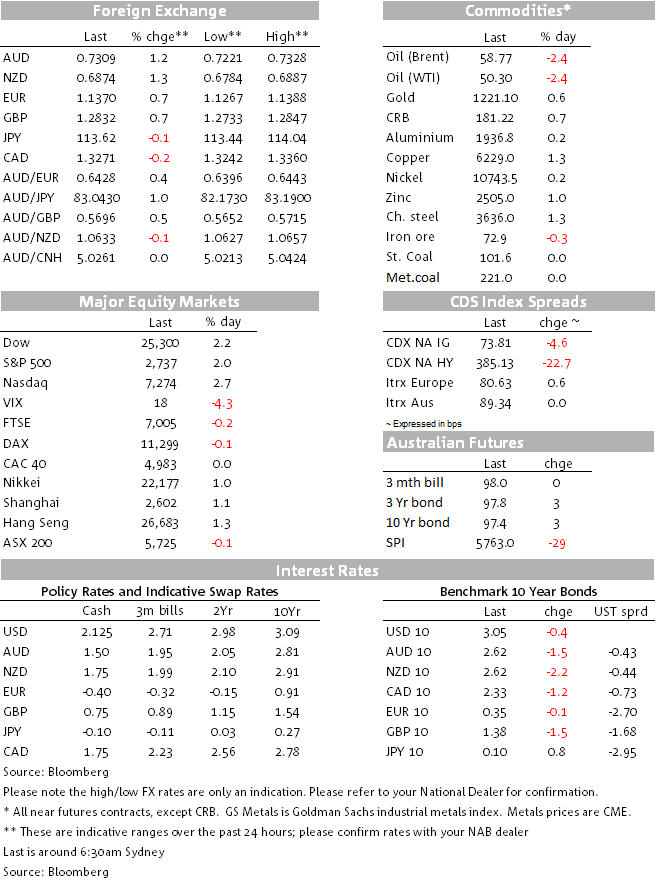

…and so the dot plot thickens. A dovish interpretation to Fed Chair Powell’s remarks early this morning has boosted US equities and dragged the USD lower alongside a steepening of the UST yield curve led by a rally in front end yields. NZD and AUD have benefitted the most within G10 with both antipodean currencies up more than 1%. A long-awaited BoE/Treasury Brexit scenario report reveals the UK to be economically worst off under any form of Brexit, meanwhile Trump has continued to up the ante on the prospect of car tariffs.

Early this morning Fed Chair Powell spoke at the Economic Club of New York and although his speech was primarily about financial stability with an emphasis on a gradual approach to policy tightening (highlighting rising indebtedness and deteriorating loan quality as top vulnerabilities facing the U.S. financial system), the market reaction to the speech came from his observation that interest rates “remain just below the broad range of estimates of the level that would be neutral for the economy.”. This was a material change from his view in October when he noted that that “we may go past neutral, but we’re a long way from neutral at this point, probably.”

As noted above Powell’s remarks elicited a risk positive market reaction as they appear to suggest a softening in his stance in terms of what might be the future pace of policy tightening. The consensus view is that the Fed would look to pause as and when it reaches a neutral level in the cash rate where policy is considered to be neither stimulatory nor restrictive. That is all well and good, but the problem is that there is no consensus even within the Fed as to where exactly neutral is and just to put an additional spin on that, neutral is not a static place. For instance if productivity does increase, as many expect , then this means that all else equal the US neutral rate could be higher next year relative to where it is today.

For now the market is going with a dovish interpretation to Powell’s remarks given that by his own interpretation of neutral now we are closer than where we were in October. That said we would add a bit of cautiousness to the market’s reaction, for one based on Fed officials remarks neutral is somewhere between 2.50% and 3.5% and so with the Fed Funds target range of 2.00% – 2.25%, we are one hike away from the bottom of the range, three hikes from the mid-point and five hikes from the top. Assuming the Fed hikes in December, the market is currently pricing essentially one hikes in 2019 and currently the median dot for 2019 is suggesting the Fed is looking to hike 3 times next year. Based on recent Fed rhetoric and distribution of dots, we think there is a material chance that the median dot in 2019 goes down to two hikes, so on this basis current market pricing looks aggressive. Ahead of the Fed December meeting on the 18-19th we have important data releases to consider (ISM -3 Dec, Payrolls -7 Dec and CPI 12 Dec), some slowdown in activity from above potential levels has always been part of the Fed’s consideration and if the labour market shows further tightening one hike in 2019, as per market pricing, may not be enough.

Powell’s remarks have essentially defined the price action overnight, not much to see prior to his speech and a broad weakening of the USD post. The DXY and BBDX indices are down about 0.60% with DXY now trading at 96.80 and BBDXY at 1204, so both indices still remain close to the top end of recent ranges.

Looking at G10 currencies, true to form and responding to their usual risk sensitive nature, the NZD and AUD have led the gains against the USD with both pairs up around 1.30%. AUD now trades at 0.7312, back above the figure after spending the previous 9 days with a 72 handle. Meanwhile NZD trades at 0.6875, its highest level since late June this year. Focus now is likely to shift to the G20 Trump-Xi meeting where chance for a trade truce remains evenly balanced.

The Euro is also close to the top of the G10 leader board up 0.81% to 1.1371. A lot of market commentary has been focused on the Fed likelihood of blinking, but worth noting here that we think there is a good chance the ECB will have to lower both its growth and inflation projections for 2018 and 2019. EU economic activity has continued to slowdown and lower oil prices will also play into the inflation equation for next year, so while there is clearly a risk the Fed will blink in December (lowering the 2019 dots), ahead of the Fed’s meeting we could well see the ECB blinking on December 13th. Add to that trade, Brexit and Italian uncertainties and it might be too early to call the end of the USD supremacy.

Elsewhere, the GBP didn’t see much impact from both the UK Treasury and BoE’s risk assessments of Brexit scenarios, although it has risen back above 1.28 following Powell’s speech (+0.7% on the day). The Treasury forecast a no-deal scenario would lead to a 9.3% hit to UK GDP over 15 years, while BoE forecast that the GBP would fall 25% in such a scenario, leading the Bank to hike rates to 5.5% to control inflation. Overall, the UK will be poorer economically under any form of Brexit, compared with staying in the EU. The Treasury didn’t model the recently agreed deal with the EU, but a close variant (the Chequers agreement) would see GDP 3.9% lower in 15 years. Meanwhile, talk of a second referendum is continuing to grow. Labour’s shadow chancellor john McDonnell told the BBC overnight that its “policy is if we can’t get a general election, then the other option which we’ve kept on the table is a people’s vote.”

US rates have fallen and the curve has steepened in response to the Powell speech. The Fed sensitive 2y rate is 3.6bpos lower to 2.798% and the 10y rate is 1bps lower to 3.053%. Early in Europe Italian 10y BTTPS fell 3.3bps to 3.25% and 10y bunds were unchanged at 0.348%.

Yesterday copper was the big loser and today is the big winner by a mile. The corroding metal is up 3.28% followed by base metals up close to 1%, both probably reflecting the improvement in risk appetite. Oil prices in the meantime are relatively stable, down about 0.5%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.