Online retail sales growth slowed in May following a fairly strong April

Insight

The UK Prime Minister will table her Withdrawal Agreement again tonight.

https://soundcloud.com/user-291029717/brexit-date-determined-today-us-china-trade-talks-could-take-months

With the exception of more (downward) volatility in all things GBP, not a whole lot has happened in global markets since we left of yesterday. No currency other than Sterling is more than a quarter percent away from where it was at Wednesday’s NY close, US bond yields have retraced a couple of basis points of their mid-week swoon (but with 10s still sitting below 2.40%) and all US equity indices have just closed about a third of a percent higher.

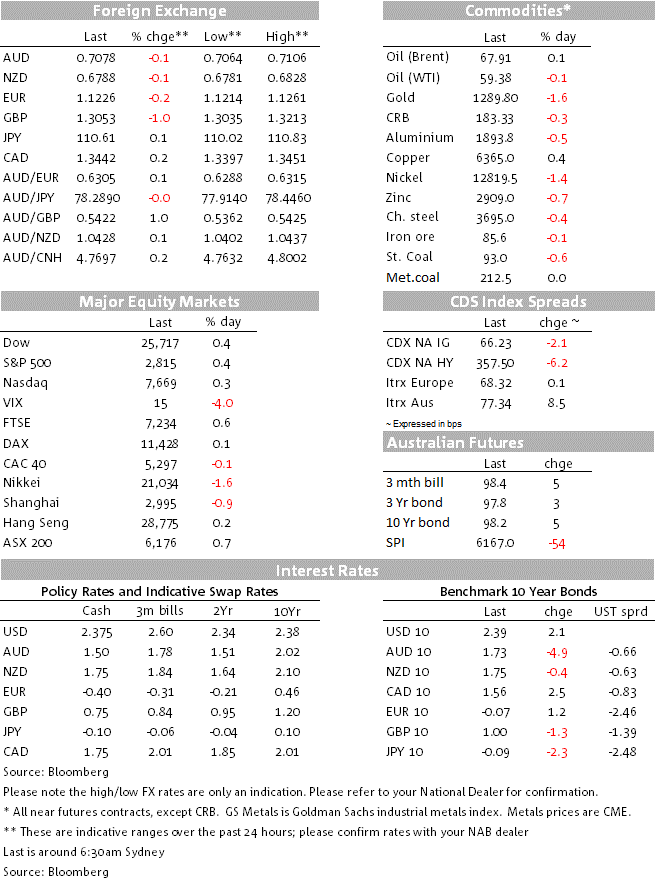

So in FX, GBP/USD is about a cent and a half down on where it was at the Sydney close, with the London market reacting for the first time to the news that greeted us yesterday morning, namely that all eight of the possible ways forward out of the Brexit morass had been voted down in the so called indicative votes process.

Meanwhile embattled Prime Minister Theresa May is about to test the adage – nonsensical of course – that a drowning man, or in this case woman, goes down three times. She is reportedly bringing her withdrawal agreement back to the floor of the House tonight, without the associated political declaration regarding the Irish backstop. It seems almost certain to be defeated (The DUP having re-iterated publicly that they won’t support it). The latest Brexit irony here, as noted yesterday by Bloomberg (nee the FT’s) gun columnist John Auther’s, is that Mrs. May needs to succeed in getting her deal approved in order to lose her job, but might get to keep it for a lot longer is she fails.

With failure all but assured tonight, we are then looking at further indicative votes next week to see whether a majority can be achieved for at least one way forward. Here, we’d note that yesterday’s vote on the UK remaining in the EU Customs Union failed by just 6 votes (revised from 8 in the originally reported count). With UK cabinet ministers having been whipped to abstain, there must be a chance that assuming May’s deal gets rejected tonight, this option could get up next week. If so it would provide the basis for the UK going back to Brussels to request a longer extension of Article 50. The proviso here of course is that at the same time the UK accepts it will take part in EU elections due May 23-26th. Under such a scenario, we’d see scope for a full retracement of the losses in GBP since March 13th, when cable was nudging $1.34.

The only other G10 FX mover has been CAD, down just under 1/4% and where President Trump’s latest Twitter-feed attack on OPEC+ demanding they pump more oil looks to have been responsible, though spot oil prices have now fully recovered from the $1+ drop suffered immediately following Trump’s tweet. It may just be a function of creeping USD appreciation, even if we ex-out the mechanical impact on USD indices from Sterling’s fall. DXY is up 0.5% to 97.24, so to within half a percent of its December 2018 and early-March cycle highs.

AUD sits just below 0.7080 from just above 0.7100 at Thursday’s Sydney close, with nothing to report beyond creeping USD strength here. Next week promises to be interesting with the RBA on Tuesday (oh and the Budget, if anyone in FX land really cares?)

Fed speak overnight has included influential Fed Vice Chair Richard Clarida, who highlighted that the US was more exposed to shocks from abroad than it has been in the past and, as such, the Fed was conscious of downside risks stemming from Brexit, a deeper downturn in the global economy and trade tensions. In a dovish nod, Clarida noted that policy adjustments by the Fed had helped cushion the impact on the US economy from previous global shocks, including the European sovereign crisis and the Chinese capital flight episode in 2015/16, with the inference being that the Fed might be willing to cut rates if these global risks were realized. There was little reaction to the speech however, with the market already pricing two full rate cuts from the Fed by the middle of 2020.

NY Fed president John Williams has also been speaking, saying the Fed would rethink its (patient) policy path if the data showed the Fed to be missing its goals, but qualifies this by saying that it is currently pretty close on both sides of its dual mandate.

On economic data, Q4 US GDP was revised lower to 2.2%, slightly below expectations, while perhaps more significant, jobless claims were lower than expected at 211k with the prior week revised down to 216k from 221k; In fact, a the result of annual revisions to seasonal adjustment factors, the trend in jobless claims is now flat, not rising as original data showed, with the four week average down to its lowest level since November. So we have a picture of continued labour market strength juxtaposed against clear evidence of slower growth either side of year end. Sound familiar?

In Europe meanwhile, business confidence fell to its lowest levels since 2016, led by the manufacturing sector, while German CPI was lower than expected at 1.4% on an EU harmonized basis, down from 1.7% in February and 1.6% expected.

On the trade front, White House economic advisor Larry Kudlow noted in a speech that an agreement with China “was policy, not time-dependent”, raising the prospect that it could be some time before the two sides can iron out their differences. Kudlow added that “if it takes a few more weeks, or if it takes months, so be it.” US Treasury Secretary Mnuchin and US Trade Representative Lighthizer will have trade talks in Beijing today and then next week Chinese vice Premier Liu will travel to Washington, with his schedule to include a meeting with Trump.

EC: Economic confidence, Mar: 105.5 vs. 105.9 exp.

GE: CPI (y/y%), Mar: 1.5 vs. 1.6 exp.

US: GDP (q/q% annualised), Q4: 2.2 vs. 2.3 exp.

US: Pending home sales (m/m%), Feb: -1 vs. -0.5 exp.

RBNZ’s governor Orr is speaking as we hit the send button but nothing market moving in the speech. Q&A is due

ANZ NZ Consumer confidence at 08:00 AEDT

Japan Tokyo CPI, industrial production, retail sales

Offshore tonight, the US core PCE deflator looks like the standout in what is a very unexciting calendar. We look for an on-consensus 0.2% print.

Also due is the Chicago PMI, New Home Sales, and the final UoM March consumer sentiment reading

Canada has monthly GDP for January, and in Europe German retail sales

ECB’s Coeure and the Fed’s Kaplan are among the anointed speakers.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.