Online retail sales growth slowed in May following a fairly strong April

Insight

There’s certainly a more cautious mood today.

https://soundcloud.com/user-291029717/caution-ahead-of-a-busy-day

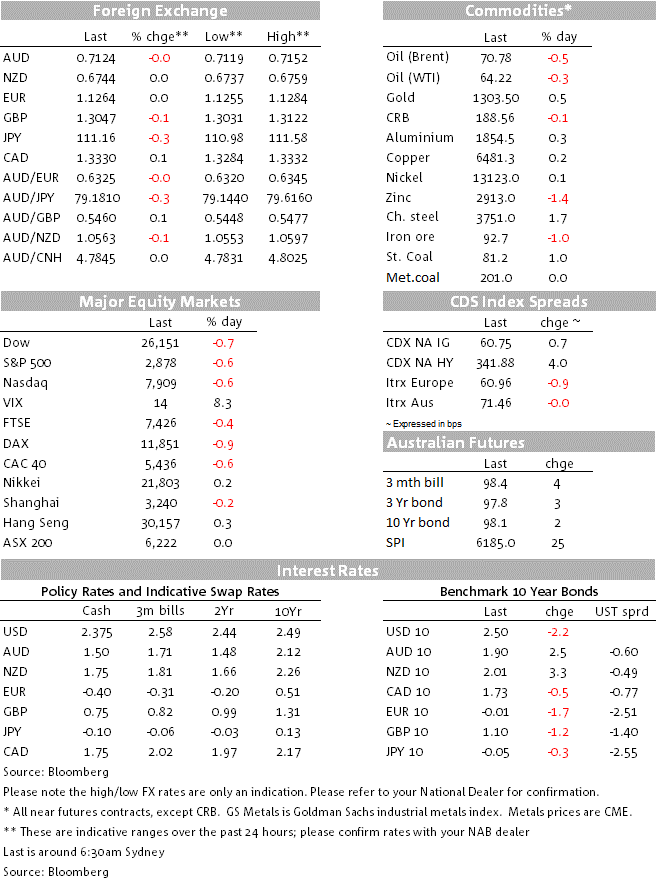

Markets have traded in a cautious mood overnight ahead of key risk events over the next 24 hours, including RBA Debelle speech this morning ahead of ECB meeting, EU Brexit summit and US CPI tonight followed by the FOMC Minutes early tomorrow morning. European and US equities closed in negative territory with the S&P 500 recording its first negative close in 9 days. Core global yields are a couple of bps lower while currency moves have been relatively subdued. AUD is unchanged after again failing to hold a move above 0.7150.

All major European equity indices closed in negative territory although they showed little reaction at the open to news the US Trade Representative was considering tariffs on EU products worth $11bn (ranging from large commercial aircraft to dairy products and wine) as retaliation over Airbus subsidies ahead of a WTO ruling. Unsurprisingly, President Trump didn’t miss the opportunity to send a tweet, noting “The EU has taken advantage of the US on trade for many years. It will soon stop!” If the US goes through with the tariffs, the EU has said it will impose countermeasures, raising the risk of further escalation. The sums involved at this stage of course pale in comparison to the US tariffs imposed on China, which cover more than $250b of imports. The move has been seen as an increase in US pressure on the EU amid a lack of progress in trade talks that have been going on for nearly a year. US equities also closed lower across the board with Caterpillar and Boeing leading the DJ decline while airlines also underperformed.

Not helping sentiment either, the IMF downgraded its global growth outlook for the third time in six months and its forecast is now the lowest since the financial crisis. The IMF cut its forecast for global growth this year to 3.3%, down from 3.5% in January, describing this as a “delicate moment” with multiple downside risks, and one in which policymakers should avoid missteps. The IMF lowered both its US (2.3% from 2.5%) and European (1.3% from 1.6%) growth forecasts, although, more promisingly, it revised up its Chinese growth forecast by 0.1% to 6.3%. Encouragingly global economic growth is expected to recover in the second half of this year, before plateauing at 3.6 % next year.

