Online retail sales growth slowed in May following a fairly strong April

Insight

Chinese authorities issued a Q&A which seems to have buoyed markets a little.

Today’s podcast

https://soundcloud.com/user-291029717/chinas-qa-mays-legal-advice-and-australias-gdp

It’s not often you can say that a central bank outside of Australia other that the Federal Reserve is capable of moving the Aussie dollar, but that is what happened last night after the Bank of Canada issued a dovish statement following its ‘no change’ rates decision, arguing that sharply lower oil prices of late – and for Canadian crude note much more so that global benchmarks – will have both some negative impact on activity as well as allowing for a longer period of non-inflationary growth.

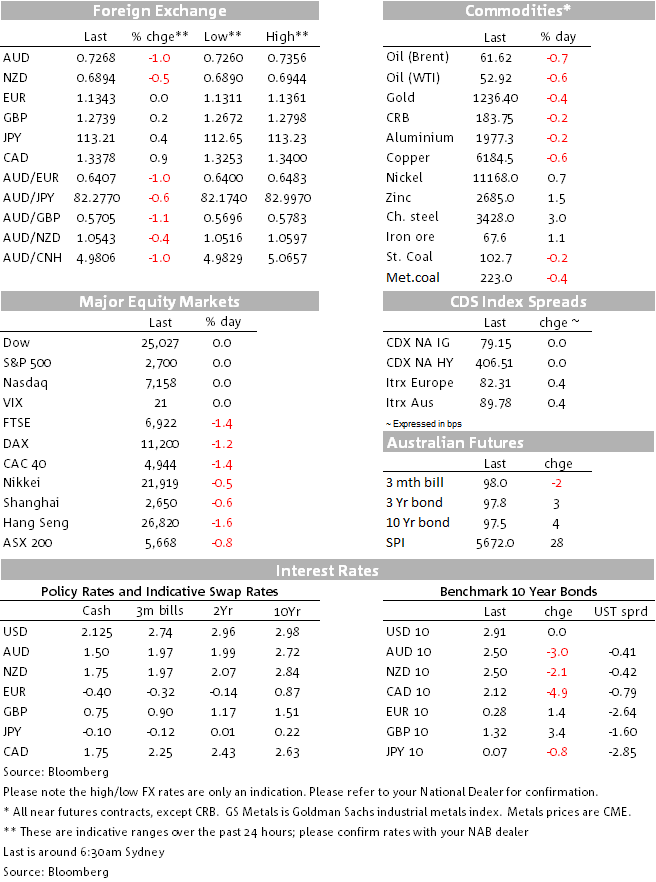

The BoC statement saw the implied probability of the next rate rise occurring after the January meeting fall from about 65% to less than 25%. March is though still priced at more than 50% with the BoC reiterating that rates still need to rise to closer to neutral (from 1.75% now). The Canadian dollar immediately rose by about 0.9% with USD/CAD hitting its highest level since June 2017 at 1.3400. The move imparted some collateral damage on the AUD and NZD, AUD/USD pulled down from 0.7300 to 0.7260 (0.7267 now) and NZD/USD from around 0.6925 to sub 0.69 (0.6894 now). Fonterra has just updated its milk price forecasts and where the mid-point of their range (NZ$6.25-6.50kg for 2018-19) is a bit higher than analysts’ estimates, though this hasn’t moved the kiwi.

AUD/USD earlier fell from around 0.7350 to sub-0.73 on the weaker than expected 0.3% GDP print, and which left annual growth as of Q3 at 2.8% after negative revisions, well below the RBA’s forecast of 3.5% growth this year and next, restated in Tuesday’s post meeting statement. Following the latest releases of growth, labour market and prices data, NAB is reassessing its view on monetary policy. While growth has turned out broadly as we expected over 2018, inflation has been weaker and the RBA appears more patient. An updated set of growth and rates forecasts will be published next week.

Elsewhere the Japanese yen is a little weaker, aided by a better risk tone after yesterday’s comments from China describing the Trump-Xi meeting as ‘very successful’, affirming a commitment to push forward trade negotiations over the next 90 days and, related to this, reports that the wheels were already in motion for China to restart imports of Soybeans and LNG. Partly because of this, European stocks overnight fared much less badly than Wall Street did on Tuesday (and where most of the falls occurred after the European close). S&P 500 futures (the ‘e-mini’) are up around 0.6%. Cash stocks and bonds were of course both closed for the state funeral of George H W Bush.

The British pound (+0.2%) is a firmer despite a much weaker than expected services PMI report of 50.4 down from 52.2 and 52.5 expected and which contained some pretty dire warnings about how services might fare in coming months. Helping GBP was Tuesday night’s UK parliamentary approval of a bill that would give it the say in ‘what happens next’ if the Brexit Withdrawal Bill is defeated next week (as seem likely). This is seen to reduce the risk of no deal/hard Brexit ‘crash out’ come next March.

GBP gains have held up EUR/USD but it’s the CAD’s 9.1% weight in the DXY dollar index that means the latter is slightly up on the day (+0.05% at 97.1).

No trading is US bonds overnight. The key feature of European bond trading was a further fall in Italian yields, 10yr BTPs off another 9.5bps (Spread to German Bunds now in to 278bps). Italy’s PM Giuseppe Conte is due to meet with the EU’s Jean-Claude Juncker today with new budget proposals.

Focus has been on oil, where the preliminary meetings ahead of the formal OPEC discussions today indicate agreement to some sort of production cuts with as yet no agreement on how much (1.1mn is one figures being bandies bout). US President Trump has though against been out railing against any output cuts from OPEC+. Crude prices are currently lower on the day, by around 0.5%. It’s a fairly mixed performance elsewhere with precious metals mostly lower, non-ferrous base metals mixed, iron ore futures about 1% up and both coals slightly lower.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.