Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

We’re ending the week with risk sentiment at its best level of the year.

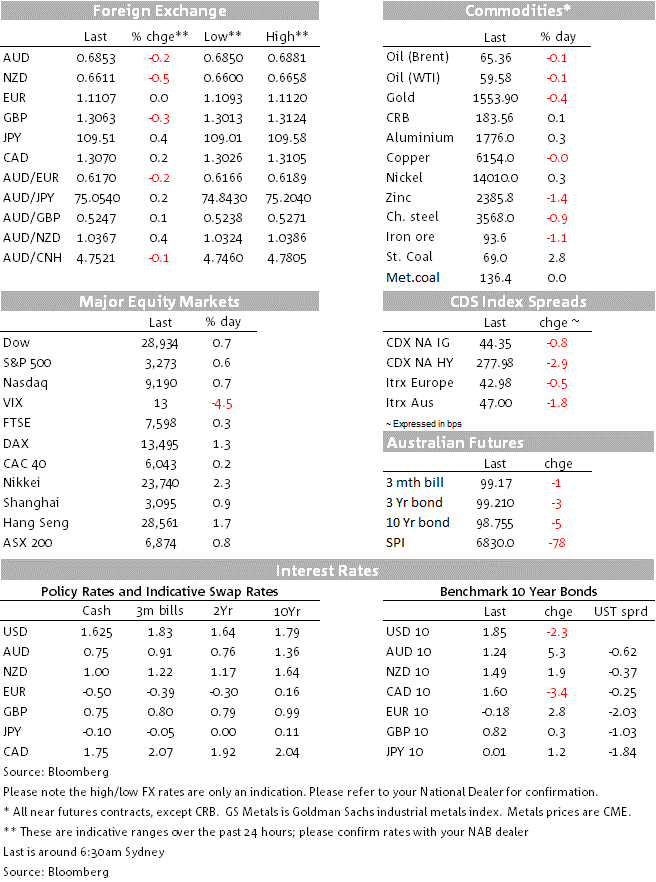

We started the working week, the first of the year for many of us, lamenting the death and destruction (still) being wreaked by Australia’s bushfires, were then distracted on Tuesday and Wednesday by the possible outbreak of WWIII and are ending it, ahead of tonight’s US employment report at least, with risk sentiment at its best level of the year as proxied by the VIX, now back below 13. In FX the USD, for most part negatively correlated with risk sentiment, is currently up over 1% on its end-2019 level.

Equally perplexing is that given current levels of risk sentiment, the AUD finds itself to be the worst performing major currency of 2020 to date, down some 2.5% and once again overnight struggling to gain a firm foothold above 0.6850 (currently 0.6852). This is despite some better economic news on Wednesday and Thursday courtesy of building approvals, job vacancies and, yesterday, better than expected November trade figures. AUD is languishing near the week’s lows despite expectations for a Feb 4 rate cut from the RBA having been pared from 60% at mid-week to about 50% now. Also in the dazed and confused side of the market ledger, the NZD is by far the weakest currency of the past 24 hours, under some fairly relentless selling pressure from early in the European session yesterday on no news, after having flatlined though the local trading day yesterday.

In Europe, German industrial production came in a little stronger than expected at 1.1% (consensus 0.8%) to be -2.6% y/y up from -4.6% in October, but the latest trade numbers were worse than expected, the surplus down to €18.3bn from €21.3bn on weaker than expected exports (-2.3% m/m). The Eurozone unemployment rate was steady at 7.5%. In the US, all we’ve had of note have been weekly jobless claims which fell to 213k from 223k the week before, pulling the 4-week average down to 224k from 233.5k, consistent with still strong employment growth and downward pressure on the unemployment rate.

