Total spending grew 0.9% in June.

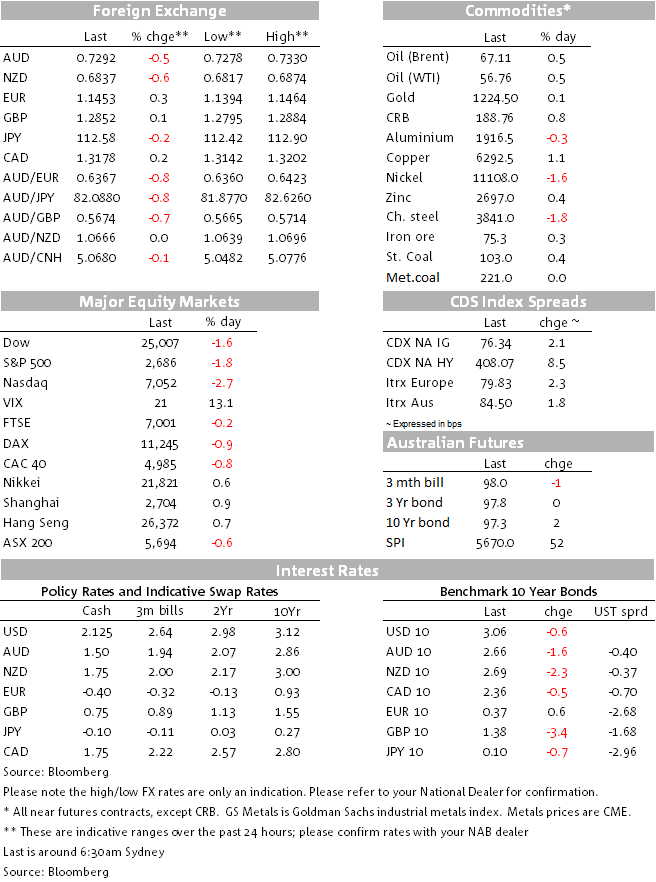

US stocks take a big hit. The Aussie and New Zealand dollars seem to have come off the worst out of the major currencies with a rise in uncertainty, whereas Sterling has risen.

https://soundcloud.com/user-291029717/wall-street-takes-a-hit-with-more-us-china-tensions

With an hour of US trade left to go, it’s so far proving to be a bad day for US equities, with the Dow and S&P off 1.6-1.9% and the NASDAQ a cooler 2.7%. The ‘FAANG’ sector is again driving the broader market weakness (the IT sector is off 4% within the S&P500), with Apple off another 3.5% on new reports of reductions in orders for three iPhone models – the stock is now 20% off its early October record high – and Facebook off 5% in conjunction with an ongoing purge of social media-related stocks in part on ongoing speculation regulation is coming to the sector.

US stocks weakness follows a 7% plunge in the ADRs of Nissan and near 10% decline in its European partner Renault after the group’s Chairman Carlos Ghosn was arrested in Tokyo on charges of financial fraud (underreporting income, allegedly) and ousted from the firm.

Adding fuel to a weak opening for US stocks and bid for US bonds has been the US NAHB survey (homebuilder sentiment) which plunged by 8 point to 60 (vs the 1-point drop expected), its biggest drop in four years and lowest since August 2016. The NAHB said “customers are taking a pause due to concerns over rising interest rates and home prices”. NAHB also argue that “the decline of builder confidence should be noted by policymakers…given that housing leads the economy”.

Last week, recall, Fed chair Jay Powell acknowledged weakness in the housing sector, though downplayed its significance for the broader economy, suggesting it was less of an influence on aggregate economic activity than in the past.

In the last few hours, we’ve heard from the (highly influential) NY Fed president John Williams in a Q&A event in the Bronx, who has failed to provide succour for the dovish interpretation that market chose to place on last Friday’s various Fed speakers. “We’ll be likely raising interest rates somewhat but it’s really in the context of a very strong economy,” Williams said. “We’re not on a pre-set course. We’ll adjust how we do monetary policy to do our best to keep this economy going strong with low inflation.”

Weaker US stocks and the aforementioned NAHB survey look to have taken up the mantle from interpretation of last week’s Fed speak to see the 2-year US note off another 2bps to 2.78% and 10s -1bps to 3.057% (they were last lower at the early stages of the October US stock market slide). US 10-year ‘break even’ inflation rates, the benchmark market-based measure of inflation expectations, have just dipped below 2% for the first time since the start of January. Earlier Monday, 10 year Italian BTP yields jumped by 10.7bps back to the highest levels since October 24th and seemingly weighing somewhat on the Euro in afternoon European trade.

Consistent with the ‘risk-off- market tone in other asset classes, The Swiss Franc sits on top of the G10 FX leader board so far this week (JPY also firmer) and the NZD and the AUD at the bottom, both off a shade over 0.5% and meaning AUD/USD has failed to sustain Friday’s push up clean above 0.73. It’s at 0.7291 now. NOK and CAD are also lower even though oil prices are fairly flat so far this week.

Of some note EUR/USD is performing well despite the latest widening in BTP-Bunds spreads to which is has tended to be quite highly correlated and weighed on the single currency in European trade. This is testament to the Euro’s partial safe-haven characteristics derived from its big positive ’basic balance’ positon (current account surplus, FDI inflows and long term portfolio flows). EUR/USD gains today also means that the DXY US dollar index is 0.3% don on the day. A slightly firmer pound is also relevant here with as yet no substantial new Brexit news (with as yet no formal challenge to PM May’s Prime Ministership)

WTI crude and Brent are currently indicated up 30 and cents respectively but are jumping around. Base metals are mixed, copper again doing well on top of Friday’s 1.7% gain (+0.9%) aluminium less so (-0.3%). Gold is flat but platinum is continuing to recoup its early month losses, up another $7 or 0.8%. Iron or futures are up 0.5%, metallurgical coal unchanged and steaming coal slightly higher.

RBA Minutes at 11:30 AEDT from the November 6th meeting shouldn’t be market moving in so far as we’ve had the subsequent SoMP, but a speech from Governor Lowe, on ‘Trust and Prosperity’ at the CEDA (Committee for Economic Development (CEDA) annual dinner in Melbourne (19:20 AEDT) will be worth tuning into, including a likely Q&A.

US housing starts are and building permits are the only significant offshore release, of added interest following the plunge in the NAHB index.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.