NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Theresa May and European negotiators have agreed an outline of what the relationship will be after the UK finally leaves the EU which helped the pound today.

https://soundcloud.com/user-291029717/may-helps-pound-up-whilst-us-chows-down

With the US chowing down for the Thanksgiving Day holiday, it could have been a very quiet session but this wasn’t the case with Brexit news prominent. It was the release of a Brexit Declaration setting out the future relationship between the UK and the EC. Supposedly, this was THE document that would form the basis with a Withdrawal Agreement to provide trade and political clarity of a deal that it would get the requisite political support.

Not yet. As observers looked at this 26 page statement of intent document it still raised as many questions as answers, with grave doubts that it would get support in the Commons. It didn’t seem to be a document that was going to get the support of the Tory Brexiteers nor the pro-Europe Tories.

The UK and EU have agreed in principle a draft that pledges an “ambitious, broad, deep and flexible partnership” but without the specific detail observers were seeking. Unlike last week’s Withdrawal Agreement which is legally binding, this political declaration – an executive summary version of the dense legal 500+ page agreement – is not. Bloomberg reported that the draft provides a few concessions, pointing the way towards easy trade in goods – hinting vaguely that the UK will be able to pursue its own trade policy and also stop free movement of people – and offers a way out of the Irish backstop though one apparently that could well be scotched by the DUP.

PM May has been trying to sell the deal to Parliament but is meeting a lot of resistance, this document not convincing the market that it will get through Parliament, with disapproval of the agreement within May’s own Conservative party and the opposing Labour party unlikely to support the deal either.

After EU leaders are expected to rubber stamp this political declaration alongside the Withdrawal Agreement EU at a summit on Sunday, the “meaningful vote” in the UK Parliament is likely in the second week in December. It would be far too optimistic to declare victory on a deal yet.

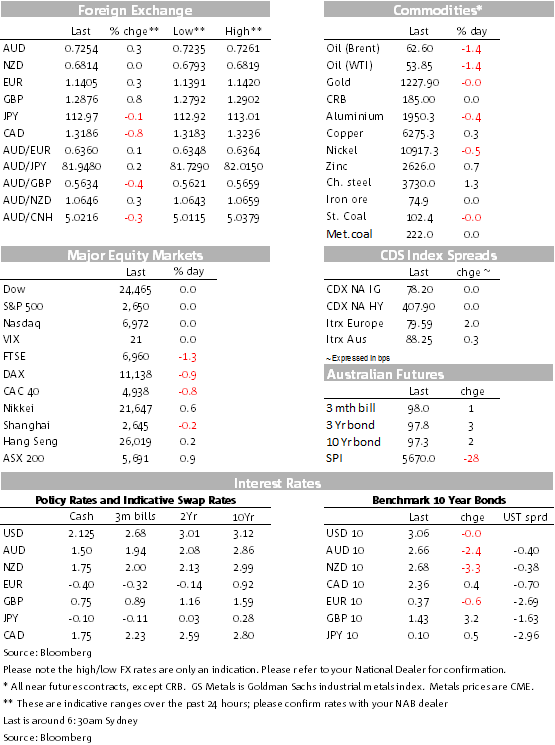

The stronger GBP (up a net 0.7% to 1.2880 this morning) spilled over modestly into EUR support, which is back up through 1.14.

There has also been some positive news on the US-China relationship front over the past 24 hours, but it’s failed (at least for now) to spill over into concerted support for the AUD and NZD, possibly reflecting a steady CNY/CNH.

The South China Morning Post reported that Trump’s trade policy advisor, the anti-China firebrand Peter Navarro (author of “Death by China” before joining the White House) would not be attending the Xi-Trump meeting at the G20 summit in Argentina the end of the month. The report added optimism that US-China trade talks can make some progress (a ceasefire even?), with a possible halt to further import tariffs for as long as negotiations continue. As a show of goodwill, the Chinese government allowed US warships to anchor in Hong Kong after barring them back in September.

In economic news, and ahead of important German and Eurozone PMIs for November tonight, euro-area consumer confidence fell markedly to minus 3.9, the lowest since March 2017. The ECB also released the account of its 24-25 meeting noting “uncertainties and fragilities” affecting the economy, but nevertheless agreeing that they weren’t enough to weaken confidence that the euro zone’s domestic strength will prevail. In their words: “It needed to be emphasized that the incoming data, while somewhat weaker than expected, remained overall consistent with an ongoing broad-based expansion”.

Central bank governors and ECB Governing Council members Weidmann (GE), Knot (NE), and Visco (IT) were speaking on a panel in Florence. No prizes for guessing their views on Euro monetary policy and they didn’t disappoint. Weidmann spoke that central bank bond buying was not to finance government (pushing back against any more QE) and the costs of high inflation (pushing back against retaining negative interest rates). Knot spoke of Italy’s problems while Visco also had a thinly-veiled warning for the Italian government noting the pressures on public debt as long as the interest rate is greater than growth, which it currently is and that Euro governments need to contribute to stability.

Speaking of Italy, there have been conflicting news reports on Italy’s budget standoff against the European Commission. One paper reported that Deputy Premier Di Maio saw “modifications” to the budget possible during the Parliamentary process. Another newspaper reported that Di Maio alongside Salvini would not shift on the budget, “We’re not changing a comma of the budget, we’re going ahead without concessions…if we yield now on the budget the whole structure of our government collapses”.

There was only the slightest of bid tones to European bond markets, coming from declining European stock markets, the Eurostoxx 600 index down 0.7% and the FTSE off 1.28%. German bund yields barely budged (down in yield by less than a basis point), Italian yields down 1.7bps. UK 10 year gilts rose 3.2 bps. Base metals were little changed, while oil eased further, WTI and Brent both down 1.4%, WTI to $53.85 and Brent to $62.60, both re-testing cycle lows.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.