Online retail sales growth slowed in May following a fairly strong April

Insight

Sanctions are stepped up against Iran today. Plus, the latest on Brexit.

https://soundcloud.com/user-291029717/tariffs-tehran-mid-terms-and-a-breakthrough-for-the-aussie-dollar

Well it is officially Guy Fawkes night in the UK (November 5th) and there are some fireworks going off under Sterling this morning courtesy of the latest on Brexit from the UK Sunday Times (see below). Incidentally, First Aid Kit’s ‘Fireworks’ is infinitely better than Katy Perry’s singular “Firework’, even though I bet you’re all now singing the latter in your head.

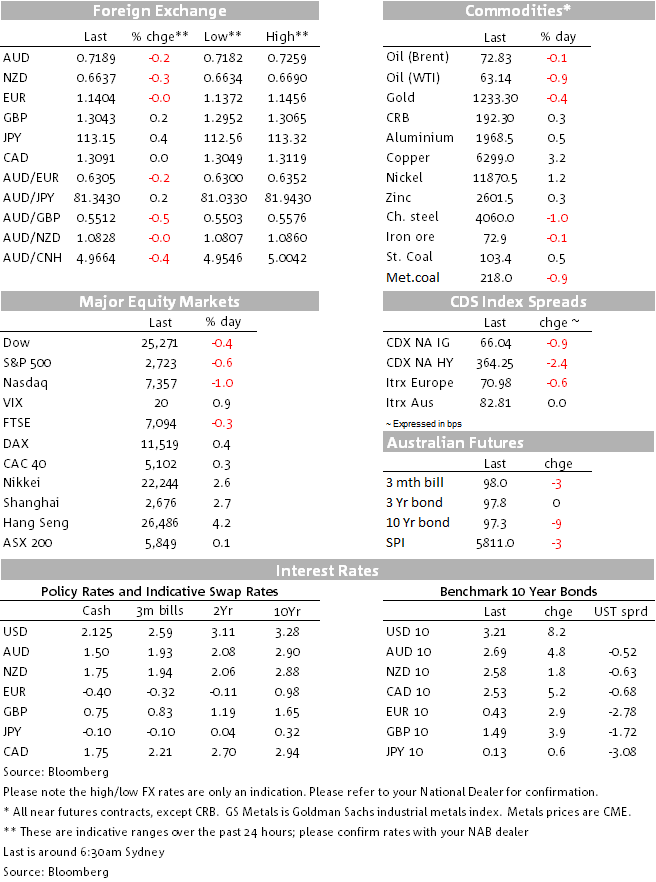

Friday’s US payrolls report exceeded expectations only in respect of the headline non-farm payrolls print (250k against 200k expected) with the unemployment rate unchanged at 3.7% as expected thanks to a 0.2% rise in the about participation rate, while average hourly earnings printed at 0.2% as expected but which lifted the annual rate to 3.1% (3.14% unrounded) and the first time above 3% since 2009.

The data prompted a partial reversal of Thursday’s USD fall back (after new local cycle highs seen on Wednesday) and lifted UST yield by between 5.9bps (2s) and 8.2bps (10s). US stocks had opened higher Friday, but the rise in bond yields weighed as the session progressed, the IT sector leading the falls with the computer hardware sub-sector the weakest, thanks to a 6.6% drop in Apple, whose shares had of course fallen in after-hours trade on Thursday. This was after its Q3 results and where the market didn’t like the lack of unit-volume growth for the iPhone and the announcement that henceforth Apple wouldn’t be breaking down its unit sales volume numbers by product.

All the main US indices finished lower, NASDAQ faring worse down 1%. On the week, the end/beginning of month turn-round sees US indices up by between 2.4% (Dow) and 2.7% (NASDAQ) with Asia stocks the standout winners (Nikkei +5%, Shanghai +3%) thanks to the glimmer of hope for diffusion of trade tensions following President Trump’s late-week tweets regarding his conversation with China’s President Xi, and then news reports Friday that President Trump has instructed officials to draft terms for a potential trade deal. Later in the NY session, White House economic advisor Larry Kudlow tried to cool expectations for a Trump-Xi agreement, telling CNBC “we’re not on the cusp of a deal”.

All G10 currencies lost ground against the USD post-US payrolls, JPY leading the way down, with a 0.4% loss and intra-day high of ¥113.32. Some of the mid-week surge in GBP on Brexit-related optimism was lost on a combination of USD strength and the failure of EU officials to offer any public support for the UK’s government’s apparent outbreak of optimism about proximity to a deal, including on financial services.

This has changed again this morning, after the UK Sunday Times reported on its front page that “Theresa May’s secret plan to secure a Brexit deal and win the backing of parliament can be revealed today. Senior sources say the prime minister has secured private concessions from Brussels that will allow her to keep the whole of Britain in a customs union, avoiding a hard border in Northern Ireland. They expect this to placate remainer Tories and win over some Labour MPs”.

The story claims that the deal entails open ended UK inclusion in the Customs Union, pending an agreement to a ‘Canada-plus’ style Free Trade Agreement. The latter means UK would be free to negotiate FTA’s with other countries (a key demand of “Brexiteers”) while at the same time the open-ended Customs Union arrangement might satisfy “Remainers” (including some in the Labour party) as well as, crucially, the DUP MPs who prop up the government in so far as obviates the end to re-impose some form of Irish border.

GBP/USD closed in NY on Friday at $1.2970 and is currently quoted at $1.3045, following the Times story.

The relative strength of AUD and NZD on Friday, each down just over 0.1%, can be put down to still-entrenched short positioning and the tailwind from the EM FX rally that started mid-week and extended on Friday thanks to strong gains for TRY, ZAR, MXN and CNY (latter +0.49%). The JPM EMCI added 0.4% in the face of an otherwise stronger USD, the ADXY 0.3%:

On the week it’s NZD that has been the star performer followed by AUD, confirming the status of these two currencies as the favoured EM FX proxies, still-short speculative positioning – as evident again in latest CFTC futures data published on Friday for the week through last Tuesday – and in case of AUD at least, the ability to break up through some important technical levels on Thursday. The USD ended just in positive territory for the week (DXY +0.2%, BBDXY +0.3%):

“Bear steepening” in the US Treasury market characterised both the day and the week, moves that commenced with the mid-week turn-round in US stocks and where moves in both stocks (up) and bonds (down) may have been exaggerated by rebalancing flows from managed funds. In terms of cross-market spreads, the main feature of last week is a compression of over 20bps in the 10-year Italy-Germany bond spread, in itself a supportive influence under the Euro.

Base metals continued to feed positively of the hopes, however slender, for diffusion of Sino-US trade tension, also helped by a softer USD Friday, while oil remains pressured as US sanction against Iran oil exports take effect from today, but where up to eight countries are seen to have secured exemption for the time being. Also, Russia tells the FT is intends to help Iran sidestep sanction, presumably by white labelling Iran oil as its own. On the week, copper’s 2.4% gains has just kept the LMEX index in positive territory with all other base metals lower, while the standout feature is the sharp (6%+) falls in oil:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.