Online retail sales growth slowed in May following a fairly strong April

Insight

The US President is keeping everyone guessing on further tariffs on Chinese imports.

https://soundcloud.com/user-291029717/trump-blows-hot-and-cold-on-china

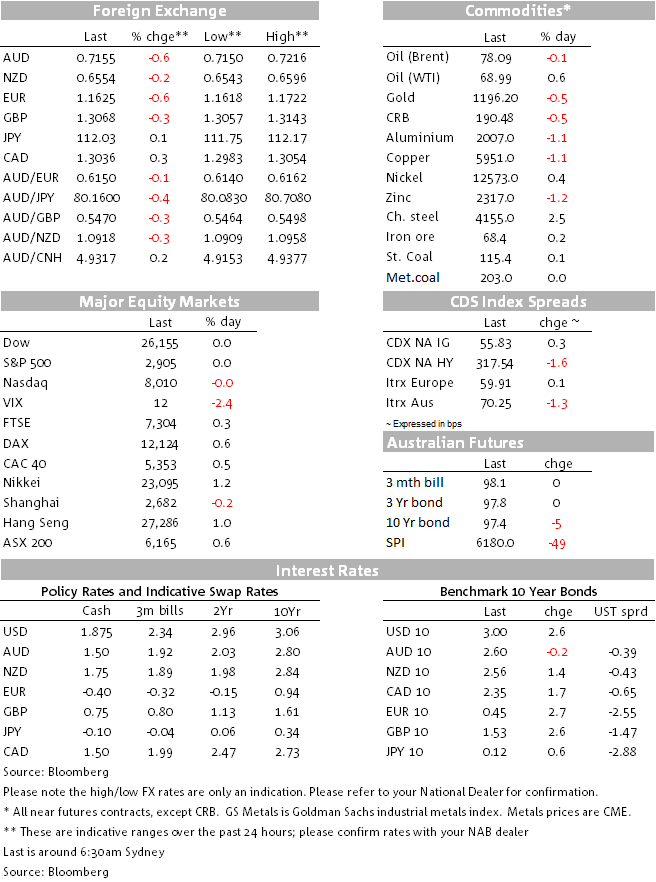

An otherwise positive Friday for risk sentiment, bond yields (higher) and the US dollar, aided by a reasonably strong set of US economic data, was punctuated late Friday by a Bloomberg source story saying that President Trump has issues instructions to officials to proceed with the long-threatened tariffs on an additional $200bn of Chinese imports, albeit with no specifics as to exact timing or magnitude. This further supported the US dollar via its safe-haven characteristics, seeing AUD, NZD and most EM currencies lose ground in the last few hours of NY trade, but both US stocks and Treasury yields recovered from an intra-day dip to close back near the highs – in the case of 10-year Treasuries, almost bang on 3% (2.995%).

Subsequent to Friday’s reports, over the weekend the WSJ, et al, has reported that an announcement on the tariffs should be forthcoming either today or tomorrow, but that the initial tariff rates would be 10%, not the threatened 25%. That’s the ‘good’ news (given what has surely now been close to being priced in). The bad news is that in moving so soon after US Treasury Secretary Steve Mnuchin had extended an invitation to his counterpart, Chinese economic czar Liu He, to attend fresh talks in Washington, China is now minded to give the US the cold shoulder and rsvp in the negative.

AUD and NZD market have been left somewhat flat-footed by weekend developments, currently both trading close to their Friday night NY closing levels.

In a re-run of the previous Friday, the US dollar benefited from both higher Treasury yields and safe haven demand. USD indices added about 0.5% with DXY coming within kissing distance of 95 and closing at 94.97. SEK was the standout loser, failing to recover from the early European day hit on weaker than expected CPI. AUD/USD made an intra-day high of 0.7216 after we went home but fell about 25 pips (from 0.7180 to 0.7154 at NY close) post the Bloomberg tariff report. On the week, DXY and BBDXY are both about 0.5% lower (improved risk sentiment on trade outweighing higher US yields) with NOK the best performer on higher oil followed by GBP on Brexit Transition Agreement optimism, then CAD on oil prices and NAFTA hopes.

A nothing day for US stocks Friday, all the main indices ending close to flat, though notable that the S&P full recovered from the 0.4% hit on the early afternoon Trump tariff report. On the week the Nikkei is the standout winner, the rise in USD/JPY doubtless a contributor, while Shanghai is the only index to be lower:

10yr Treasuries twice flirted with the 3.0% level on Friday but failed to sustain the initial break (high of 3.0014% first up, 2.999% on the second and closing at 2.995%). The US data was helpful to the cause of higher yields, while perhaps the more telling story was that yields pulled back up to 3% after initially falling back by 2bps or so on the Bloomberg Trump tariff story. On the day, 10s added 2.6bps and 2s 2.1bps. On the week, it’s been a bear-flattening theme, 2s +7.5bps and 10s +5.6bps, with the belly performing worse (5s +8.2bps). Futures implied AU 10-year yields rise by 2.5bps about during the offshore (Sycom) session such that the spread under US 10-year Treasuries has narrowed by about 2.5bps on the week.

Another very mixed performance in commodities Friday, exchange traded metals all lower bar lead but iron ore slightly higher as too steaming (but not met.) coal. WTI crude was up but Brent slightly lower (this following big falls for both on Thursday on the view that Florence-related supply disruptions wouldn’t be too bad).

On the week met. coal, up 8%, is the big story as far as Australia is concerned, followed by oil – the latter higher on supply concerns linked more to the approach of Iran sanctions than hurricanes and including perhaps a dose of realism regarding how able and how quickly other producers will be to pick up the shortfall, assuming Iranian exports drop back to their 2006 pre-sanctions levels (about 1 million bpd down on now). Related to this, we are hearing and reading more about the potential for Iran to provoke greater civil unrest in Iraq (Shias on Shias), in particular around Basra, Iraq’s main port from where some 3.5mn bpd of Iraqi oil is currently shipped:

China August new home prices +1.49% vs 1.21% in July; yr/yr 8.0% up from 6.6%

US August retail sales +0.1% (0.4%E, 0.7%P revised from 0.5%).

US August ‘control’ sales +0.1% (0.4%E, 0.8%P revised from 0.5%, June revised to 0.0% from -0.1%

US August sales ex-autos +0.3% (0.5%E, 0.9%P revised from 0.6%)

US August industrial production +0.4% (0.3%E, 0.4%P revised from 0.1%, June 0.6% from 1.0%

US August manufacturing production 0.2% (0.3%E, 0.3%P)

University of Michigan preliminary Sep. consumer sentiment 100.8 (96.6E) from 96.2 in August

UoM 5-10yr inflation expectations 2.4% from 2.6% (now below the 2.5% 2017 average)

UoM 1yr inflation expectations (less important to the Fed) 2.8% from 3.0%

US August import prices -0.6%m/m (-0.2%E); yr/yr 3.7% down from 4.9% and 4.2%E

Sweden August CPI 2.0% (2.2%E, 2.1%P)

Sweden CPIF 2.2% (2.3%E, 2.2%P)

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 55% is a new low for the year but coms on higher auction volumes (1,985 vs.1,916 last weekend). It compares to last week’s final 55.3%, and the final rate this weekend should end up well below this.

Melbourne cleared a preliminary 57.2% against a final 60% last weekend and Sydney 52.6% vs. a 50.6% final rates last week. Since last week’s preliminary clearance rate in Sydney was 57.8% there’s a very good chance this weekend’s final rate comes in well below 50%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.