On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

As Americans head out to the polls the markets are left guessing whether it’ll be a good or bad result for President Trump.

https://soundcloud.com/user-291029717/the-waiting-game-1

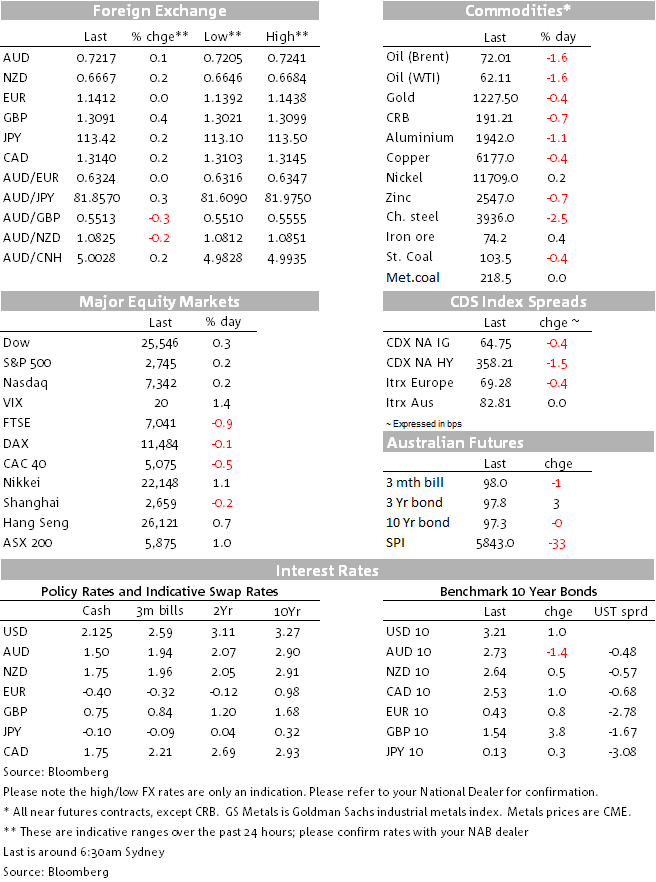

Market predictably quite with voting in the US mid-terms still underway (first polls close at 9am AEDT). In FX GBP (up) and CAD (down) showing some life with AUD and NZD both a little firmer. US stocks showing small gains into the close, oil lower again and US bond yields a smidge higher.

It seems we’ve now graduated from an obsession with President Trump’s Twitter feed to interpreting the hand signals coming out of 10 Downing Street as a source of inspiration for market volatility. Thus a ‘thumbs up’ from UK Brexit secretary Dominic Raab out of a Cabinet meeting yesterday saw Sterling immediately jump to its best levels in two weeks. This was on the view that progress is being made towards a UK Brexit position with regards to the Irish backstop that could suffice to have EU Brexit Commissioner Michel Barnier being prepared to call an EU Summit for later this month. According to the Guardian newspaper, “Cabinet sources saying that ministers, led by Geoffrey Cox and Dominic Raab, are now working up a mechanism to review the backstop which will make sure that it won’t go on forever.” A little later in the day, Barnier himself was quoted saying that without an operation backstop, there is no deal and so no transition period, but that “if we can get a deal on a backstop and I see decisive progress, I will recommend a (November) Summit”.

In the last hour, the BBC has reported that on November 19th the Withdrawal Agreement and future framework will be put to parliament by way of a statement by Brexit minister Raab, citing a Brexit document it has been but which a government spokesman has just said “does not represent the government’s thinking”.

So all to play for still, but with the smoke surrounding a possible Brexit deal thickening, the trading market looks justified in taking the view there must be a fire somewhere, bearing in mind that there is easily another 5-6 cents of upside for the GBP/USD rate on confirmation a deal (and which would put AUD/GBP easily down through its recent lows of around 0.5340).

On the negative side of the European ledger overnight are signs Italy’s coalition may be fraying. The populist government called a parliamentary vote of confidence amid internecine tensions over immigration and spending priorities, Bloomberg reports. Deputy PM and League head Matteo Salvini is pushing for restrictions on the rights of asylum-seekers, opposed by some Five Star senators who risk expulsion from the party if they vote against the administration. 10 year Italian government bonds are 7bp higher while EUR/USD sits little changed on this time yesterday, unable to benefit in the slipstream of the stronger Pound, as has been the case of late.

