We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

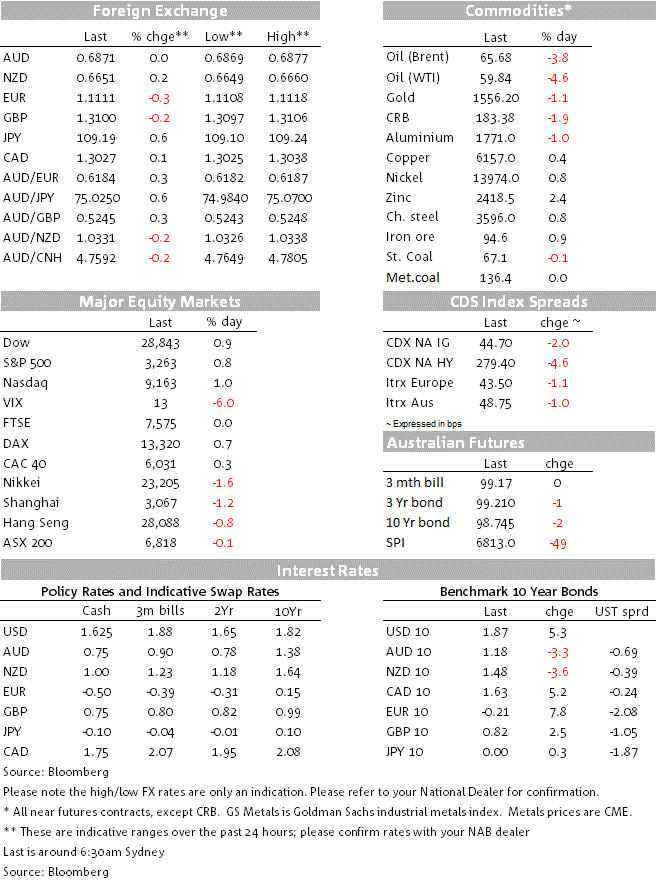

Markets have now largely unwound the risk-off moves that have occurred since Friday.

Iran-US tensions have de-escalated dramatically over the past 24 hours, despite the Iranian missile strikes yesterday. The main driver was President Trump’s delayed response to the missile strike yesterday, suggestive that he was taking a more cautious approach then his usual demeanour and prior tweets suggested. That interpretation was confirmed overnight as Trump backed away from further conflict, instead advocating further sanctions and noting “Iran appears to be standing down, which is a good thing”. The Iranian strike was also phrased as being limited and “proportionate”, while the strike itself did little damage to US assets and some geopolitical analysts classed the strike as more symbolic in nature and being a “warning shot” designed not to inflict too much damage on US assets.

Markets have now largely unwound the risk-off moves that have occurred since Friday. Brent oil after falling 3.8% overnight is now actually 0.7% lower than it was prior to the assassination of General Soleimani at $65.72 a barrel. The Yen is now weaker, USD/JPY +0.6% overnight and is now 0.6% higher than it was prior to the assassination. Yields have also done the round trip with US 10yr now unchanged since the assassination, moving in a 17bps range since Friday. The exception is gold, which while declining 1.1% yesterday, is 1.8% higher to $1,552 since Friday.

Markets have priced out the probability that the tensions spiral into a cycle of retaliation. This is important given economic data to date has suggested some stability emerging in the global economy – most recently seen in the Services PMI and the US Non-manufacturing ISM. Assuming Iran-US tensions continue to simmer rather than boil, markets are likely to re-focus on the global growth outlook and on trade with the interim US-China trade deal expected to be signed on 15 January. US politics also appears to be relatively benign, with Politico noting that Wall Street Execs expect Trump to win again in 2020 and that Joe Biden will likely win the Democratic nomination ahead of more leftist candidates Warren and Sanders.

Its no surprise then to see equities up overnight with the S&P500 +0.8% to 3,263 and driven by broad-based gains apart from energy stocks which are down 1.5% on the lower oil price. The risk of a melt-up in stocks that many had tipped to start 2020 now looks to be a more probable scenario.

Yields have risen in the more positive environment with US 10yr Treasuries +5.3bps to 1.87%. Pricing for a Fed rate cut by the end of 2020 has also reduced from being an almost certain event being 112% priced, to now 80% priced.

There was little news outside of easing geopolitical tensions of significance. UK PM Johnson met with the European Commission President von der Leyen reiterating he wants a deal done by the end of 2020, while the EU continues to emphasise that a comprehensive deal in that timeframe is “basically impossible”. Subsequent comments emphasise that the UK is aiming for a Canada-style FTA by the end of the year. The comments saw some gloss come off GBP, down 0.2% to 1.3103.

There was little of significance out. German Factory orders fell sharply, down 1.3% against expectations of a 0.2% rise. The data saw EUR trade with a soft tone with EUR -0.3% to 1.1111.

Weakness in both GBP, EUR and Yen saw the USD (DXY) rise 0.3% to 97.30. ADP Payrolls were stronger than expected at 202k against the 160k consensus. There were also substantial upward revisions to last month’s weak read which was revised to 124k from 67k. With revisions the average ADP jobs gain is now 163k, more in line with official payrolls growth and still suggestive of a robust labour market. The move in ADP also helped the move in yields.

The Australian dollar was broadly unchanged at 0.6870. The ebbing of geopolitical risk has yet to be fully reflected in the AUD with AUD/JPY still -1.0% since Friday’s events. There is a growing consensus that the fallout from the bushfires may tip the RBA into cutting rates February with markets just over 50% priced. Data yesterday in Australia though did act as one counter with surprising strength in Building Approvals (+11.8% m/m against 2.0% expected) and Job Vacancies (+1.6% q/q, reversing last quarter’s -1.6%).

Domestic focus will be on the Trade Balance, though is unlikely to be market moving this month. Internationally, with geopolitical tensions easing between US-Iran, focus likely shifts back to the data with Chinese CPI figures and a host of Fed speakers out today.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.