Central bank speakers have been hitting the wires thick and fast, the most- market moving of which have been from outgoing Bank of England governor Mark Carney, who claimed that the Bank has at least 250 basis points of additional monetary policy space. It has sufficient headroom to “at least double” its August 2016 package of 60 billion pounds ($78 billion) of asset purchases, he said, which would deliver the equivalent of around a 100 basis-point cut to the benchmark, which currently stands at 0.75%. Factoring in forward guidance “adds to this armoury…all told, a reasonable judgment is that the combined conventional and unconventional policy space is in the neighbourhood of the 250 basis points cut to bank rate seen in pre-crisis easing cycles,” Carney said in a speech at the BOE’s Future of Inflation Targeting Conference in London. Moreover, Carney intimated that the Bank is seriously considering using some of that space in short order, saying “The economy has been sluggish, slack has been growing, and inflation is below target….Much hinges on the speed with which domestic confidence returns. As is entirely appropriate, there is a debate at the MPC over the relative merits of near term stimulus to reinforce the expected recovery in U.K. growth and inflation.”

GBP loss almost a cent against the USD following Carney’s remarks, though is currently only 0.3% down on Wednesday’s New York close, faring no worse than the JPY, CAD and SEK – also all -0.3% – and better than the NZD (-0.6%). AUD is 0.2% lower which the EUR and CHF are little changed

CAD is coming back from its worse level either side of comment by Bank of Canada Governor Stephen Poloz, who says he is watching to see if recent labour market moderation persists but also that the Bank is monitoring for renewed signs of froth in the housing market. Latest labour market data is tonight.

Fed speakers have included Charles Evans, Bob Kaplan, Neel Kashkari and James Bullard, none of whom are deviating from a relatively optimistic view of growth in 2020 – indeed some are expressing it with greater confidence in part due to reduced trade uncertainty – and the need to see a material change in the outlook to justify changing rates. Evans say explicitly that he “expects the Fed could go through 2020 without any interest rate changes”. This is also NAB’s view, but with risks skewed heavily in the direction of lower not higher rates.

US equity markets have entered the last hour of trading while the major indices 0.6-0.7% high and meaning the S&P has made a new intra-day record high of 3,275.6. All subsectors of the S&P are in the green while Boeing has recovered all of the losses it suffered on news on the 737 crash soon after take-off from Tehran on Wednesday as more international news agencies and governments report intelligence suggesting the plane was almost certainly shot down. We did find it strange here than the Iranian government could claim mechanical failure minutes after the crash, though a missile strike would do that, wouldn’t it?

US treasury yields are lower but are holding above the levels prevailing prior to Tuesday morning’s news of Iranian strikes on US military installations, 10s -2.5bps to 1.85%, 2s -0.8bp at 1.572 (latter unchanged from where we left them last night). .

Commodity markets see Brent crude 0.1% lower and WTI unchanged (so both benchmarks are now below start of year levels). Base metals are mostly higher (LMEX index up a quarter of a percent) while iron ore is about 1% lower. Gold has lost another $4 as geopolitical tensions further ease, now back at $1,553 having between briefly above $1,600 at mid-week.

AU Retail Sales, the week’s local economic highlight, is due at 11:30 ET. Sales likely strengthened on Black Friday sales and is forecast to show a rise of 0.5% after 0.1% in October, consistent with the NAB Cashless retail sales index. The trend in sales has deteriorated, such that faster growth in November partly reflects the increased popularity of Black Friday/Cyber Monday sales, but where Monday fell in December this year. This shift in spending patterns has been mostly captured in the seasonal adjustment of the data, but if sales exceed our forecast that could reflect a bring forward of Xmas spending, where December sales have become less important over time.

It’s US payrolls Friday where the consensus is for non-farm payroll employment to rise by 160k (with the whisper number likely a bit higher after this week’s ADP and non-manufacturing ISM employment reads, notwithstanding the weak manufacturing ISM employment sub-index). The unemployment rate is seen steady at 3.5% and Average Hourly Earnings also unchanged at 3.1% yr/yr.

Canada also has its December labour market report – hugely volatile of late – with the consensus calling for a 25k rise after -71.2k in November.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.