Total spending grew 0.9% in June.

There are three bits of news driving optimism in the markets.

https://soundcloud.com/user-291029717/a-trio-of-optimism

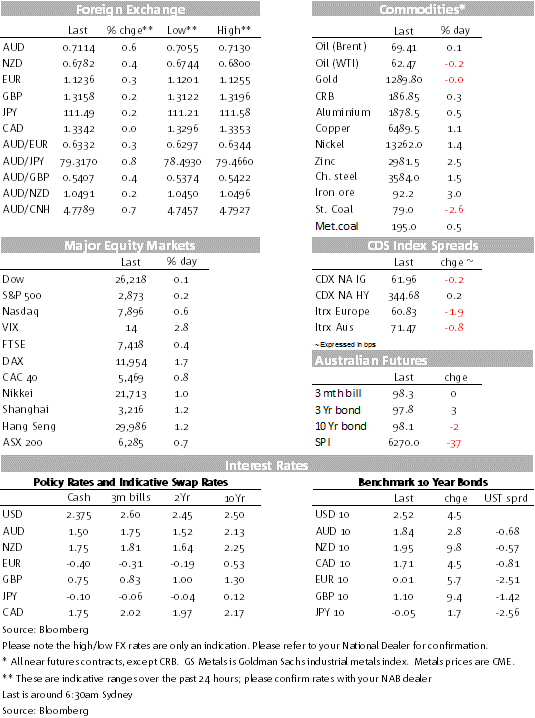

It all started yesterday with the FT reporting China and the US were close to agreeing a trade deal, then solid China and Europe Services PMIs helped the positive vibes, easing concerns over a protracted global growth slowdown. The probability of a soft-Brexit has also risen with Parliament getting ready to pass a bill to block a no-deal Brexit while PM May and opposition leader Corbyn have a constructive initial chat. European equities have led the gains in equities, but US equities have struggled to maintained the positive momentum. Core global yields have also headed north with UK Gilts leading the move higher. Ease in safe haven demand has seen the USD lose ground across the board with the AUD top of the leader board, extending its gains after yesterday’s solid retail sales print.

Yesterday risk assets were boosted following an FT report noting that top US and Chinese officials have resolved most of the issues standing in the way of a trade deal with China’s vice-premier, Liu He getting ready to meet Robert Lighthizer, the US trade representative, and Steven Mnuchin, the US Treasury secretary, for a potentially climactic negotiation session starting Wednesday in Washington. That said while talks on a new trade relationship appear to be close to a resolution, the article also noted that discussion over implementations (will the US lift or keep tariffs in place?) and the terms of an enforcement mechanism ( threat of more tariffs) could easily derail all the constructive progress so far. Playing into this cautiously optimistic view, overnight Trump’s economic advisor Kudlow said that negotiators are “making good headway…but we’re not there yet”.

Also during our session yesterday, the bounce in China’s Caixin services PMI (54.4 vs. 52.3 exp. a new 14-month high) was an additional boost to risk assets which were further enhanced during the overnight session by better than expected final European services PMIs (see details below).

Going against the grain, US data overnight were on the softer side, with the US non-manufacturing ISM disappointing – although the composite index remains at a high level and the employment component improved – while ADP employment was softer. More weight will be given to US payrolls data released at the end of the week, where the consensus expects a solid 180k monthly increase.

The US 10-year Treasury rate rose 3bps on the FT report to 2.50% and overnight has traded a tight 2.50-2.52% range. UK Gilts led the move higher over night with the 10y tenor gaining 9.3bps to 1.095. Brexit news have also been supportive with the UK Parliament very close to passing a bill to avoid a hard-Brexit while PM May and Opposition Leader Corbyn were reported to have had a constructive chat on their objective to reach a Brexit compromise. Germany’s 10-year rate jumped higher on the European open and the stronger PMI data helped pushed it back into positive territory, closing at 0.08%, up 6bps for the day.

European equities opened higher following a positive lead from APAC and then extended their gains on the PMI and Brexit news. US equities also opened higher with the softer than expected ISM print only resulting in a brief pullback early in the session. Notwithstanding energy and consumer stables underperformance, all three major indices look set to close in positive territory.

Moving onto currencies the USD is softer across the board amid a decline in safe haven demand. That said, both the DXY ( -0.30%) and BBDXY(-0.11%) indices remained close to the top of their ranges held over the past year. A closer look at G10 performance reveals the AUD ( 0.61%) and SEK (0.61%) as the top performers over the past 24hrs. In addition to the China US trade news, yesterday the AUD was also boosted by a much stronger than expected Australian retail sales February print (+0.8% vs 0.3% NAB 0.2%) and better than expected trade surplus increasing from $4.4b in January to $4.8b (market: $3.7b; NAB: $3.5b). There were some unusual moves in the underlying retail sales number suggesting an overstatement in the Department Store Sales (+3.5% m/m against a trend -0.2% in the series) and Food Retailing (+0.8% m/m against a trend of 0.4%). So we think caution is needed when interpreting the numbers. More of the same will be required in order to give the RBA and the market some reassurance that household spending could bounce over the coming months. We would also add that data the does little to change the view that household consumption is coming under pressure from house price declines and subdued income growth. Although we have seen a pullback in RBA rate cut expectations in recent days, the markets is still pricing a 25bps rate cut by September this year.

Stronger PMI data have supported EUR, which is back up near 1.1235. GBP remains supported after PM May’s pivot yesterday morning, which saw her reach out to the opposition Labour party for a cross-party solution to the Brexit impasse. Both sides have said that talks are “constructive” and the odds of a soft form of Brexit have increased. A UK bill aimed at blocking no-deal Brexit is expected to pass later today JPY is the weakest of the majors since this time yesterday, given the higher global rates backdrop. USD/JPY trades around ¥111.50.

As we are about to press the send button, Bloomberg is reporting further progress in the US-China trade negotiation. The US is said to set a 2025 target for China to meet trade pledges. The plan would see China committing by 2025 to buy more US commodities, including soybeans and energy products, and allow 100% foreign ownership for US companies operating in China as a binding pledge that can trigger retaliation from the US if left unfulfilled.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.