Online retail sales growth slowed in May following a fairly strong April

Insight

Fed pricing has shot back up following Payrolls and the ISM to almost fully pricing a 25bps March hike and then a follow up May hike (there is now 40bps priced across the two meetings, up from 30bps the day prior).

“Ricochet, you take your aim; Fire away, fire away; You shoot me down, but I won’t fall; I am titanium”, Titanium, David Guetta/Sia Furler, 2011

“A wow number” is what the Fed’s Daly called the monster payrolls report on Friday. It is hard to disagree with headline payrolls at 517k vs. 188k expected, and the unemployment rate falling a tenth to 3.4% vs. an expected rise to 3.6%. That was then followed by a stunning ISM Services (55.2 vs. 50.5 expected; 49.2 prior) which has the markets questioning the Fed is almost done narrative. The worry of course is that the much better than expected data is bad news if the Fed sees this as bolstering its case of two more hikes and keeping rates elevated for longer. The WSJ’s Fed Whisperer opined this likely sees the Fed hiking by 25bps in March and signalling another hike at the following meeting, while officials are also likely to debate whether the current dot plot is enough to bring inflation back to target. All eyes on Fed Chair Powell on Tuesday who is speaking in conversation in what is a quiet week for data. The RBA also meets on Tuesday and is expected to hike by 25bps (more below).

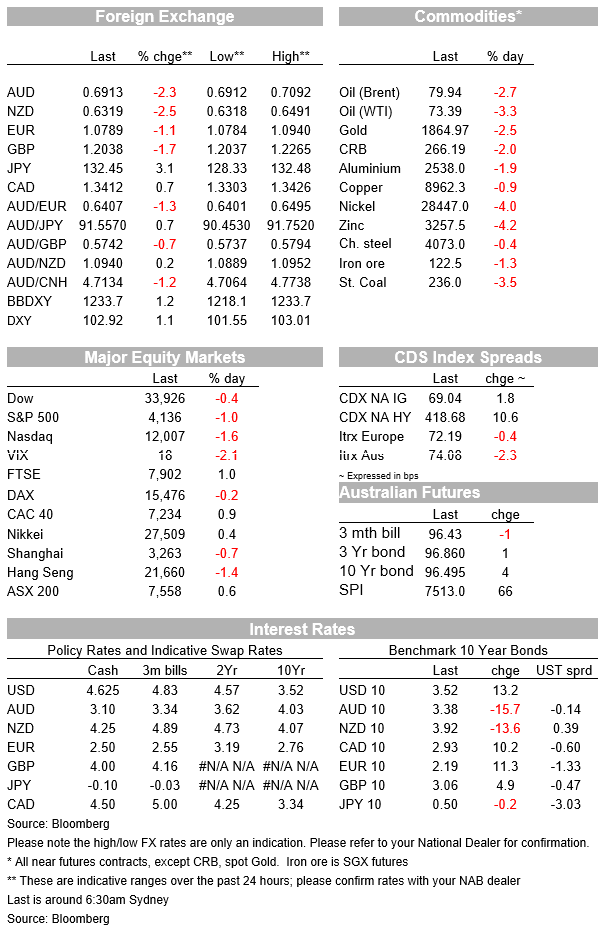

Fed pricing has shot back up following Payrolls and the ISM to almost fully pricing a 25bps March hike and then a follow up May hike (there is now 40bps priced across the two meetings, up from 30bps the day prior) . The terminal fed funds rate is now priced at 5.00% from 4.90% previously, and pricing for cuts in H2 2023 has been pared slightly to -40bps from -50bps the day prior. Yields shot higher led by the short-end with the policy-sensitive 2yr up 19.6bps to 4.29%, and importantly is 7bps higher than it was prior to last week’s FOMC meeting. 10yr yields rose by 12.3bps to 3.52% and is also around 4bps higher than it was prior to last week’s FOMC; under the surface real yields reflected most of the move in nominals with the 10yr TIP yield up some 12bps to 1.29%, while the implied breakeven was little changed at 2.23%.

The USD followed the sharp move in yields with the DXY +1.3%, and is now 1.1% higher than last week’s FOMC. The AUD (-2.2% to 0.6923), NZD (-2.4% to 0.6331), and Yen (USD/JPY +2.1% to 131.19; and now is up another 0.9% on reports of the Amamiya being sounded out as the next BoJ Governor – see below) all weakened sharply, along with commodities (gold -2.5% to $1,865; brent oil -2.7% to $79.94). The EUR was -1.1% and GBP -1.7%. The tumble in oil is interesting and may suggest a weaker underbelly to global growth with US oil inventories increasing last week, while the China demand rebound has been slower to materialise. Equities meanwhile fell with the S&P500 -1.0%, though the reaction was much more muted than what the headline would suggest given futures just prior to payrolls were already -0.5% due to soft tech earnings post Thursday’s close. Indeed the S&P500 is still up 1.5% prior to last week’s FOMC meeting, while both yields and the USD are higher.

