NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The markets have been treading water ahead of the meeting between Presidents Trump and Xi at the G20 this weekend, impacted a little by the news that Peter Navarro might also be attending the dinner.

https://soundcloud.com/user-291029717/trump-xi-and-navarro

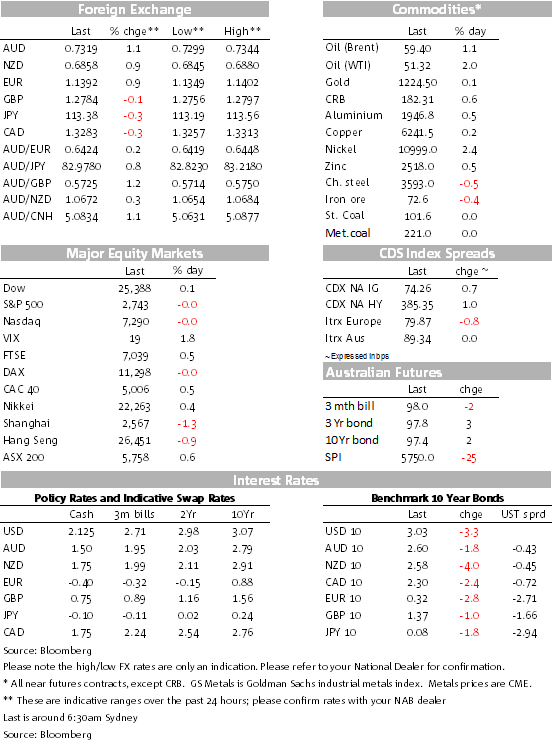

Markets have been choppy this morning amid varying views on the prospect of any sort of trade deal this weekend between Trump and Xi at the G20. Oil has been especially volatile, initially taking more heat before it was reported that Russia might join OPEC in limiting supply. The latest readings on German and US inflation have underwhelmed expectations, but activity indicators have generally better, except for US housing. The AUD has perked up a little beyond 0.73 since the release of the FOMC Minutes this morning pointing to more rate flexibility ahead after a December hike, also pushing US equities back into the black.

There have been conflicting reports ahead of Xi and Trump’s highly anticipated and important dinner meeting Saturday night in Argentina, after the G20 summit.

Rather than jump at headlines, the market has taken a laid-back approach and prices are treading water until we see the outcome. Early in the day, Trump tweeted the merits of his tariff policy and, as he was leaving for the G20, told reporters that the US was very close to a deal with China, but added “I don’t know if we want to do it. I’m open to making a deal, but frankly, I like the deal we have now”, the latter comment implying he liked the tariffs in place that might put pressure on China to change its policies.

The WSJ reported that the US and China, “looking to defuse tensions and boost markets, are exploring a trade deal in which Washington would suspend further tariffs through the spring in exchange for new talks looking at big changes in Chinese economic policy”. This contradicts Trump’s comments last week that he thought it highly unlikely he would suspend the proposed increase in tariffs on 1 January.

Separately, the South China Morning Post reported that White House advisor Navarro – a China hawk – will now attend the Xi-Trump dinner this weekend after reports last week that he wouldn’t. We also note that bubbling away in the background, former Trump lawyer Michael Cohen is expected to plead guilty to charges of misstatements to Congress over statements about Russia during the 2017 election campaign. He has been assisting the Mueller Trump-Russia probe with extensive interviews. Trump called Cohen “weak” and a “liar”.

It’s been a choppy night for currencies. The USD has been whippy and non-directional, testing both ends of it recent ranges. Oil seemed to be a factor, the USD following the better fortunes of US equities into the FOMC Minutes, before giving back some rate ground since.

After earlier testing 0.7340, the AUD/USD traded down to the figure, before again pushing 15-20bps higher after the release of the FOMC Minutes this morning into the last two hours of the US session. Sterling has been bleeding further, AUD/GBP up above 0.57 this morning on little sterling news. And we didn’t even mention the B word on the Morning Call today.

Inflation has been under focus this morning with the release of Germany’s November CPI and the US October PCE deflators. Both missed expectations, the EU-harmonised CPI coming in at 0.1%/2.2% against expectations of 0.2%/2.3% (and seemingly not from oil that’s still to come). The US Core PCE deflator came in at 0.1%/1.8% from a downwardly revised 0.2%/1.9% and short of the consensus 0.2%/1.9%. This only plays to the theme that buys more time for the ECB to ponder when they might begin to exit from negative rates and for the Fed to be increasingly data dependent and cautious with rates approaching neutral.

The FOMC Minutes released this morning said that another rise in the Fed funds rate would likely be warranted “fairly soon” (i.e. December), but introducing more flexibility ahead, members discussing modifying the language on gradual rate hikes ahead. Of course, from the opposite perspective, should activity continue with momentum and inflation surprise on the high side, that would mean rate acceleration. But for now at least, inflation is benign, as we saw with the PCE deflators, the core deflator running at an annualised rate of 1.6% in the past six months.

Separately, Euro-zone confidence surveys for November were mixed, the Business Climate Indicator up from 1.01 to 1.09, but consumer confidence steady at -3.9. In the US, while inflation was low, real consumption grew 0.4% in October, the Atlanta Fed lifting its Q4 GDPNow estimate to 2.6% from 2.5% on higher consumption now expected to be 3.2% in Q4. While consumption remains solid, housing continues to soften, pending home sales down 2.6% in October. Weekly jobless claims also pushed higher to 234K from 224K, the highest since July, though some attribute this to normal noise around Thanksgiving. It does throw more attention on next week’s payrolls.

The big mover overnight has been oil, initially lower before doing a quick about face on expectations Russia will join OPEC in limiting production, OPEC meeting December 6. WTI traded first to a new 13m low of below $49.50, but is now trading at $51.36, up over 2% for the day, Brent up 1% to $59.37. Treasury yields followed oil and equities lower in the first instance, 10y yields testing 3% before rising to 3.03% as we write. Base metals are mostly a little higher, gold is steady with bulk commodities not eliciting too much new for analysts.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.