Long-term signal vs. Short-term noise

Insight

There were no major surprises in Friday’s US NFP report, unlike the prior days weekly jobless claims data.

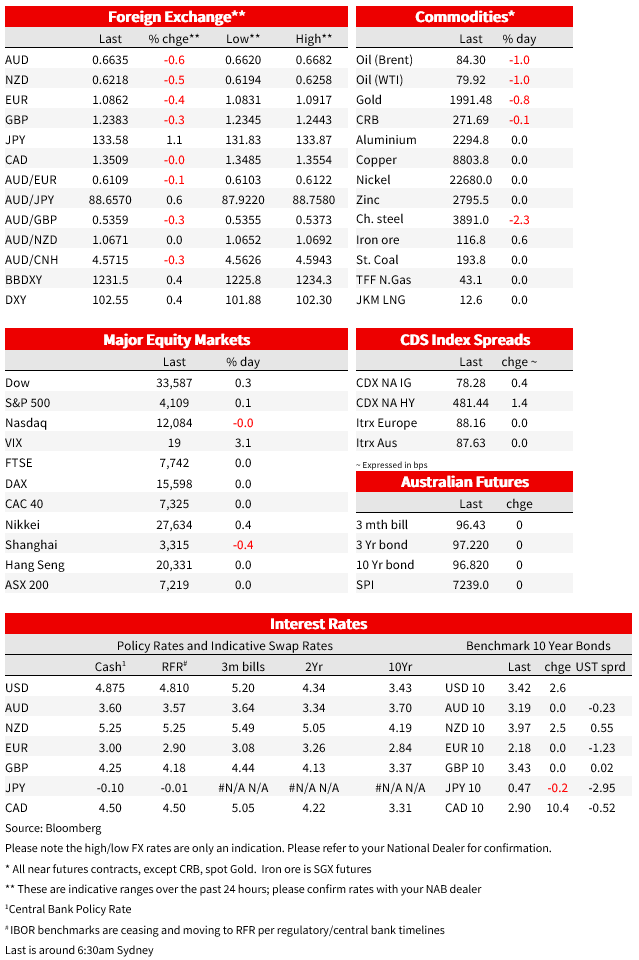

CA: Unemployment rate (%), Mar: 5.0% from 5.0% vs. 5.1 exp.

US: Jobless claims (k), wk to 1 Apr: 228 vs. 200 exp.

US: Change in nonfarm payrolls (k), Mar: 236 vs. 230 exp.

US: Unemployment rate (%), Mar: 3.5% from 3.6% vs. 3.6 exp.

US: Average hourly earnings (m/m%), Mar: 0.3 vs. 0.3 exp.

US: Average hourly earnings (y/y%), Mar: 4.2 from 4.6% vs. 4.3 exp.

In a truncated US bond market session on Friday, US Treasury yields jumped 15bps at 2-years and 8.5bps at 10 years, the US dollar rose modestly and the AUD was unchanged, still mired below 0.67. This was after the March US payrolls report revealed a 236k rise in non-farm payrolls with +17k of net revisions (230k expected). The unemployment rate fell 0.1% to 3.5% (3.6% expected) and average hourly earnings rose by an as-expected 0.3% to be 4.2% up on a year ago down from 4.6% and 4.3% expected.

Despite this evidence that wages growth is moving quite decisively in the ‘right’ direction from an inflation perspective US money market rates moved to ascribe a 70% probability to the Fed lifting the Funds rate by 0.25% to 5.0-5.25% on May 3, up from close to 50% pre-release. Monday’s US session has seen bond yields edge higher (2-3bps) with the 2-year note back at 4.0% while equities have closed little changed in NY. The USD has gains have extended Friday’s gains, particularly versus the JPY (USD/JPY up over 1%). AUD/USD is now back below 0.6650.

Arguably more revealing that the payrolls report, last Thursday night’s weekly jobless claims showed large-scale upward revisions following the annual benchmarking process of seasonal adjustment factors. Claims were 228k in the week ended 1 April from a prior week’s 246k that was originally reported as 198k. The revised data now shows claims above 220k since the beginning of March. Meanwhile the latest Challenger Gray & Christmas planned layoffs data recorded 89,703 in March, showing the February fall to be a blip on a rising trend that date back to last October (before which layoffs were running at sub-30k a month).

US economists we closely reckon Friday’s non-farm payrolls gain of 236k was the last 200k rise we’ll see in the cycle and could be negative within a couple of months. In this respect the NFIB’ (small business) hiring intentions reading also out late last week was a near 3-year now, while the ‘quit rate’ within the earlier JOLTS report is giving a strong signals that average earnings growth is heading down to a rate that the Fed will before too long deem consistent with its 2% inflation target.

Other data out since we broke up for Easter included a strong Canada jobs report, with employment up 34.7k against 5k expected and the unemployment rate steady at 5.0% rather than the consensus for a rise to 5.1%. Markets nevertheless continue to ascribe zero change to the Bank of Canada resuming raising rates following its pause when it meets this week. In Japan, yesterday, Japan’s consumer confidence readings were positive, Consumer confidence is up to 33.9 in March from 31.1 and the Eco Watchers ‘Current’ reading up to 53.3 from 52.0 and ‘Outlook’ to 54.1 from 50.8. But Friday’s hard Household and Consumer spending data told a different story, with consumer spending growth down to 2.6% y/y from 6.1% (albeit for February).

Incoming BoJ governor Ueda, speaking at a press conference Monday, says that its appropriate to continue with yield curve control, that the yield curve is smoother than before and that ‘big’ rate increases aren’t possible in Japan for now. He does note though that this year’s wage talks have been ‘good so far’ and that it’s entirely possible underlying inflation will reach the 2% BoJ goal. His remarks would appear to rule out any policy change at this month’s meeting, but we still contend the June and if not June then July meetings are ‘live’ for a change in YCC policy.

Bond markets have shown more volatility than equities since last Thursday’s close, with US 2-year yield up some 18bps (and 23bps since lst Wednesday’s close) and 10s up 11bps to 3.42%. US equities have closed out Monday’s US session with the indices narrowly mixed (S&P500 +0.1%, NASDAQ flat and the Dow +0.3%). In FX, the USD is stronger across the board since Thursday, with losses of +/- 0.5% for NZD, AUD, GBP, EUR and CHF, while USD/JPY is up 1.35% thanks to the combination of higher US Treasury yields and the above Ueda comments.

Finally, New York Fed President John Williams has just been speaking and says it’s important the Fed is able to take steps to lower prices (implicitly endorsing another hike in May) and that he’s not worried about market rates expectations (for cuts later this year) and that he doesn’t think rates hikes are behind the issues at failed banks. The Fed is though monitoring credit conditions in the wake of the turmoil and says it’s not clear how much credit conditions will tighten.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.