Coming in for landing in a heavy cross wind

Insight

The US dollar is now sitting at its strongest level of 2019 in DXY terms.

https://soundcloud.com/user-291029717/suddenly-nothing-happened

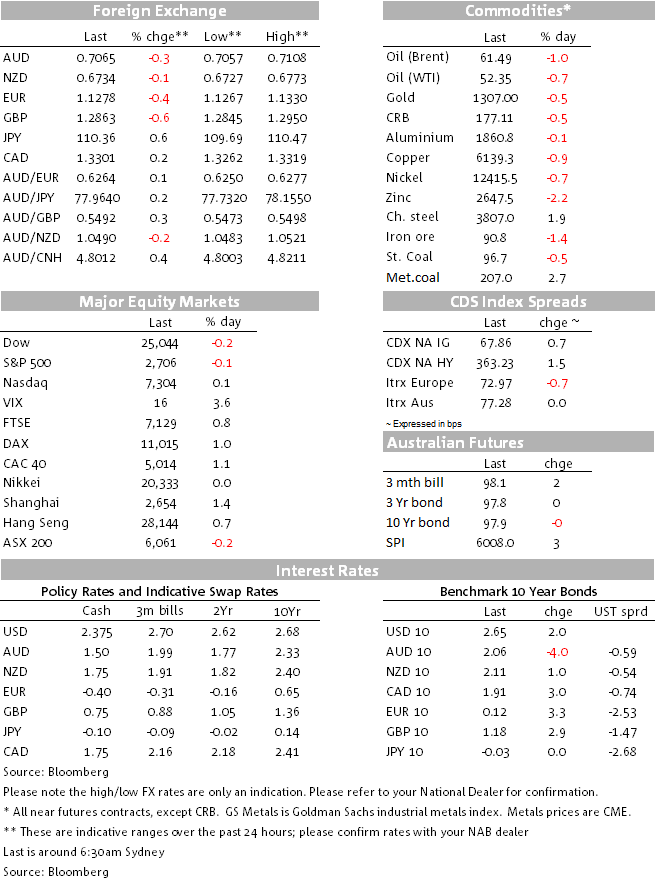

In what has been a slow news night, the outstanding feature of financial markets has been further gains for the US dollar, now sitting at its strongest level of 2019 in DXY terms albeit still comfortably inside the range that has held since mid-2018. This is largely by default, USD again looking like the cleanest dirty shirt in the laundry. Elsewhere equities have come into the last hour of trading narrowly mixed on the day so far, while US Treasury yields – closed during our time zone yesterday – are higher by between 2 and 3bps.

There has been little by way of tangible developments on any of the big uncertainties currently clouding markets. Namely whether or not a fresh government shutdown will be avoided by Friday’s deadline when the continuing resolution funding some departments expires; whether this week’s trade talks, featuring Lighthizer, Mnuchin Liu He will yield anything substantive; and whether Brexit discussions (if indeed there are any just at the moment) will do anything to prevent the clock just ticking down toward the March 29th Brexit date.

No word here on when or whether PM May will be back before parliament with another attempt to get her Withdrawal Agreement passed – at the moment there is nothing new with respect to the Irish backstop to vote on – or whether her offer to discuss the Labour opposition proposal for the UK to remain within a Customs Union will do anything other than alienate some members of her own party, including in the Cabinet.

On Sino-US trade, the one positive development that we first heard courtesy of Axios during our morning yesterday was that Presidents Trump and Xi could meet in Trump’s Florida resort of Mar a Lago in mid-March. US officials have suggested that the absence of a meeting before 1st March is because of logistics (Trump going to Vietnam to meet Kim, etc.) and say that the two could talk by phone this month. We also had White House spokesman Kellyanne Conway out saying it’s likely the US and China will make a trade

In FX, every G10 currency is weaker against the USD, pushing the DXY index up to 97.1, its first time above 97 this year. Of the DXY components, GBP is the biggest loser, -0.64%, after a pretty dire set of UK economic statistics, including weaker than expected Q4 GDP (0.2%), a sharper 0.4% drop in monthly (December) GDP with industrial and manufacturing production down by 0.5% and 0.7% respectively. None of this is being put down to Brexit uncertainty directly, though the FT’s lead story at the moment is about a raft of US companies warnings about the disruptive/negative impact on their business from a hard Brexit.

The Euro is 0.42% weaker, so in itself account for just over half of the 0.44% rise in the DXY. Nothing really new to report here, though some note to be taken of the possibility of Spain’s PM Sanchez being forced to take his country back to the polls in April (failure to so far win the support of Catalan parties for his budget is one of the key issues here).

The AUD’s efforts to claw back onto a 0.71 handle during our time zone yesterday proved fleeting , AUD/USD down to a low of 0.7057 overnight (no ‘new news’, just USD strength really) to its lows levels since January 4th when it was still recovering from the January 3 ‘flash crash’. NAB business survey this morning very important for RBA rate cut expectations and with that the currency.

US equities aren’t showing much of a pulse an hour before the close, within nothing notable in any of the S&P sub-sectors (Communication Services are +0.7%, Industrials +0.4% and Health Care -0.3%, but not much else changed with the overall S&P500 currently flat. This follows a generally positive day for European stocks (+/-1%) and a good day for Shanghai upon its return from last week’s Lunar New year holidays (+1.8%).

US bond yields are higher across the curve, 2 and 10 year Treasures up a little over 2bps having been closed during our day yesterday due to the Tokyo holiday. Local bond futures have largely followed suit.

Commodity markets are in a sea (albeit more pink than crimson) with oil off 40-60 cents, Dr.Copper off 1%. Iron ore futures, which re-opened on the Dalian exchange limit up yesterday, have eased back slightly in the night session (-0.7%) while other futures exchanges are showing losses of just over 1%. Gold is $5 lower.

UK Q4 GDP 0.2% (0.3%E, 0.6%P)

UK Dec GDP -0.4%

UK Dec Industrial Production -0.5% (0.1%E)

UK Dec Manufacturing Production -0.7% (0.2%E)

NAB AU January Business Survey (Conditions last 2.2 from 10.6; Confidence last 2.8 from 3.4)

AU Dec Home Loans (-2.0%E, -0.9%P)

US NFIB Small Business Optimism (103.0E, 104.4P)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.