Online retail sales growth slowed in May following a fairly strong April

Insight

Friday saw quite a shocking miss on US non-farm payrolls.

https://soundcloud.com/user-291029717/nab-forecasts-two-rate-cuts-powell-on-primetime

Friday saw a quite a quite shocking miss on US non-farm payrolls of just +20k, but the number needed to be seen in context of an exceptional January print (revised up to 311k) and weather-related hits to the likes of the construction sector (e.g. the Household Survey, from which the unemployment rate is calculated not non-farm payrolls, reported that the number of non-farm workers unable to work because of the weather was some 160k above the average of the last 10 Februarys).

We should also note that at 186k, the 3-month average is still more than enough to keep downward pressure on the unemployment rate. Indeed, this fell by 0.2% to 3.8% so back close to the cycle low of 3.7% witnessed in Q4 2018. Equally, or perhaps even more significant, average hourly earnings rose by 0.4% (0.3% expected) too see annual growth lift to 3.4% from 3.2%. This compared to the 2018 increase of 3% and 2.6% in 2017. The Phillips Curve may be much flatter these days, but it’s not completely flat, at least judging from these numbers.

The – as yet unanswered – question for the Fed here is whether higher wages will translate into higher prices (or will it just result in lower margins?) and if it does, will the Fed resume tightening later this year or next? Fed chair Jay Powell gave a speech on Friday which reiterated the ‘patient’ and ‘wait and see’ mantra than now characterises almost all Fed-speak. But he also indicated that there was a high bar’ to adopting a new policy framework that seeks to embrace so called ‘make-up’ strategies that compensate for periods of sub-target inflation by aiming to achieve above-target inflation for a while such that the target is met on average over time. Such a policy might work in theory, but there is as yet no example in the real world of it working in practise, Powell noted. Expect ‘evolution not revolution’ was his conclusion.

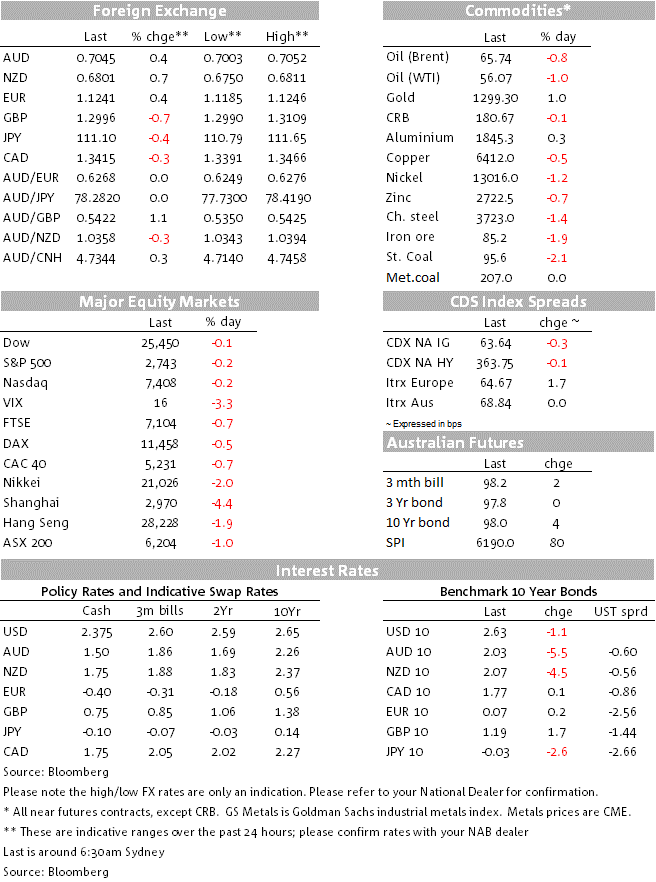

US stock markets didn’t like the payrolls miss (or perhaps it was, as per the foregoing, also the strong earnings number and so concern that that slower growth/stronger wages combo will be bad for margins?). The S&P fell over 0.8% at the open, extending the earlier fall in the futures index, but then proceeded to eke out gains during the NY afternoon to close down just 0.2% down. Energy was by far the worst performing sector (-1.95%) after Norway’s Sovereign Wealth Fund announced that it was planning to disinvest from upstart (i.e. exploration-centric) oil and other fossil fuel companies.