One other development to note overnight is further slippage in oil, with Both Brent and WTI crudes off close to $1. This is allegedly on reports that Iraq plans to boost its output and capacity in 2019; this comes on top of realisation that a lot of Iranian oil is going to continue to flow as a result of the sanctions waivers granted to eight countries by the US (as well as Russia’s declared intent to help Iran circumvent oil export restrictions).

The relevance of this for currencies is that the Canadian dollar continue to suffer much more than the Aussie dollar on lower oil even though it represents a negative terms of trade shock for both of them. CAD is the worse performing G10 currency overnight and AUD/CAD has just exceeded its previous (Sep 26th) high overnight, hitting 0.95 to now sit very close to its 100 day moving average. With the AUD speculative market still collectively sitting short it seems, but not CAD, there looks to be scope for more gain in the absence of a quick oil price turnaround.

AUD gains in the last 24 hours to a high of 0.7241 (~0.7220 now) has been eclipsed by NZD as well as GBP, but owes something to yesterday’s post-RBA meeting statement where the Board flagged small upgrades to its growth and inflation forecasts and ¼% downward revision to its 2020 unemployment rate forecast (to 4.75%) in Friday’s Statement on Monetary Policy.

US bond yields are just under 1bp higher at 10 years and the more Fed policy sensitive 2-year note yield up 1.6bps to a new cycle high of 2.925%. 10 years yields are back from their intra-day highs after a good 10-year note auction, while of some note US break-even inflation rates have risen by 1bps or so despite the further decline in oil prices (meaning real yields have actually eased back a touch). As mentioned above, 10 year Italian bonds (BTPs) are 7bp higher while German 10 year bonds closed 0.8bp up. On Italy, PM Conte is now out saying that pension reform and citizen’s income will commence early in 2019 – that might not play too well later today.

Into the close, the S&P 500 is up about 0.14% with industrials and materials leading with gains of +/-1% and communications the one sub-sector in the red but only just. The NASDAQ is finishing 0.3% up and the Dow about 0.4%

Platinum and wheat are the only two commodities across the entire spectrum of energy, base and precious metals, and agri. to be showing green on my screen at the moment, with oil extending loses into the NY close (Brent -$1.15, WTI -$1.0). Aluminium is the biggest faller among the base metals (-1.25%) while iron ore futures are almost matching (-1.2%). In agri., last night dairy auction saw the GDT Index clearance price down 2%. So prices continue to track lower, broadly in line with expectations on the day. The GDT Price Index is 12.3% below a year ago. Price declines this season have been orderly but persistent.

German manufacturing order rose by 0.3% in September against expectations for a 0.5% fall, so some signs that the impact of retooling in the auto sector may be completing, though orders are still 2.2% down on a year ago.

Eurozone final services PMI printed 53.7 against a preliminary 53.3.

US Jolts job openings for Sep eased to 7009mn (saar) from a revised 7136, but not surprising in this volatile series and given the surge so far this year. Hiring’s also eased to5744 from 5906 (by more than openings, thus extending potential wage rises). The quit rate also eased slightly

US mid-terms elections are in train with first polls closing at 6pm ET in Kentucky and Indiana (9am AEDT); TV networks may begin to make projections soon thereafter. About 20 large states will see their polls close at 8pm ET (11:00 am AEDT) and results will be flooding in, so we get a reasonable idea of how the balance of power in the House is shifting after this and also whether confidence in the Republicans retaining control of the Senate is looking justified.

8:45 AEDT see NZ publish the September quarter labour market statistics. Our BNZ colleagues believe these will be robust, at heart, though with a risk that some of it may look a bit disappointing on technical grounds. Base case, however, is for the unemployment rate to nudge down to 4.4% for Q3, whereas the August MPS anticipated it to be unchanged at 4.5%. Annual employment growth, as per the Household Labour Force Survey, is seen at 2.0%, close to the RBNZ’s forecast of 2.1%. BNZ are exactly in line with the RBNZ, however, in picking the annual pace in the private Labour Cost Index to decelerate to 1.9%, from 2.1% in Q2. This is as the big “care-worker” impact on Q3 2017 drops out of the annual calculation, and a 0.5% gain comes in for Q3 2018.

The European session will see German industrial production, following last night’s 0.3% rise in factory orders.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.