The US small business sentiment (NFIB) survey also elicited little reaction by the market. The index was little changed in March after its sharp fall – from what was close to an all-time high – the previous month. According to the text of the report, “Overall, the Index anticipates solid growth, keeping the economy at “full employment” with no signs of a recession in the near term.” Meanwhile, US job openings fell sharply in February, although the series can be volatile month-to-month, prone to revision, and it remains near record high levels.

The cautious mood was similarly evident in the bond market with core global bond yields also lower. 10y Bunds closed 1.6bps down to -0.01% while the 10 year UST yield is down 2bps to 2.50%.

Currency moves have also been very subdued, USD indices are little changed and barring the gains in JPY (+0.32%), all other G10 pairs moves have been contained within +/-0.10%.

Risk aversion plays into the modest JPY strength with USD/JPY now trading at ¥111.14, after briefly trading below the figure overnight. GBP has had another volatile night trading to a high of 1.3122 early in the session, then going down to 1.3030 early this morning and now looking a bit more settle at 1.3050. Ahead of the EU Brexit summit tonight, PM May has been visiting German and French leaders, Merkel and Macron with little new news. Technically all options remain open, but at this stage it seems that it is more likely than not that PM May will agree to an EU longer extension offer, perhaps to April 2020 – but one that gives May a break-clause to allow it to leave earlier if a deal can be cobbled together earlier. An extension to Brexit beyond 30th June may see a modest relief rally in the GBP, although by kicking the can down the road, the risk of elections as well as the possibility of a second referendum will likely keep GBP gains contained for now. Reaction from Pro-Leave Tories and Pro-second referendum Labour MPs will be important.

The AUD traded to an overnight high of 0.7152, but as it has been the case since early February the pair was unable to sustain a move above 0.7150. The positive vibes from US- China trade negotiations, coupled with better than expected China and Australian data releases have played into a stronger AUD of late. The aussie, however, is a risk sensitive currency and given the number of risk events over the next 24 hours it seem reasonable for the pair to trade with a cautious tone

At 1.40pm AEST RBA Deputy Governor Debelle is scheduled to speak on the ‘State of the Economy’. We think the speech could prove important given the RBA tweaked the policy paragraph of its interest rate decision early in April, which was the first change in years. In the Statement the RBA said, “The Board will continue to monitor developments and set monetary policy to support sustainable growth in the economy and achieve the inflation target over time”.

