Online retail sales growth slowed to almost flat in March

Insight

Have the Fed clarified its position after an apparent U-turn at their last meeting?

https://soundcloud.com/user-291029717/fed-minutes-uk-defections-and-aussie-jobs

After being moribund for much of the past 24 hours, markets have displayed a somewhat stronger pulse in the hour or so following publication of the January FOMC meeting Minutes – meaning a US dollar some ¼% up on where it was pre-Minutes and US Treasury yields 1-2bps higher across the curve. In justifying this reaction, my speed-reading BNZ colleague Jason Wong picks out this quote: “Many participants observed that if uncertainty abated, the Committee would need to reassess the characterization of monetary policy as “patient” and might then use different statement language.” This can be read as implying that the Fed still retains a tightening bias of sorts, in which respect Fed Vice Chair Rich Clarida is just out saying that “I don’t think the Fed made a U-Turn” (In January).

Earlier in the text, the Fed notes that softness in both core and headline inflation provides reason for a ‘patient’ approach, in order to assess the impact of past rate rises, etc.. It also notes that some downside risks to the outlook had recently increased even though the economy at the time of the meeting was fairly characterised as showing a ‘strong labour market’ and inflation ‘near target’.

On the Fed’s balance sheet, the Minutes note that ‘almost all’ FOMC members wanted to halt the run-off later this year.

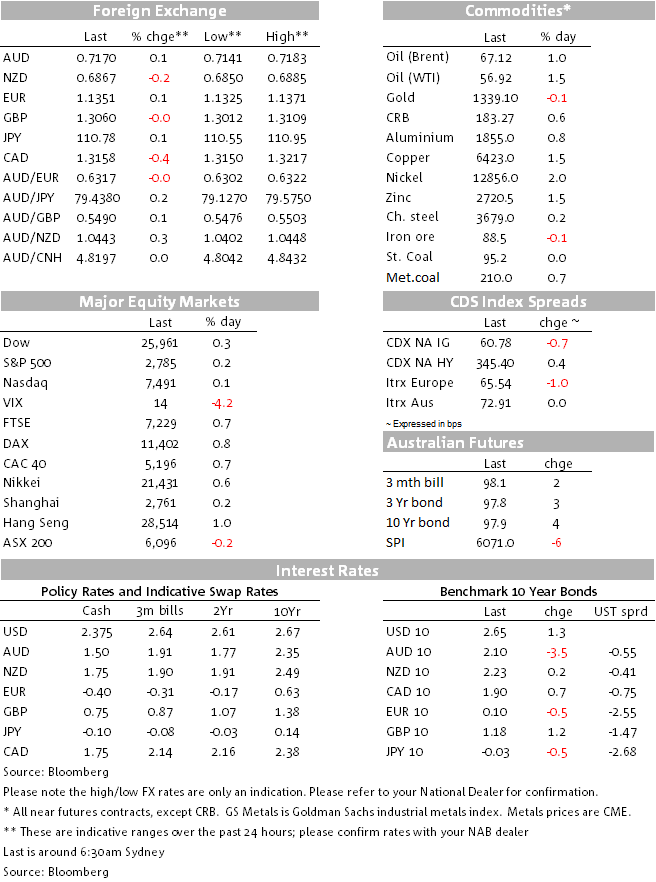

The generalised positive US dollar reaction to the Minutes means that two of the night’s best performing currencies – GBP and AUD – have seen their gains reduced, AUD/USD to 0.7169 as I wrote from 0.7183 and GBP/USD to 1.3058 from a high of 1.3109.

Strength in the latter followed news of further defections – from three Tory MPs as well as another Labour lawmaker – into their newly formed centrist parliamentary grouping, moves which on our read (not universally shared, we should add) are seen to further diminish the risk both of a March 29th ‘hard Brexit’ and a successful no-confidence motion being brought by Labour leader Jeremy Corbyn and hence early elections. Incidentally, an opinion poll published overnight puts the Tories on 38%, Labour of 26% and the ‘Independence’ group (i.e. this week’s ‘splitters’) at 14%.

UK PM May and EU chief negotiator Juncker have just been out saying that the two reconfirmed their commitment to avoiding a hard border on the island of Ireland and that their talks covered the role alternative arrangements could play in replacing the backstop in the future. Earlier in the night, reports were that whatever change in wording – or adjunct to the Withdrawal Agreement – is crafted, the EU wants Theresa May to go back and get it ratified before the whole of the EU would be asked to sign off on it. Still no mean feat. If May’s deal doesn’t get through Parliament soon, then the odds continue to favour her losing control of the process. Parliament is expected to take over in a likely scheduled vote from 27 February.

As for AUD, this fell by about 15 pips yesterday, with 3-year rate futures some 2.5 ticks higher, on the Q4 Wage Price Index which came in at +0.5% (NAB, mkt: 0.6%, 0.6%P) with annual growth steady at 2.3% (2.3%E). Annual wage growth bottomed some time ago, but the pace of improvement has been slow and growth is well below the long-run average of 3.2%. In a statistical quirk, both public and private wages rose at a faster rate than the headline total, up 0.6% in Q4, where this reflects the ABS calculating growth using rounded wage data. Annual growth in private wages excluding bonuses continued to trend higher, reaching 2.3%, while growth including bonuses remained elevated at 2.8%. Today’s labour Force survey should be more influential on RBA thinking (see below).

45 minutes ahead of the NYSE close, US stocks are generally showing small gains (DJIA and S&P 500 both up 0.2%, NASDAQ flat). Materials are the standout S&P sector, +1.91%, with gold, copper and steel-related counters all showing strong gains (2.5-3.0%). In this respect copper prices are up 1.4%, steel rebar futures +1.7% iron ore futures and gold up just 50 cents but meaning it has held Monday’s $14 gains (when US stocks were closed, hence catch-up today). SPI futures are up 0.15%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed to almost flat in March

Insight

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.