The questioning of the prevailing narrative of the US economy weakening and the Fed being close done to done may have some near-term USD implications. Payrolls data suggests the US Fed needs to do more, while the BoE and ECB in rhetoric seem closer to re-evaluating their policy stance despite both flagging another hike in March, and the BoC also recently explicitly stated it was going to pause. That narrative was given legs on Friday with BoE Chief Economist Pill giving much less hawkish remarks, stating that while “It is important we do enough to attain our objective to return inflation to within the 2% target”, “… it is also important that we guard against the possibility of doing too much. We need to keep that zen-like balance in our objective. We have to recognise that we have done a lot with monetary policy already”.

Meanwhile as we go to print the Nikkei Times reports the Japanese government has approached BoJ Deputy Governor Amamiya as a possible successor to Kuroda, whose term ends on April 8. Amamiya has been deeply involved with BoJ policies (incl. YCC) and is seen as a continuity candidate. In early trade USD/JPY is up another 0.9% to 132.36 following the 2.1% move on Friday (see Nikkei Times: Japan sounds out BOJ deputy Amamiya for central bank governor ). Amamiya’s appointment, the ratification of which should be a formality means that the late July BOJ meeting is likely the earliest at which we’ll see a change in The YCC policy, following the completion of the annual wage rounds and which will need to yield an average (whole economy) wage gain of around 3% (vs 2% last year). As such the pop higher in USD/JPY is unlikely to be the start of a renewed uptrend.

As for details on US Payrolls, it was undeniably strong. Headline Payrolls were 517k vs. 188k expected and the unemployment rate fell a tenth to 3.4% to its lowest in 54 years vs. 3.6% expected. There were also upward revisions to prior months as benchmarks were updated with the level of payrolls revised up by 813k. Importantly, average hourly earnings while matching the 0.3% m/m expectation, was revised higher, meaning wages growth is not moderating as quickly as previously thought (3m annualised now 4.6% compared to 4.1% prior). The WSJ’s Fed Whisperer Timiraos post Friday’s close noted that “ Fresh signs of a hot U.S. labor market leave the Federal Reserve on course to raise interest rates by a quarter percentage point at its meeting next month and to signal another increase is likely after that” (see WSJ: Booming Job Gains Could Fuel Fed Debate Over Whether More Is Needed to Corral Inflation). Also debated will be if the 5.25% upper band terminal rate as given in the December dot plot is enough.

The Fed’s Daly was the first out of the blocks to comment on the report, noting “…the jobs report was a wow number, but the trend was not surprising…” and that the Fed’s December forecasts, which showed a median estimate of about 5.1% at the end of 2023, was “a good indicator of where policy is at least headed” and that “I’m prepared to do more than that, if more is needed”. “Right now the most important thing to convey to listeners is that the direction for policy is for additional tightening and holding that restrictive stance for some time”. (see Daly: Federal Reserve Bank of San Francisco president reveals ‘direction of policy’). Fed Chair Powell is due to speak in conversation on Tuesday and all focus will be on to what degree he pushes back on market pricing for cuts in H2 2023, and whether he walks back his FOMC press conference remark that “Financial conditions didn’t really change much from the December meeting to now. They mostly went sideways or up and down but came out in roughly the same place”.

ISM Services did little to dissuade from the view of the Fed needing to do more. The Headline ISM Services rose to 55.2 from 49.2, against 50.2 expected. Increases were seen across most components with a particularly sharp rise in new orders (60.4 from 45.2) and business activity (60.4 from 53.5), though employment was flat (50.0 from 49.4). The prices paid index also remained elevated at 67.8. There remains a wide divergence between what the ISM Services at 55.2 is implying for the economy, and the rival S&P Global Services PMI which is in contraction territory at 46.8. It is hard to square the divergence. One anecdote from a firm surveyed by the ISM was that “ Modest increase in sales activity following the holiday slowdown. Still seeing warning signs of a national/international recession. Higher interest rates having an impact. Outlook for the first quarter of 2023 is still projected lower than the same period in 2022” (see Services ISM Report on Business and the S&P Global US Services PMI for details)

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.