Coming in for landing in a heavy cross wind

Insight

Fed hikes by 25bps, signals ‘ongoing rate increases’ will be appropriate..

Okay, so you’re a rocket scientist, That don’t impress me much, So you got the brain but have you got the touch, Don’t get me wrong, yeah I think you’re alright, But that won’t keep me warm in the middle of the night. That don’t impress me much – Shania Twain

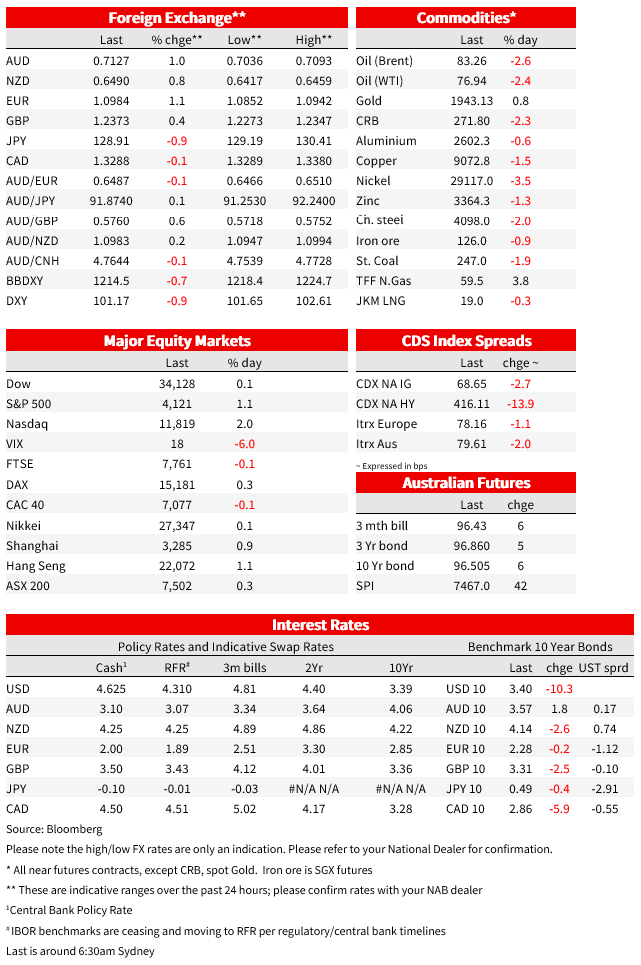

In delivering the ‘as expected’ 25bps lift to the Fed Funds Target Rate an hour ago, the hawkish messaging if the Statement , viz that ‘ongoing rate increases’ (plural) will be required and that while inflation has ‘eased somewhat’ it ‘remains elevated’ the knee-jerk sell-off in bonds and equities and lift to the US dollar this generated were all very small and already partially reversed ahead of the post-meeting Powell pressure. The latter has yielded nothing to scare the market, or which it didn’t expect to hear- still happily persisting in the believe the Fed will be cutting rate in the second half of this year – such that bond are rallying hard, the USD is dropping and the more interest rate sensitive NASDAQ off to the moon.

In the ensuing press conference, Fed chair Powell spoke of the need for the Fed to stay restrictive for ‘some time’, that substantially more evidence was needed to be confident inflation is on sustained downward path, and that the Fed’s focus is on sustained changed to financial conditions (but which he acknowledged had tightened ‘very significantly’ in the past year). The FOMC is talking about a ‘couple more rate hikes’ pre-pause – a message fully consistent with the December FOMC Summary of Economic projections ‘dots’ which show a median 5.0-5.25% 2023 Funds rate (versus a market that continues to see a sub-5% ‘mid-point’ terminal target rate).

US data releases – three in all, produced overs (JOLTS) and unders (ADP, Manufacturing ISM). ADP private payrolls rose just 106 k in January, well below the expected 180k, but the report noted bad weather held back employment growth. More disconcerting, annual wage growth for workers who remained in their job remained strong at 7.3%, while job-changers saw accelerated median pay rises of 15.4%, data going against other recent releases (Average Hourly Earnings – next update tomorrow – and this week’s Q4 Employment Cost Index, both of which suggest moderating wage inflation).

The JOLTS report (for December) showed a surge in job openings to a five-month high of 11.021m. While still well below the 11.86m March 2022 peak, the ratio of job openings to unemployed rose from 1.7 to 1.9, a figure the Fed chair has previously indicated he would like to see closer to 1. Today’s FOMC statement and messaging surrounding it from chair Powell should be seen in this context, giving no succour to ongoing market confidence ion rate cuts before 2023 is out.

Back on the ‘unders’ side, the ISM manufacturing index fell for a fifth consecutive month to 47.4 from 48.5 (48.0 expected and implying manufacturing contracting at a faster pace). Amplifying the message from the headline, the new orders component slumped to 42.5 from 45.1 (lowest since May 2020 and prior to that, March 2009 (GFC era). Prices paid blipped up to 44.50 from 39.4 but remember this reading was above 87.0 back in March 2022. Employment was 50.6, just down an a (downward revised) 50.8 in December.

Eurozone CPI inflation fell by a much larger than expected 0.7% in headline y/y terms , to 8.5% from 9.2% (consensus 8.9%) but the core measure was unchanged at 5.2% against a fall to 5.1% expected, highlighting the dominance of recent sharp energy price falls in driving the headline drop ( something ECB hawks later today will doubtless be keen to highlight). Also of note is that the numbers still lack Germany’s actual contribution, worth some 28% of the headline index, leaving the final numbers subject to risk of a large revision one way or the other (Eurostat reportedly incorporated a forecast into the numbers published Wednesday).

As for yesterday’s local data during our time zone, the NZ labour market data came in on the soft side of market expectations and, importantly, softer than the RBNZ projected, – sluggish employment growth of 0.2% q/q in Q4, a lift in the unemployment rate to 3.4% and wage inflation remaining strong but further signs that, like CPI inflation, it has peaked. As a result and following the earlier Q4 CPI report, our BNZ colleagues altered their RBNZ forecasts to now expect 50bps in February scaling down to a (final) 25bps in April, taking the ‘terminal’ OCR to 5.0% (versus latest market pricing currently close to 5.25%).

In markets with still an hour to before the NYSE close , the S&P 500 is up 0.9% and the NASDAQ around 2%. US 10-year Treasury yields, which rose from 3.47% to 3.50% immediately post the FOMC Statement have since dropped 10bps to 3.40%, and 2s from a post-statement high of 4.255% to 4.125%. The USD is accordingly smartly lower in conjunction with lower yields and strong risk appetite, the DXY index off the best part of 1% on the day do far, more than half of that coming post-FOMC/Powell presser. AUD, SEK and EUR are all showing gains of 1% or more (AUD/USD to a high of 0.7136, so still a tad below its January high of 0.7142). CAD is dragging the chain consistent with its link to the big dollar’s fortunes, up just 0.1%.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.