On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Market pricing for ECB meetings increased, helping European yields higher across the curve.

“I got a letter this morning, Postmark said it was from Spain” – Electric Light Orchestra

A more cautious tone across markets starts the new week. Central Banks, key data, and earnings all loom large this week, though the news flow over the last 24 hours has been comparatively quiet. US equities are lower, with the S&P500 tracking around 1% lower. Yields are higher globally, led by Europe as stronger-than-expected Spanish inflation suggested stickier inflation and added to expectations for ECB hikes.

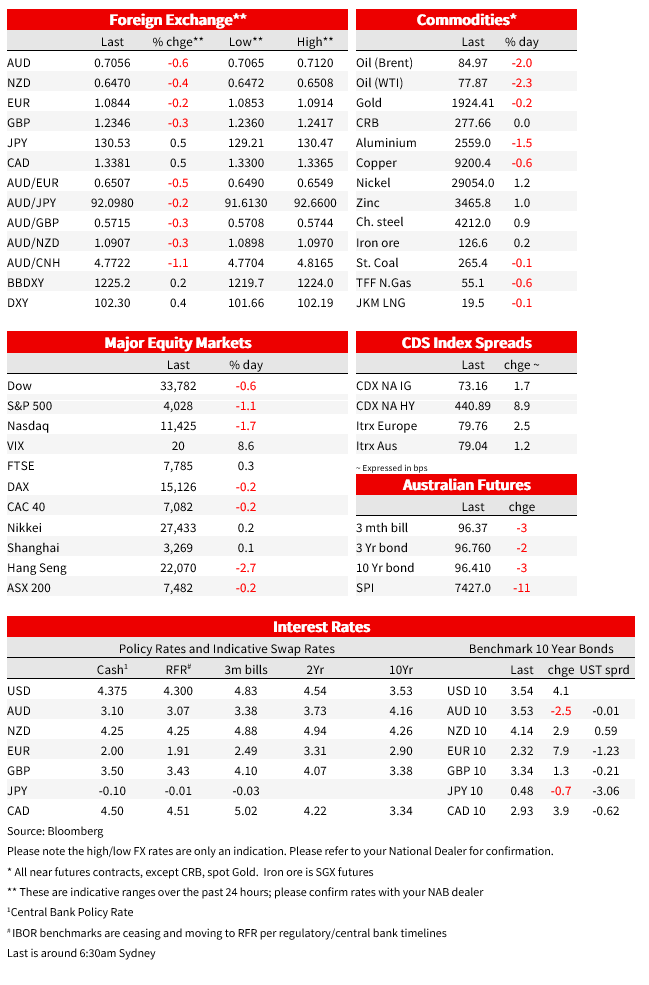

US Equities were lower on Monday. The S&P500 is trading around 1.1% lower led by declines in energy, IT, and Communication sectors. The NASDAQ was 1.7% lower. Those moves contrast strong gains last week when the S&P500 added 2.5% and the NASDAQ surged 4.3%. The cautious start to the new week is ahead of a packed earnings season calendar with more than 100 S&P500 companies reporting. Spotify and Snap report on Tuesday, ahead of Meta on Wednesday and Apple, Amazon and Alphabet on Thursday.

The key data overnight was Spanish inflation, which surprised sharply higher. Harmonized CPI was 5.8% higher y/y from 5.5% and sharply above the fall to 4.8% expected. The distribution of forecasts was unusually wide, with added uncertainty from a reweighting. The result was driven by a rebound in fuel costs and smaller discounts in start-of-year apparel sales, but the core measure rose to a record 7.5% y/y adding to fears of stickier price pressures even as headline reads are off their peaks. The surprise suggests upside risk the Eurozone numbers on Thursday just ahead of the ECB Meeting. Note German inflation data, including the state level readings, usually released ahead of the eurozone aggregate, has been postponed this month.

Market pricing for ECB meetings increased, helping European yields higher across the curve. Markets now price a July peak rate of 3.41%, from 3.32% on Friday, though the expectation for this week’s meeting remains firmly at 50bp, the uncertainty instead on the path forward after that. An immediate jump up in European bond yields after the report was sustained throughout the session, with Germany’s 2-year rate up 10bps and the 10-year rate up 8bps. The move spilled over into US Treasury yields with the 2-year yield 5bp higher and 10-year 4bp higher to 3.54%.

Contrasting the upside surprise to inflation was German GDP data , which fell 0.2% q/q on the flash estimate, revised lower from an earlier estimate implying flat growth. Euro area GDP is released today, with consensus for a 0.1% q/q decline and 1.7% y/y. A more forward looking read comes from the euro-area economic confidence index – a mix of business and consumer confidence – which lifted for the third consecutive month in January to 99.9, a seven-month high and above expectations. Industry, Services and Consumer confidence all rose, with consumer confidence now at its highest level in 11 months, though still at low levels.

In currency markets the USD was 0.4% higher on the DXY. Higher rates helped JPY to the weaker end of the leader board, with USD/JPY up 0.5% to 130.53, while the euro was the best performing of the G10 currencies, down 0.2% against the dollar. The AUD lost 0.6% against the dollar to 0.7056. Yesterday, a report from a panel of experts, including potential future BoJ deputy Governor Yuri Okina, proposed that the government and BoJ should revise the joint policy statement to make the inflation target a “long-term” goal. “The normalization of yield functions and the bond market would likely mean a need to comprehensively rethink monetary policy, including its various methods of conduct ” Okina said. Knee-jerk yen strength on publication of the report saw the USD/JPY down to a low of 129.20, but this wasn’t sustained. Speaking to Parliament, BoJ Governor Kuroda says that the Bank of Japan will maintain its 2% inflation target and continue monetary easing.

Chinese equity markets returned from the Lunar New Year Holidays to early gains , though the CSI 300 pared the bulk of those through the day to end just 0.5% higher. The index is just under 20% above its end-October low. The pace of the rebound in activity continues to be in focus, with one positive signal being that more than 300 million trips were made during the Lunar New Year holiday, nearly 90% of pre-pandemic levels, according to the Ministry of Culture and Tourism. January Official PMIs are released today.

Other news flow of some note includes reports that New York and much of the East Coast are at risk of a gasoline shortage this summer with seasonal stockpiles at their lowest levels in a out a decade ahead of the peak driving season and the EU ban on Russian oil-product imports beginning 5 February. On the inflation outlook, Nobel laureate Paul Krugman is worried “markets are getting ahead of themselves” and warns that markets pricing that inflation is over could be a ‘self-denying prophecy’ if easier financial conditions reignite price pressures. On a longer-term view, US Treasury Secretary Janet Yellen said persistently weak inflation is the more likely long-term challenge once we are through “unusual and difficult period.”

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.