Online retail sales growth slowed in May following a fairly strong April

Insight

Three pieces of news drove sentiment overnight.

https://soundcloud.com/user-291029717/eu-doldrums-uk-hope-and-chinas-complications

Your love alone is not enough not enough not enough – Manic Street Preachers

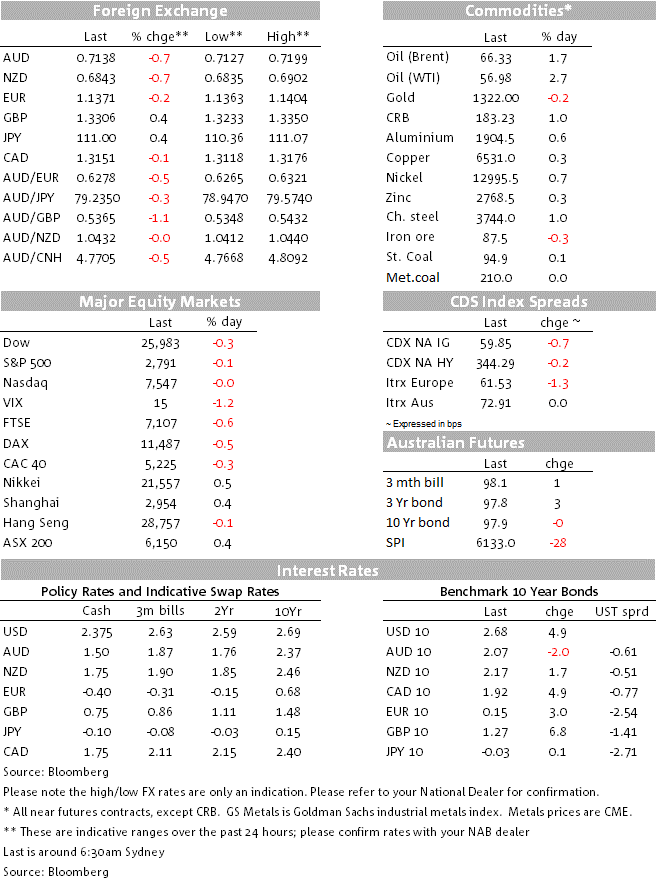

Risk assets remain in a cautious mood not helped by an escalation in tension between India and Pakistan while overnight US Trade Representative, Robert Lighthizer, tempered expectations of an imminent US-China trade deal following earlier suggestion by President Trump that a deal with his friend Xi was in the making. The USD is a tad higher with gains against AUD, NZD and JPY partially offset by a stronger pound and oil linked currencies (CAD and NOK). Oil prices jumped following an unexpected decline in US inventories, UST yields also head higher.

US equities have traded in an out of positive territory initially opening with a soft tone following a negative lead from Asia and Europe. The flare up in tensions between India and Pakistan triggered a bid for safe haven assets late in our session yesterday. Speaking before Congress, US Trade Representative Lighthizer delivered a more cautious message in terms US-China trade negotiations progress. In contrast to comments from President Tump, a few days ago where the President suggested an agreement could be signed late in March, Lighthizer sounded less optimistic noting that that “The issues on the table between the U.S. and China “are too serious to be resolved with promises of additional purchases,” and that it is still too early to tell if China will concede to US demands. Lighthizer also said that “This administration is pressing for significant structural changes that would allow for a more level playing field” adding that “Much still needs to be done, both before an agreement is reached, and more importantly, after it is reached.”.

In contrast to the soft/sideways moves in equities, global rates have moved higher overnight. Looking at the intraday charts the jump in both 10y Bunds and 10y UST yields appear to have been driven by technical factors aided by the move higher in oil prices while US corporate issuance and heavy selling of German bunds futures also seemingly played a role. After coming under some pressure following a tweet by President Trump asking Opec to “relax”, oil prices rebounded overnight following an unexpected drop in US crude-oil inventories (8.6m barrels decline to 445.9m vs expectations for a small increase) and comments from the energy minister of Saudi Arabia, reiterating OPEC’s commitment to cutting output to rebalance the market. 10y UST yields now trade at 2.6933%, up 6bps over the past 24hrs while 10y bunds closed 3bps at 0.148%.

The USD is a tad higher in index terms with DXY up 0.17% to 96.16% while BBDX is +0.18% to 1187.85. Gains in the USD vs majors have come from weakness in AUD, NZD and JPY. Yesterday the antipodean currencies traded softer amid weaker than expected domestic data releases, NZD took as small hit on worse than expected January trade figurers (-$914mn vs. -300m E), then AUD (to low of 0.7175 from high of 0.7199) on weaker than expected Construction Work Done. The latter suggest there is considerable downside risk to the RBA’s implied expectation of a relatively modest 0.9% q/q decline for private dwelling investment in Q4. Cautious risk mood overnight didn’t help the AUD and NZD either with both pair extending yesterday’s losses. AUD now trades at 0.7137% and NZD is at 0.6842.

Late yesterday, USD/JPY traded lower following news that Pakistani fighter jets shot down two Indian aircrafts and a soft opening by European equities didn’t help either. That said, given the high degree of sensitivity to 10y UST yields, courtesy of the BoJ’s yield curve control policy, USD/JPY is back above ¥111 as we type reacting to the solid jump in 10y UST yields to 2.69%.

The standout performer in FX markets is again the GBP, following on from Theresa May’s decision to allow the UK parliament the option of extending Article 50. The GBP is 0.4% higher to 1.3306, its highest level since July. This morning the UK Parliament voted against a motion put forward by the Opposition Labour party that urged the government to adopt a Customs Union deal and then move to a second referendum. This motion was expected to be defeated and pressure will now be on Corbyn to go full steam for a second referendum in coming days. That in turn will help pressure the Tory Brexiteers to take May’s deal on the 12/13th March or risk losing Brexit to a long extension or second referendum. Meanwhile, on the other side of the Channel, French President Emmanuel Macron said the EU would only grant the U.K. an extension to the Brexit negotiations if there is a “clear” reason for doing so, meanwhile in a more conciliatory tone German Chancellor Angela Merkel said “The exit deal applies. If the UK needs a little bit more time we will not say no but we want an orderly Brexit,”. Our position has long been the UK will not leave without a deal and while we expect GBP to make further gains, we also think a volatile GBP environment is likely as the political tension get worked out.

Having delivered his semi-annual testimony to the Senate yesterday, there was, unsurprisingly, little new information from Fed Chair Powell’s testimony to Congress overnight. Powell said the Fed was close to agreeing a plan on its balance sheet (which is shrinking, as the Fed lets is QE holdings mature). The consensus is for the Fed to halt its balance sheet reduction later this year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.