On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

The path of central banks does seem to be having as many twists and turns as a Dickensian novel. NAB’s Ray Attrill says the path of bond yields at the end of the week showed how the UK is taking a divergent path from the US, where central bank speakers are still suggesting there will be more hike(s) to come.

Good morning

Go your own way, You can call it another lonely day (Another lonely), You can go your own way, Go your own way – Fleetwood Mac

Fridays’ data and events highlights:

Japan August CPI 3.2% from 3.3% vs. 3.0% expected

Japan August CPI ex fresh food 3.1% from 3.1% vs. 3.0% expected

Japan August CPI ex-food & energy 4.3% from 4.3% vs. 4.3% expected

BoJ Policy Balance Rate -0.1% unchanged as expected

BoJ 10yr. YCC target 0% unchanged as expected

UK August Retail Sales inc. auto fuel 0.4% m/m vs. 0.5% expected

UK August Retail sales ex. auto fuel 0.6% m/m vs. 0.7% expected

France September Manufacturing PMI 43.6 from 46.0 vs. 46.1 expected

France September Services PMI 43.9 from 46.0 vs.46.0 expected

France September Composite PMI 43.5 from 46.0 vs 46.0 expected

Germany September Manufacturing PMI 39.8 from 39.1 vs 39.5 expected

Germany September Services PMI 49.8 from 47.3 vs 47.1 expected

Germany September Composite PMI 46.2 from 44.6 vs 44.7 expected

Eurozone September Manufacturing PMI 43.4 from 43.5 vs 44.0 expected

Eurozone September Services PMI 48.4 from 47.9 vs 47.6 expected

Eurozone September Composite PMI 47.1 from 46.7 vs 46.5 expected

UK September Manufacturing PMI 44.2 from 43.0 vs 43.2 expected

UK September Services PMI 47.2 from 49.5 vs 49.5 expected

UK September Composite PMI 46.8 from 48.6 vs 48.7 expected

US September Manufacturing PMI 48.9 from 47.9 vs 48,2 expected

US September Services PMI 47.2 50.2 from 50.5 vs 50.7 expected

US September Composite PMI 50.1 from 50.2 vs 50.4 expected

Canada July Retail Sales 0.3% m/m vs. 0.4% expected

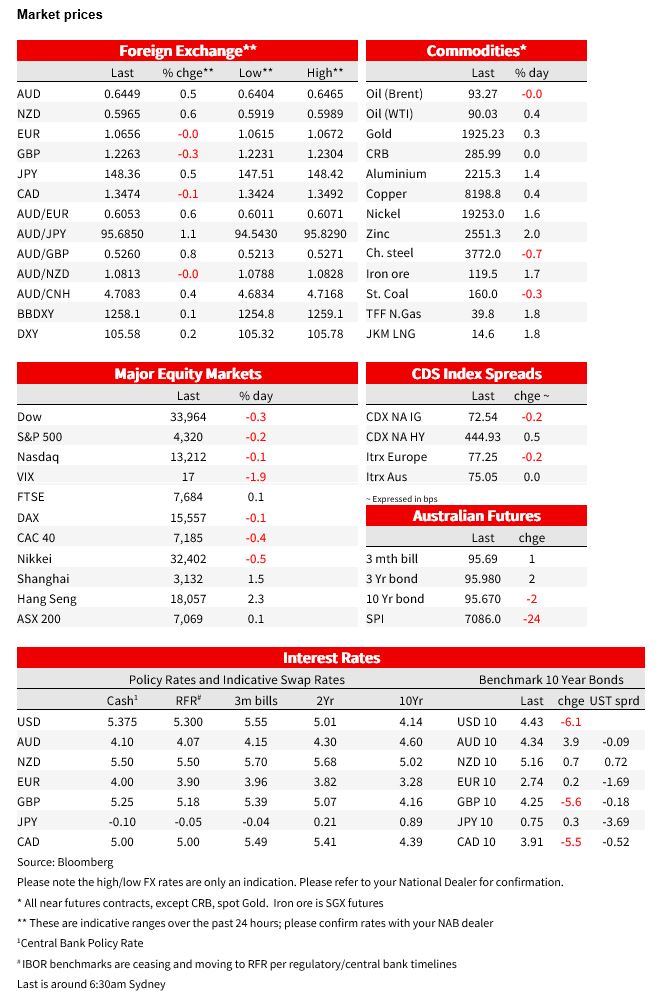

After probing above 4.50% in Friday’s Tokyo trade, 10-year US Treasuries recoiled during the European and US sessions, closing in NY at 4.43%, in conjunction with US equities extending their losing streak to a fourth day (and third week), stocks reportedly suffering some impact from news United Autoworkers Union (UAW) workers were extending strikes to more GM and Stellantis parts factories. While the US dollar extended its gains, this was mostly against the JPY post the BoJ’s no-change decision, GBP and EUR, where latest UK and EZ PMI news was overall negative. AUD and NZD appeared to benefit from strong gains for Hong Kong and China stocks Friday, even though CNY was little changed. In the week ahead, a looming US government shutdown of non-essential departments from mid-night Saturday and a broadening of UAW car plant shutdowns will capture much attention. US PCE deflators and EZ CPI are the main international data draws, while locally we get the August CPI release as well as Retail sales. China official PMIs are on Saturday

The Bank of Japan on Friday’s rounded out an intense week of central bank policy decisions, and while the no-change outcomes with respect to both the -0.1% Policy Rate Target and 0% YCC target were fully expected, USD/JPY rose to a high of ¥148.40 after the ensuing press conference from BoJ Governor Ueda. Mr. Ueda said nothing to encourage the view that a policy shift could be afoot as soon as the next (October 31) meeting. He said Japan is not in a situation where BoJ can see the (inflation) goal being met, that the distance to ending negative rates had not changed much, and repeated that the BoJ has prioritised the risk of acting too soon.

Fed speak on Friday, post Wednesday’s “hawkish hold’ FOMC outcome, included Governor Michelle Bowman, marking herself out as one of the more hawkish FOMC members by saying. “I continue to expect that further rates hikes (plural) will be needed to return inflation to 2% in a timely way”, noting that in the latest Fed economic projections, inflation is expected to stay above 2% until at least 2025.

Boston Fed President Susan Collins meanwhile said, “I expect rates may have to stay higher, and for longer, than previous projections had suggested, and further tightening is certainly not off the table,” though added the Fed needs to show patience before raising rates again so it can sift through the economic and separate “the signal from the noise.”

San Francisco Fed President Mary Daly echoed Collins’ remarks, saying “We hold rates steady so we have more time to collect the information we need to see if more is necessary or if we can simply hold where we are…What we did at the meeting this week is not a predictor of what we will do at the next meeting….I have not gotten to a point where I get to declare victory.”

Incoming economic news tended to support the prevailing market narrative that the US is doing ‘better than the rest’ or rather at least relative to Europe (equivalent China numbers won’t be available until Saturday). UK PMIs confirmed the hint in last Thursday’s Bank of England Minutes that they had deteriorated (Services especially) and while in the Eurozone Germany’s lifted a little, in France they crunched lower, its composite index now at just 43.5 down from 46.0. The Eurozone composite reading improved marginally, but at 47.1 from 46.7 remains mired deep in contractionary territory. US (S&P Global) PMIs also deteriorated, but its Composite reading is still just above 50 (50,1 from 50.2) and of late has been sharply at odds with the more established (and much stronger) ISM surveys (September readings not out until next week). We really don’t know which ones to believe right now.

Coming Up

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.