Online retail sales growth slowed in May following a fairly strong April

Insight

Today, a session that has been high on movement, even though it’s been low on data. And the Bank of Japan’s attempts to control bond yields has impacted bond prices across the globe.

https://soundcloud.com/user-291029717/faangs-bitten-bonds-hit-by-boj

Like Nelly Furtado’s hit Powerless (Say what you want), the rates markets has come under pressure over the past 24hrs with speculation over the BoJ policy decision today pushing core global yields higher. The USD is weaker across the board, the AUD has been a bystander and SEK the outperformer. US equities are weaker, led by further declines in the tech sector, as investors rotate out of this sector following some high-profile earnings misses

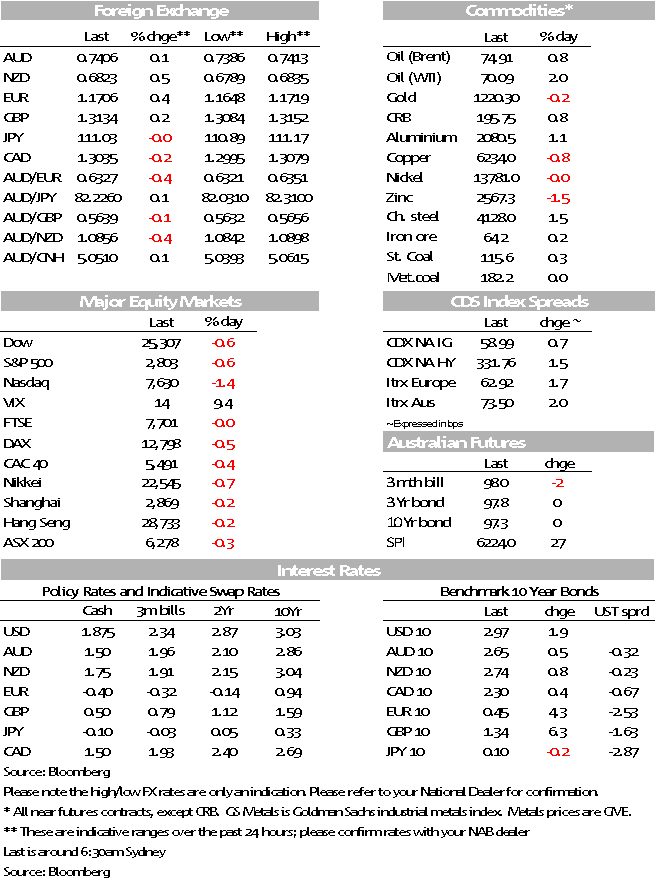

The USD has been the worst performing of the majors for no particular reason, with a steady grind lower since the European open. AUD is little changed currently trading at 0.7406 unable to materially benefit from a softer US. Meanwhile SEK is at the top of the leader board, up over 1% to 8.77, boosted by Sweden’s Q2 GDP of 1.0% q/q that smashed expectations of a 0.5%.

Against a soft USD, the yen has made little progress and USD/JPY sits close to 111, with some nervousness ahead of this afternoon’s BoJ policy announcement. The last week or so has seen reports that the BoJ may either review its yield curve control policy or tweak its operation, with the idea to improve the longevity of the stimulus programme and reduce the harm it causes to the profitability of commercial banks. It seems that the BoJ would be happier to see long term rates increase but it doesn’t want to see a concurrent appreciation of the yen. It’s a difficult balancing act and the central bank will need to get its messaging right.

Fears of higher JGB yields means fears of weaker Japanese demand for foreign bonds and this has seen global rates increase recently. Those moves extended overnight, with UK’s 10-year rate up 6bps to 1.34% and Germany’s 10 year rate up 4bps to 0.44%. That backdrop has seen US 10-year Treasuries nudge up 2bps to currently 2.975%, after reaching a fresh July high of 2.99% overnight. A slightly steeper curve is evident, with the 2-year rate flat.

The negative lead from Asia which saw the Shanghai Composite closed down at 0.16% extended into the European and US sessions with all major indices showing negative returns for the start of the week. The NASDAQ has once again led the decline as investors rotate out of IT shares following a string of disappointing earnings results. The NYSE FANG index is now down over 9% through the past three trading sessions.

It thas been a contrasting night for commodities, oil prices are up between 1% to 2 % driven by news that a key Canadian facility won’t return to full production as quickly as expected, adding to global supply concerns. Iron ore, gold and metals are little changed, but steam coal is the big loser, down 3.67%

US Commerce Secretary Ross indicated that trade negotiations with Mexico under its new President were proceeding rapidly and were close to completion. This follows US Trade Rep Lighthizer’s comments last week indicating some hope that NAFTA talks are in the “finishing stages”. It remains to be seen whether a bilateral deal with Mexico will be agreed before negotiating separately with Canada.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.