NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Todays Podcast UK gilts lead global bond yields higher, Italy and France also up a lot, budget news hurts Treasuries recoil ~10bps from new (4.685%) high ahead of expected government shutdown tomorrow This plus reduced UAW pay demands, news of possible Xi-Biden meet, boosts US equity sentiment, AUD/USD recovers more than 1% of recent losses […]

Good morning

And it’s hell to pay when the fiddler stops, It’s closing time, (Closing time), (Closing time), (Closing time) – Leonard Cohen

Thursday’s Economic releases:

NZ: ANZ activity outlook (net%), Sep: 11 vs. 11 prev.

AU: Retail sales (m/m%), Aug: 0.2 vs. 0.3 exp.

EC: Economic confidence, Sep: 93.3 (unchanged) vs. 92.4 exp.

GE: CPI EU harmonised (m/m%), Sep: 0.2 vs. 0.3 exp.

GE: CPI EU harmonised (y/y%), Sep: 4.3 vs. 4.5 exp.

US: GDP (saar q/q%), Q2: 2.1 vs. 2.2 exp.

US: Initial jobless claims (k), Sep-23: 204 vs. 215 exp.

US: Pending home sales (m/m%), Aug: -7.1 vs. -1.0 exp.

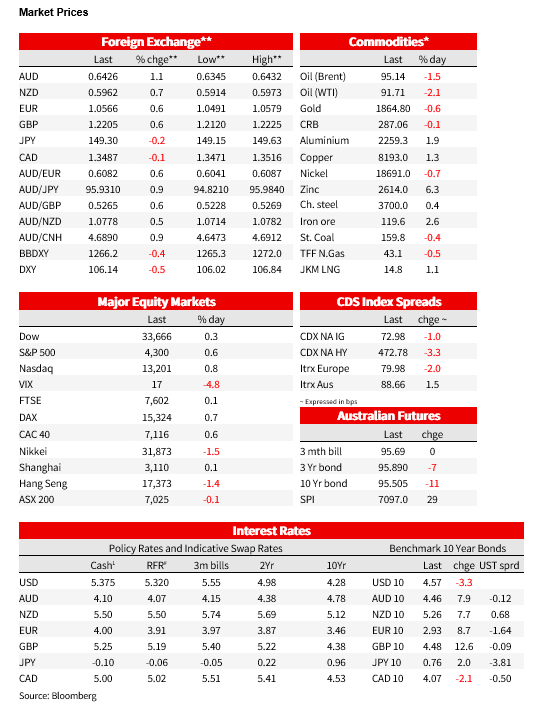

Another day another rise in bond yields Thursday, though in the case of US Treasuries there has been a big recoil from a high of 4.685% down to 4.58% in afternoon New York trade. This is in contrast to Europe where yields rose sharply then stayed there. Gilts are up 12bps on the day and Eurozone benchmarks, both core and periphery, by between 8 and 10bps, including the Italian BTP spread over equivalent German Bunds blowing out to 200bps – its widest since March. Here, Italy’s new budget now envisages a 4.3% deficit next year, up from 3.7% projected in April, with France also blowing out – projected at 4.4% next year and not returning to within the old 3% Maastricht EMU treaty limit before 2027. In contrast, German, Spain, and Dutch deficits are projected to be inside the 3% limit. Quite why gilt yields have done as much as they have is a bit of a mystery, but they have of course been a big outperformer in the wake of last week’s BoE no-change rates decision.

Higher Eurozone yields came despite German inflation falling to a two-year low and slightly below market expectations at 0.2% m/m and 4.3% y/y, the latter plunging from 6.4% due to base effects (the reversal of the last July’s rail fare subsidy which boosted the August 2022 figures). Annual CPI inflation in Spain also undershot expectations by 0.1% at 3.2%, albeit up from 2.4%. This is ahead of pan-Eurozone, later today (see Coming Up below).

US economic data was mixed. US Q2 GDP was unrevised at 2.1% but there was a significant revision in the composition, with consumer spending up an annualised 0.8%, its weakest pace in a year, and revised down from 1.7%, offset by an upgrade to business investment. Initial jobless claims remained low, rising just 2k to 204k. Pending home sales, a leading indicator of existing home sales, plunged 7.1% m/m in August, a much greater fall than expected and raising question marks about the health of the housing market in the face of higher mortgage rates (in contradiction of claims made by Federal reserve Board member Michelle Bowman last weekend).

Incoming Fed speak is from Chicago Fed President Austin Goolsbee, who noted “The unwinding of supply shocks, the composition of demand returning to more stable patterns, and Fed credibility are central to why I think it might be possible today to reduce inflation while avoiding a deep recession,” he said. He went on to warn about the risks of the Fed overtightening but didn’t say whether he favours another increase or not, though he called progress so far on inflation “really excellent.”

Note Fed chair Powell is delivering a Town Hall as we write – his prepared remarks contained no reference to the economy or monetary policy.

US equities have finally had a decent ‘up’ days and here, news of progress in narrowing the worker/employer gap in the current UAW dispute has helped, and too news reports suggesting a possible visit to the United States by China’s President Xi in November. On the former, Bloomberg reports UAW union officials reducing its pay demand from 40% to 36% (employers have so far offered 20%) but also that union officials want to emerge from the strike with ‘at least’ a 30% rise. Auto stocks rallied on this news.

FX markets have been lively , with AUD/USD pulling up from Wednesday’s 0.6332 (new) low to as high as 0.6432. Better risk sentiment, the fall back in US Treasury yields (but not in Australia overnight) and USD/CNY back down through 7.30 all look to have had a hand. Being the last day of the month/quarter, there will be some speculation of hedge-adjustment related supply of AUD/USD today/tonight, but given the scale of equity market declines this month, we wonder whether much of this may have bene done dynamically already? Currency gains elsewhere have ranged from 0.1% (CAD) to 0.7% for the CHF (beyond another outsized (+1.4%) jump in the SEK

Yesterday, local Retail Sales rose 0.2% m/m in August. While this is a subdued pace of growth, the industry splits were more mixed and suggests resilience in discretionary retail categories. There were relatively strong increases in ‘cafes, restaurants and takeaway food services’ (+0.7% m/m), ‘clothing, footwear and personal accessory retailing’ (+1.3% m/m), ‘other retailing’ (+0.7% m/m), and department stores (+0.4% m/m). Weakness was concentrated in ‘food retailing’ (-0.3% m/m) and ‘household goods retailing’ (-0.4% m/m). (Much) warmer than usual August weather was cited by the Statistician as having a hand in boosting discretionary spending (e.g., clothing) with the Women’s World Cup also cited as a positive influence.

Coming Up

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.