SPI futures fell by 14 points or 0.22% so we should dee the ASX opening lower this morning

US bond markets didn’t do too much with the employment report (the Powell speech was after Friday’s close) with Treasury yields about 1bps lower on average (10s ending at 2.628%)

In FX, the data also took the edge off the US dollar’s post-ECB rally from Thursday that had seen the DXY index revisit its Q4 2018 highs (97.7). From 97.5 pre-payrolls, DXY sipped to 97.3 post the data and held the loss though the NY day.

Most G10 currencies firmer against the softer USD led by NZD (+0.74%) and AUD (+0.41% to 0.7039 after a low of 0.7004 in late Sydney trade and following Friday’s China much worse than expected February trade numbers (but which weren’t quite so bad when looked at over January-February and bearing in mind Lunar New Year distortions).

EUR/USD pulled up to 1.1230 (+0.37%). CAD was +0.3% post strong employment data, while GBP bucked the trend, down over 0.5% on fading hopes for UK PM May’s Withdrawal Agreement getting passed by parliament this Tuesday. It has also opened sharply lower this morning.

In Commodities, oil prices were 1% lower (Brent) and -0.8% (WTI) with the Norway news seemingly playing more to the ‘peak oil demand’ view than concerns about reduced future supply from less investment in oil exploration.

Base metals, iron ore and steel futures were all lower with the exception of aluminium, as too was steaming coal (-2%).

CH: Exports ($, y/y%), Feb: -20.7 vs. -5 exp.

CH: Imports ($, y/y%), Feb: -5.2 vs. -0.6 exp.

US: Building permits (k), Jan: 1345 vs. 1287 exp.

US: Housing starts (k), Jan: 1230 vs. 1195 exp.

US: Change in non-farm payrolls (k), Feb: 20 vs. 180 exp.

US: Unemployment rate, Feb: 3.8 vs. 3.9 exp.

US: Average hourly earnings (y/y%), Feb: 3.4 vs. 3.4 exp.

CA: Net change in employment (k), Feb: 55.9 vs. 1.2 exp.

CA: Unemployment rate, Feb: 5.8 vs. 5.8 exp.

CH: Aggregate financing (CNY bn), Feb: 703 vs. 1300 exp.

CH: M2 money supply (y/y%), Feb: 8 vs. 8.4 exp.

CH: New Yuan loans (CNY bn), Feb: 885 vs. 950 exp.

Locally, the NAB Business Survey tomorrow will attract much scrutiny, also Westpac’s Consumer Confidence survey on Wednesday.

Today, in a couple of hours in fact (11:00AEDT) Fed chair Jay Powell will be featured on CBS’s ‘60 Minutes’

US Retail Sales is the data highlight tonight, expected flat in headline terms but +0.6% for the ‘Control’ reading that fees the consumption component of GDP

German industrial production and trade due in Europe; after Friday’s unexpected fall in orders, production is unlikely to match the 0.5% consensus forecast logged prior to the orders numbers.

A big week for Brexit with a series of votes in parliament starting with Tuesday’s second attempt by UK PM May’s to get her Withdrawal Agreement approved. This seems highly unlikely, leading to further votes in the week on whether to accept a hard Brexit at the end of the month (even more unlikely) then one to approve an extension of Article 50 (the likely outcome, the question for markets and all things GBP then being – for how long?)

Also of interest, China activity readings for February are on Thursday. President Trump will be unveiling his 2020 Budget, which press reports indicate will include the $8.6bn of funding to get on with the ‘wall’, so far denied him by Congress. Progress or otherwise on a Sino-US trade deal will also be important, amid reports that a Xi-Trump meeting to ink a deal might not now take place as early as late March. Trump adviser Larry Kudlow has though been out over the weekend saying progress is continuing to be made.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.