A private sector improvement to support growth

Insight

The main takeaway being that Americans anticipate income growth to slow and inflation to stay elevated.

NZ: Performance of services index, Jan: 54.5 vs. 52.1 prev.

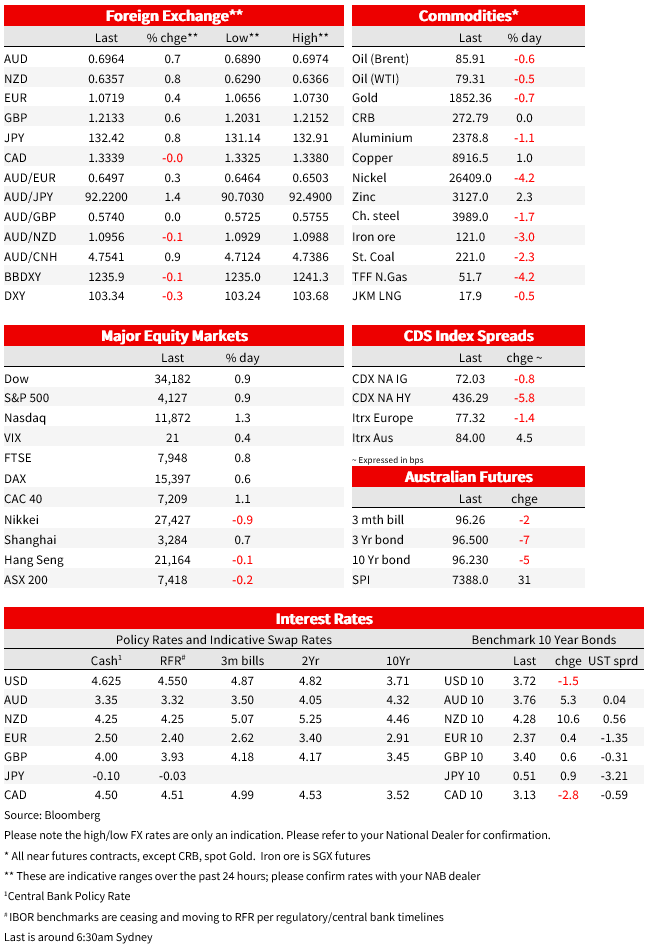

Positive thinking is said to contribute to less stress, better overall physical and emotional health, longer life span, and better coping skills. On that note, equity investors have begun the new week looking at the bright side of life notwithstanding a further rise in front end yields with the UST curve flattening as 10y UST yields ease a couple of bps to 3.71%. US CPI is the big the data release over the next 24 hours and the rates markets is seemingly bracing for a strong print while equity investor seemingly reckon “She’ll be right”. The USD is weaker across the board with NZD and AUD at the top of the leader board while ahead of the official BoJ Governor nomination today, JPY is the lonely USD underperformer.

It has been a quiet night in terms of data releases and perhaps that has played into the media airplay given to the January release of the New York Consumer survey. The main takeaway being that Americans anticipate income growth to slow and inflation to stay elevated. Of note, the survey revealed a 1.3% decline in expected household income, the largest monthly decline in almost ten years. On the inflation front the survey revealed expectations on inflation one year ahead were unchanged at 5% while households were mixed about where inflation might head in the longer run. Inflation expectations softened to 2.7% three years ahead but increased at the five-year-ahead horizon to 2.5%. The equity market seemingly paid more attention to the expected decline in household income which should eventually ease price pressures in the future.

As I type the S&P 500 is up just over 1% while the tech-heavy Nasdaq 100 is +1.38%, following its first weekly loss of 2023. Meanwhile in Europe all main regional equity indices ended with positive returns on Monday with the EuroStoxx 600 +0.9%.

Playing into the positive vibes, overnight the EU commission upgraded its economic growth outlook for the region and downgraded the inflation outlook, supported by an easing of the energy crisis. Economic growth is now seen at 0.8% vs +0.3% previously for EZ and +0.9% from 0.3% for broad EU. The recovery extends into 2024 with EZ growth seen at 1.5% while inflation is expected to decelerate from 8.4% last year to 5.6% in 2023 and 2.5% in 2024.

My BNZ colleague Jason Wong notes that the Bank of America US credit card data is showing signs of “a meaningful increase in spending” during the weeks after Christmas. The Bank suggested that consumers could have held back pre-Xmas holiday spending to maximise savings from post-holiday discounts and also noted the increase in minimum wage in over 20 states, the 8.7% lift in social security payments, and resilience of the labour market as factors contributing to increased spending through January. The report was released a few days ago, but it certainly plays to the additional increase in UST front end yields. The 2y rate is up 2.3bps since the market opened in Tokyo yesterday and now trades at 4.537%, at the start of February the yield was 4.10%. The UST curve has a flattening bias with the 10y Note yield down almost 2bps to 3.7168%.

Moving onto currencies the USD a tad weaker across the board with JPY the notable exception (-0.93%). Over the past 24 hours USD/JPY has edged up almost 1 big figure to ¥132.475 with the market seemingly still trying to assess what a BoJ will look like with Ueda under the helm . After media reports confirming its nomination over the weekend, the government is expected to officially announce his nomination today along with his two deputies. The LDP has a majority in parliament, so ratification of the nominees is expected at the end of the month. Ueda is regarded as a sensible outsider choice; he is not a fully committed uber dove and as an outsider he should have more flexibility. Notably too, at least on record, he would seems more willing to consider alternative ways of thinking. The Governor will take charge in April and in the meantime the rise in core global yields may still pose a challenge to the BoJ. 10y JGBs closed Monday at 0.51%, the YCC band could be tested once again if core yields rise further from here.

The improvement in risk appetite evident in the equity market alongside gains in metal ( Copper 1%) and oil (0.8%) prices have favoured pro-growth currencies such as the AUD and NZD (although iron prices are weaker -3.0%). The AUD now trades at 0.6964, up 0.7% over the past 24 hours while the kiwi is 0.8% and starts the new day at 0.6358, both trading near their highs for the session. EUR (@1.0718) and GBP (@1.2133) have made smaller gains, up 0.61% and 0.37% respectively.

In other news, in a sign of an ease in political tensions, after spending the past week or so popping balloons high in the sky. Bloomberg reports the US is considering a meeting with China officials, Secretary of State Antony Blinken may meet with Wang Yi, China’s top diplomat, at a security conference later this week.

The US NFIB survey is also out tonight, and Fed’s Logan, Harker and Williams speak.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.