Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Dirty trade talk rattles the markets.

https://soundcloud.com/user-291029717/trade-war-talk-makes-dollar-yuan-worse-for-trump

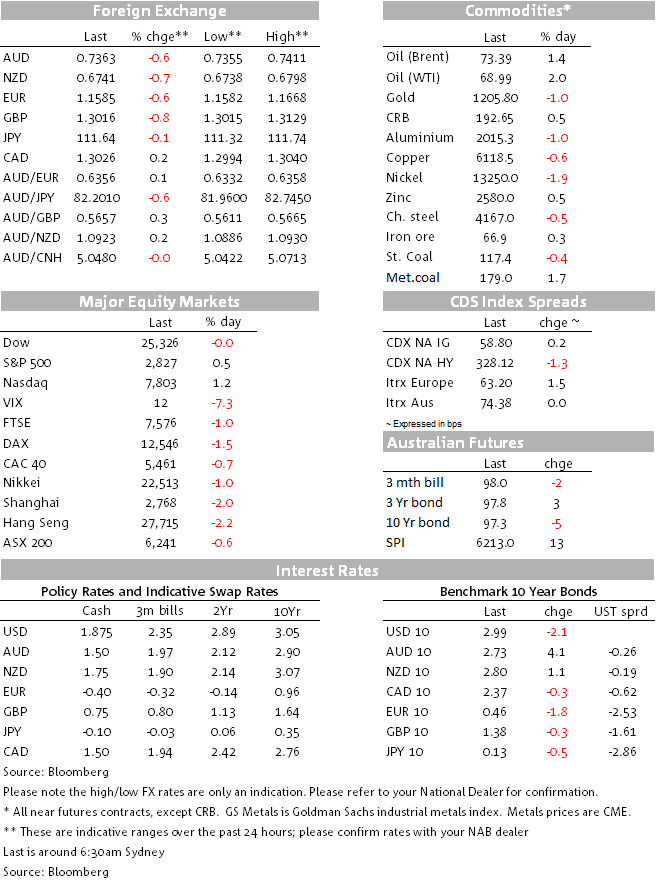

Yesterday’s official confirmation that President Trump had instructed the USTR to consider a higher 25% tariff (from 10%) on the proposed $200bn of Chinese goods triggered an angry response from China, a sell-off in Asian equities and a weaker CNY. European equities also closed in the red, but a bounce in IT shares led by gains Apple boosted US equities. CNY weakness weighed on AUD and NZD and GBP underperformed in spite of a hike by the BoE.

After yesterday’s NY close, Washington confirmed earlier news reports that the administration wanted to increase the proposed tariff on $200 billion of Chinese goods to 25% from 10%, stepping up pressure on Beijing to change its trade practices. Politico reported the higher tariff proposal is due to the depreciation of the Chinese currency offsetting the proposed 10% rate (CNY -8% over the past month). There was no clarification on the $16bn of tariffs that could be announced anytime from now.

Late yesterday, China’s Ministry of Commerce said that “China is fully prepared and will have to retaliate to defend the nation’s dignity and the interests of the people, defend free trade and the multilateral system, and defend the common interests of all countries”.

Reaction to the step up in negative trade rhetoric was firstly evident in the equity market with Chinese indices leading the decline. The Shanghai Composite closed 2% lower, after being down more than 3% at one stage. Europe was unable to arrest the negative lead from Asia and after a sharp decline at the open, US equities closed higher on the day, boosted by gains in IT shares. Apple shares led the rebound and in the process it became the first US company with a valuation of $1trn.

CNY was relatively stable at the start of yesterday’s Asian session, but at the European open after China’s response to higher US trade tariffs threats, it seems that some interpreted the “fully prepared” comment from China as a signal that authorities are willing to allow the currency to depreciate further and not get in the way of market forces. CNY and CNH came under steady pressure over the remainder of the overnight session, closing the day at 6.842 and 6.88.

Softer equities and weaker CNY dragged the AUD and NZD lower with both antipodean currencies losing about 0.55% against the USD. AUD now trades at 0.7360, with the early July low of 0.7311 now a little bit too close for comfort. Meanwhile the move up 68c proved short lived for the kiwi with the pair now trading at 0.6739. As we type the AUD/NZD cross has come under pressure dropping 25pips to 1.09 and probably reflecting the market’s perception of AUD’s higher sensitivity to China’s fortunes.

GBP is a notable underperformer despite the fact that BoE officials unanimously voted to lift the Official cash rate by 25bps to 0.75%. The move was widely expected, but there was some expectations for a couple of dissenters. GBP initially spiked +0.4% to 1.3125 on the no dissents headline, but quickly reversed the initial move trading to an overnight low of 1.3016, one bps lower where it currently sits. One explanation of the GBP moves would be that the market interpreted the BoE decision as a dovish hike, another however could be that the market believes the Bank is heading towards a policy mistake amid heightened Brexit uncertainty.

A stronger USD backdrop sees EUR sub 1.16 and from technical perspective the gap lower to 1.1587 now means the pair has pierced through its narrowing triangle evident since late May. USD/JPY is essentially unchanged at ¥111.66 with the key support at around ¥111.40 still resilient, in spite of the increase in US led trade tensions.

In the bond market, Japan conducted an unscheduled bond buying operation after the 10-year yield reached as high as 0.145%. This signals that whilst the BoJ ultimately has an upward limit of 0.20%, it is not prepared to see the market jump to that level so quickly, creating more of a two-way market in the short-term. Italy has returned to the spotlight, with its 10-year rate up 12bps to 2.90% on nervousness ahead of Budget talks. US 10-year Treasuries haven’t pushed on through the 3% and have retreated a little to sit down slightly to 2.98%.

It has been another mixed night for commodities with oil prices up between 1.5% and 2% while on the other end copper and metal prices are down around 0.70%.

AU: Trade balance ($m), Jun: 1873 vs. 900 exp.

UK: Markit construction PMI, Jul: 55.8 vs. 52.8 exp.

UK: Bank of Eng. bank rate (%), Aug: 0.75 vs. 0.75 exp.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.