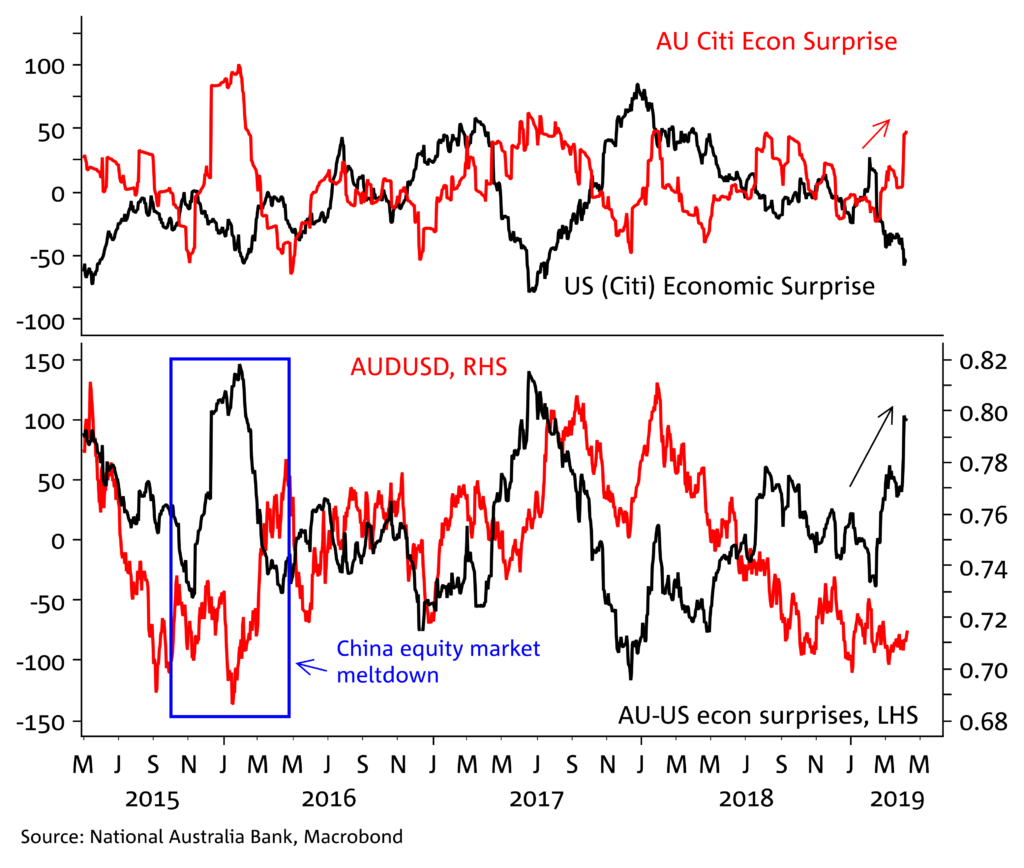

Using Citi’s economic data surprise index, recent data releases in Australia have mostly printed on the better side of expectations and in fact when compared with the generally disappointing US economic data releases, the improvement in Australia’s data releases has been quite impressive and supportive of a stronger AUD (see chart of the day below). One could argue then that the better Australian data releases of late do not provide a smoking gun for Deputy Governor Debelle to signal an imminent change in policy guidance. However, we know the RBA is biding its time in order to better assess how the tension between the strength in the labour market and slowdown in GDP growth resolves its self. If we add to that the ongoing weakness in housing market including its impact on housing construction, employment and wealth effect, then we think Debelle has plenty of ammunition to signal a new round of RBA easing could be in the offing. Our economists believe that consumer spending is likely to remain weak, underpinning an outlook of sluggish GDP growth in the low 2s. We expect the RBA to cuts twice this year, pencilling in the first cut in July, but see a clear risk that the RBA acts quickly given we expect it will downgrade its growth and inflation outlook in May.

US: NFIB small business optimism, Mar: 101.8 vs. 102 exp.

US: JOLTS job openings (k), Feb: 7087 vs. 7566 exp.

NZ- REINZ House Sales (Mar)

JN- PPI, Core Machine Orders Feb, Machine Tool Orders (Mar P), BOJ Kuroda speaks

AU – Westpac Consumer Conf Index (Apr), RBA’s Debelle gives speech in Adelaide titled “The State of the Economy“

UK – Trade Balance (Feb), UK Industrial Production (Feb), Industrial Production (Feb), GDP (Feb)

EC – ECB policy meeting, ECB’s Draghi speaks in Frankfurt after Policy Decision

There have been reports President Draghi was considering pushing out forward guidance (currently “interest rates to remain at their present levels at least through the end of 2019”) and discuss a tiered deposit rate for banks. However, follow up reports suggest the Council is not that keen on the idea. Draghi’s steps down as ECB president at the end of October, so some have suggested that he may find some resistance to the provision of policy guidance beyond his term. Given it is a meeting without new forecasts, a policy change announcement seems unlikely, but amid recent soft data releases it is hard not to expect anything but a dovish tone from Draghi at the post meeting press conference. Note we should also get more details on the already-announced TLTRO.

US – MBA Mortgage Applications, CPI (Mar), FOMC Meeting Minutes, Fed Clarida is on speaking duties

March inflation is likely to remain muted, allowing the Fed to be patient. Our core model of US CPI is suggestive of an on consensus +0.2% m/m print (Chart 2). However, the risk is more likely to the downside due to the shifting timing of Easter (this year Easter Sunday is 21 April compared to 1 April last year) and a high rate of retail store closures which is likely leading to higher than normal liquidation sales. The Minutes should provide detail on the Fed’s balance sheet and a bit more colour around the risks to the Fed’s pencilling in of 1 hike in 2020 (a rate cut now 68% priced by the end of 2019).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.